- Comprar cripto

- Mercados

- Futuros

- Spot

- Copy trading

WE-Launch

WE-Launch

a16z: How will stablecoins eat into the payments industry? What happens after that?

Original title: How stablecoins will eat payments, and what happens next

Original author: Sam Broner, a16z crypto investment partner

Original translation: 0xjs, Golden Finance

Today's payments landscape is dominated by gatekeepers who charge high fees, undercut the profitability of every business they touch, and justify those fees in the name of ubiquity and convenience — while they stifle competition and limit the creativity of builders.

Stablecoins can do better.

Stablecoins have lower fees, more competition among payment providers, and wider accessibility. Because stablecoins reduce transaction costs to almost zero, they can free businesses from the friction of existing alternatives. Adoption of stablecoins will start with businesses most affected by current payment methods, a process that will disrupt the payments industry.

Stablecoins have become the cheapest way to transfer dollars. Last month, 28.5 million unique stablecoin users sent over 600 million transactions. Stablecoin users are found in nearly every country and use stablecoins because they offer a safe, cheap, and inflation-resistant way to save and spend. Aside from cash and gold, stablecoins are the only widely adopted payment method that can operate without gatekeepers such as banks, payment networks, or central banks. At the same time, stablecoins are permissionless, programmable, scalable, and integrable—anyone can help build a stablecoin payment platform on top of a stablecoin payment rail.

This disruption may take time, but it may happen faster than many expect. Businesses such as restaurants, retailers, enterprises, and payment processors will benefit the most from stablecoin platforms, with significantly higher profit margins. This demand will drive adoption, and as stablecoin adoption continues to increase, the other benefits of stablecoins—permissionless composability and improved programmability—will bring more benefits to on-chain users, businesses, and products. I’ll share more whys and hows below, but first some background on the payments industry.

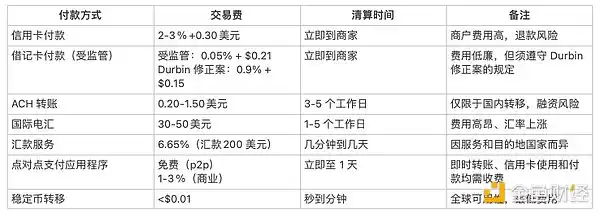

Payment Tracks

• Payment Channels: The technology, rules, and networks that process transactions

• Payment Processors: Operators on the payment rails that facilitate transactions

• Payment Service Providers: Entities that provide access to payment systems to end users or other systems

• Payment Solutions: Products provided by payment service providers

• Payment Platforms: A suite of interrelated payment solutions across providers, processors, and rails

Payments Industry Background

The size of the payments industry cannot be underestimated. In 2023, the global payments industry processed 3.4 trillion transactions worth $1.8 trillion and generated $2.4 trillion in revenue. In the United States alone, credit card payments accounted for $5.6 trillion and debit card payments accounted for $4.4 trillion.

Despite the industry’s ubiquity and scale, payment solutions remain expensive and complex, and payment apps are often shielded from the consumer experience. For example, while peer-to-peer payment app Venmo may look simple on the front end, on the back end, the product hides a maze of bank integrations, debit card vulnerabilities, and countless compliance obligations. Payment solutions are often interdependent, which adds to the complexity, and people still use a variety of payment methods: cash, debit cards, credit cards, peer-to-peer payment apps, ACH (Automated Clearing House), checks, etc.

The four main metrics for payment products are timeliness, cost, reliability, and convenience.

Consumers prioritize questions like “How much will I pay?” Merchants ask “Will I get paid?” But in fact, all four metrics are essential for both parties.

Ever since businesses had to find fraudulent credit cards in physical ledgers, waves of innovation have continuously improved the payment experience. Each wave of innovation has brought faster, more reliable, more convenient, and cheaper payment methods, which in turn has led to an increase in transaction volume and the amount spent.

But many customers are still not enjoying modern services, or are underserved. For merchants, credit cards are expensive, directly eating into their profits. Despite growing adoption of real-time payments (RTP), U.S. bank transfers are still too slow, taking days. And peer-to-peer applications are region- and network-specific, making transfers between ecosystems slow, costly, and complex.

While businesses and consumers have come to expect more sophisticated functionality from payment platforms, not all users benefit from existing solutions. In fact, most users pay too much in fees and don’t use all of the bundled payment products. But they accept the current state of affairs.

Where Stablecoins Fit In

The key to stablecoins disrupting the industry is the failure of existing payment solutions (high cost, low availability, or high friction), and the fact that bundled products of payment solutions (including identity, lending, compliance, fraud protection, and bank integration) are least necessary.

Take remittances as an example. It was born out of desperation. Many remittance users are underbanked and use highly fragmented banking services. As a result, these users see little value in native integrations between traditional payments and banking services. Stablecoin payments offer instant finality, low costs, and no middlemen, which are structural advantages for any payment user or builder. After all, with stablecoins, it costs less than $0.01 to send $200 from the United States to Colombia, but $12.13 on traditional corridors. (Remittance users need to send money home regardless of transaction costs, but will benefit greatly from lower fees.)

International commercial payments, especially for small businesses in emerging markets, also face high fees, slow processing times, and low bank acceptance. For example, a payment between a Mexican apparel manufacturer and a Vietnamese textile manufacturer will involve four or more intermediaries – local bank, foreign exchange, correspondent bank, correspondent bank, foreign exchange, local bank. Each intermediary charges a percentage and there is a risk of middleman bankruptcy.

Fortunately, these transactions occur between partners with a regular relationship. With stablecoins, Mexican payers and Vietnamese payees can experiment and eliminate slow, bureaucratic, and expensive intermediaries. They may have to work hard to find local channels and workflows, but in the end they can enjoy faster, cheaper transactions and more control over the payment process.

Small-value transactions (especially low-fraud face-to-face transactions, such as those conducted in restaurants, coffee shops, or corner stores) are also a promising opportunity. These businesses are cost-sensitive due to their low profit margins, so the 15-cent transaction fee charged by payment solutions has a big impact on their profitability.

For every $2 a customer spends on a cup of coffee, only $1.70 to $1.80 goes to the coffee shop, with the remaining nearly 15% going to the credit card company—just for facilitating the transaction. But credit cards are here for convenience: neither the consumer nor the store needs additional features to justify the charges. Consumers don’t need fraud protection (they’re just getting a cup of coffee) or loans (the coffee was only $2). And coffee shops have limited compliance and bank integration needs (they typically use integrated restaurant management software or none at all). So if there’s a cheap, reliable alternative, these businesses will take advantage of it.

Cheaper Payments Improve Profitability

Current payment system transaction fees directly hurt the bottom line for many businesses. Lowering these fees would provide a huge boost to profitability. The first shoe has already dropped: Stripe announced they will charge 1.5% on stablecoin payments, 30% less than what they charge for credit card payments. To support this effort, Stripe announced the acquisition of Bridge.xyz for approximately $1 billion.

Wider adoption of stablecoins would significantly improve profitability for many businesses—not just small businesses like coffee shops or restaurants. Let’s look at the financials for three public companies in fiscal 2024 to get a rough idea of the impact of reducing payment processing rates to 0.1%. (For simplicity, this assessment assumes that businesses pay a 1.6% hybrid payment processor cost and that on- and off-ramps have minimal costs. More on this below.)

· Walmart, with $648 billion in annual revenue, could pay $10 billion in credit card fees and make $15.5 billion in profit. Do the math: Given the elimination of payment fees and Walmart's profitability, its valuation (controlling for all other factors) could increase by more than 60% just through a cheaper payment solution.

· Chipotle is a fast-growing fast-food restaurant with $9.8 billion in annual revenue. It makes $1.2 billion in profit each year, of which it pays $148 million in credit card fees. Just by reducing fees, Chipotle could increase profitability by 12%—an astonishing number not available elsewhere on its income statement.

· National grocer Krogers has the lowest margins and therefore makes the most money. Surprisingly, Krogers’ net revenue and payment costs may be nearly equal. Like many grocery stores, its profit margin is less than 2%, which is less than the fees businesses pay to process credit card payments. With stablecoin payments, Krogers’ profits could double.

How will Walmart, Chipotle, and Krogers reduce transaction fees with stablecoins? First, consider an idealized scenario: consumers will not accept stablecoins all at once, and there will still be considerable fees until stablecoins gain enough acceptance, especially when starting and stopping use. Second, both retailers and payment processors oppose high-fee payment solutions. Payment processors are also low-margin businesses that give up most of their profits to credit card networks and issuing banks. When payment processors process transactions, most of their fees are passed on to payment networks. So when Stripe handles the online retail checkout process, they take a 2.9% cut of the total transaction and a $0.30 fee, but they pay more than 70% to Visa and the issuing bank. As more payment processors like Block- formerly Square, Fiserv, Stripe, and Toast adopt stablecoins to improve their profit margins, they will make stablecoins more accessible to more businesses.

Stablecoins have low fees and no network gatekeeper fees to pay. This means payment processors earn much higher margins on revenue from stablecoin transactions. Higher margins could lead payment processors to support and encourage more businesses and use cases to use stablecoins. But as payment processors begin to adopt stablecoins, expect stablecoin payment fees to compress over time: Stripe’s 1.5% fee is likely to fall.

Next Steps: Mass Consumer Adoption

Today, stablecoins are a new permissionless way to send and store money. Entrepreneurs are already building solutions to turn stablecoin rails into stablecoin platforms. As with previous innovations, adoption will occur gradually, starting at the fringes of consumer demand, then forward-thinking businesses, until the platform matures enough to meet the needs of everyday users and cautious businesses. Three trends will drive more mainstream enterprise adoption of stablecoins.

1. Increase back-end integration through stablecoin aggregation

Stablecoin aggregation (the ability to monitor, guide, and integrate stablecoins) will soon be integrated into payment processors such as Stripe. These aggregation products enable businesses to process payments at a much lower cost than current mechanisms without major process or engineering changes. Consumers may end up with cheaper products without knowing it, because invoices, payrolls, and subscriptions have lower structural costs by default.

Many of these stablecoin aggregation businesses have begun to attract customers who want instant settlement, low-cost, and widely available business-to-business or business-to-consumer payments. By integrating stablecoins in the backend, businesses will benefit from the advantages of stablecoins—without interrupting or reducing the quality of service that users expect from payment providers, while the adoption of stablecoins will increase.

2. Improve the enterprise entry process and increase shared incentives

The stablecoin business is becoming more and more mature in bringing end users into the chain by sharing incentives and improving entry solutions.

Entry is becoming cheaper, faster, and more ubiquitous, making it easier for users to get started with cryptocurrencies. At the same time, more and more consumer applications support cryptocurrencies, allowing users to benefit from the expanded stablecoin ecosystem—without adopting new applications or user behaviors. Popular applications such as Venmo, ApplePay, Paypal, CashApp, Nubank, and Revolut allow their customers to use stablecoins.

Moreover, companies are more motivated to use these channels to integrate stablecoins and deposit funds in stablecoins. Fiat-backed stablecoin issuers such as Circle, Paypal, and Tether are sharing profits with ordinary businesses, just as Visa shares profits with United and Chase for signed credit card users. Such cooperation and integration benefit stablecoin issuers because they can create a larger pool of assets to earn returns. But they can also benefit businesses that successfully convert users from credit cards to stablecoins. These businesses can now earn a portion of the revenue generated by the funds their products generate, a business model that is usually only available to banks, fintech companies and gift card issuers that make money from user float.

3. Improve regulatory clarity and availability of compliance solutions

When businesses are confident in the regulatory environment, they are more likely to adopt stablecoins. While we have not yet seen comprehensive global regulation of stablecoins, many jurisdictions have issued rules and guidance on stablecoins, allowing entrepreneurs to start the hard work of building compliant, user-friendly businesses.

For example, the EU's Markets in Crypto-Assets Regulation (MiCA) sets rules for stablecoin issuers, including prudential and behavioral requirements. Since the stablecoin provisions came into effect earlier this year, the regulation has significantly changed the European stablecoin market.

Despite the current lack of a stablecoin framework in the United States, policymakers from both parties are increasingly recognizing the need for effective stablecoin legislation. Such regulation needs to ensure that issuers fully back their tokens with high-quality assets, have their reserves audited by third parties, and take comprehensive measures to combat illegal financial activities. At the same time, legislation needs to preserve the ability of creators to create decentralized stablecoins, reduce user risks by eliminating intermediaries, and take advantage of decentralization.

These policy efforts will get companies across industries to consider moving from traditional payment methods to stablecoin infrastructure. While compliance solutions are unattractive, everyone who adopts stablecoins helps prove to incumbents that stablecoins are a reliable, secure, regulated, and improved solution to traditional payment problems.

As stablecoins gain popularity, the platform’s network effects will grow stronger. While it may still be a few years before stablecoins can be used at point-of-sale or as a replacement for bank accounts, as the number of stablecoin users grows, stablecoin-centric solutions will become more mainstream and more attractive to consumers, businesses, and entrepreneurs.

Trend: Why Stablecoins Will Continue to Improve

As adoption progresses, the product itself will continue to improve. The web3 community is celebrating stablecoin adoption for good reason: stablecoins are climbing the value innovation S-curve thanks to years of investment in infrastructure and on-chain applications. As infrastructure improves, on-chain applications become more abundant, and on-chain networks grow, stablecoins will become more attractive to users. This will happen in two ways.

First, the painstaking engineering of crypto infrastructure has made stablecoin payments of less than a cent possible. Future investments will continue to make transactions cheaper and faster. At the same time, stablecoin aggregation and an improved onboarding experience are only possible through better wallets, bridges, deposits and withdrawals, developer experience, and AMMs.

This technological foundation provides increasing incentives for entrepreneurs to build stablecoins that provide a better developer experience, a rich ecosystem, broad applications, and permissionless composability of on-chain currencies.

Second, stablecoins unlock new user scenarios through the permissionless composability of on-chain currencies. Other payment platforms have gatekeepers that force entrepreneurs to work with extraction networks, such as costly intermediaries in credit card transactions or international payments. But stablecoins are self-custodial and programmable, lowering the threshold for creating new payment experiences and integrating value-added services. Stablecoins are also composable, allowing users to benefit from increasingly powerful on-chain applications and increasing competition. For example, stablecoin users have benefited from DeFi, on-chain subscriptions, and social applications.

Conclusion

Stablecoins can lead us into a world of free, scalable, and instant payments. As Stripe CEO Patrick Collison said, stablecoins are "room temperature superconductors for financial services." They will enable businesses to pursue new opportunities that would otherwise not be able to withstand the burden of existing payment channels or the friction of traditional gatekeepers.

In the short term, stablecoins will have a structural change to financial products as payments become free and open. Incumbent payment companies will seek new ways to monetize, either by taking a percentage of revenue or by selling services that are complementary to this newly commoditized platform. As these traditional businesses recognize the changing landscape, entrepreneurs will create new solutions that help these businesses leverage stablecoins.

In the long run, as stablecoins become more common and the technology advances, startups will seize the opportunities presented by a world of feeless, frictionless, and instant payments. These startups will be founded today, unlocking new and unexpected scenarios and further democratizing the opportunities afforded by the global financial system.

Acknowledgements: Special thanks to Tim Sullivan, Aiden Slavin, Eddy Lazzarin, Robert Hackett, Jay Drain, Liz Harkavy, Miles Jennings, and Scott Kominers for their thoughtful feedback and suggestions that made this article possible.

También te puede interesar

WEEXPERIENCE Whales Night: AI Trading, Crypto Community & Crypto Market Insights

El 12 de diciembre de 2025, WEEX organizó WEEXPERIENCE Whales Night, un encuentro comunitario offline diseñado para reunir a los miembros de la comunidad criptomoneda local. El evento combinó el intercambio de contenido, juegos interactivos y presentaciones de proyectos para crear una experiencia offline relajada pero atractiva.

AI Trading Risk in Cryptocurrency: Why Better Crypto Trading Strategies Can Create Bigger Losses?

El riesgo en long no reside principalmente en una mala toma de decisiones o errores emocionales. Cada vez más en tiempo real en la estructura del mercado, las vías de ejecución y el comportamiento colectivo. Comprender este cambio es más importante que encontrar la próxima estrategia “mejor”.

AI Agents Are Replacing Crypto Research? How Autonomous AI Is Reshaping Crypto Trading

La IA está pasando de asistir trades a automatizar todo el proceso de investigación a ejecución en mercados de criptomonedas. La ventaja cambió de la perspectiva humana a los sistemas de flujos de datos, velocidad y listos para la ejecución, lo que hace que los retrasos en la integración de la IA sean una desventaja competitiva.

AI Trading Bots and Copy Trading: How Synchronized Strategies Reshape Crypto Market Volatility

Los trades minoristas de criptomonedas han enfrentado en long los mismos desafíos: mala gestión de riesgos, entradas tardías, decisiones emocionales y ejecución inconsistente. Las herramientas de tradear de IA prometían una solución. Hoy en día, los sistemas de copy trading potenciados por IA y bots de ruptura ayudan a los trades a dimensionar posiciones, establecer stops y actuar más rápido que nunca. Más allá de velocidad y precisión, estas herramientas están remodelando los mercados silenciosamente: los trades no solo tradean más inteligentemente, sino que se mueven en sincronización, creando una nueva dinámica que amplifica bot riesgo como oportunidad.

AI Trading in Crypto Explained: How Autonomous Trading Is Reshaping Crypto Markets and Crypto Exchanges

AI tradeando está transformando rápidamente el panorama cripto. Las estrategias tradicionales luchan por mantenerse al día con la volatilidad continua de las criptomonedas y su compleja estructura de mercado, mientras que la IA puede procesar datos masivos, generar estrategias adaptativas, gestionar el riesgo y ejecutar trades de forma autónoma. Este artículo guía a los usuarios de WEEX a través de qué es el AI tradear, por qué las criptomonedas acelerar su adopción, cómo evoluciona el sector hacia los agentes autónomos y por qué WEEX está construyendo el ecosistema de tradear de IA de la próxima generación.

Call to Join AI Wars: WEEX Alpha Awakens — Global AI Trading Competition with $880,000 Prize Pool

Ahora, pedimos que trades de IA de todo el mundo se unan a las Guerras de IA: Alpha Awakens de WEEX, una Competencia de trading global de IA con un pool de premios de $880.000.

AI Trading in Crypto Markets: From Automated Trading Bots to Algorithmic Strategies

Tradear impulsado por IA está cambiando las criptomonedas de la especulación minorista a la competencia de nivel institución, donde la ejecución y la gestión de riesgos son más importantes que la dirección. A medida que la IA tradea, aumentan el riesgo sistémico y la presión regulatoria, lo que hace que el rendimiento en long plazo, los sistemas robustos y el cumplimiento sean los diferenciadores clave.

AI Sentiment Analysis and Cryptocurrency Volatility: What Moves Crypto Prices

El sentimiento de IA está influyendo cada vez más en los mercados de criptomonedas, con cambios en las expectativas relacionadas con la IA que se traducen en volatilidad para los principales activos digitales. Los mercados de criptomonedas tienden a amplificar las narrativas de IA, permitiendo que los flujos impulsados por el sentimiento superen a los fundamentales en short plazo. Comprender cómo se forma y spread el sentimiento de IA ayuda a los inversores a anticipar mejor los ciclos de riesgo y las oportunidades de posición en distintos activos digitales.

AI Wars: Guía del participante

En este enfrentamiento definitivo, los mejores desarrolladores, analistas cuantitativos y traders de todo el mundo darán rienda suelta a sus algoritmos desde batallas en el mercado real, compitiendo por uno de los pools de premios más exuberantes en la historia del trading de cripto con IA: 880.000 USD, lo que incluye un Bentley Bentayga S para el campeón. Esta guía te orientará por cada paso que debes dar desde el registro hasta el inicio oficial de la competencia.

Central Bank Week and Crypto Market Volatility: How Interest Rate Decisions Shape Trading Conditions on WEEX

Las decisiones sobre tasas de interés de los principales bancos centrales, como la Reserva Federal, son eventos macroeconómicos importantes que afectan a los mercados financieros mundiales, influyendo directamente en las expectativas de liquidez y el apetito de riesgo del mercado. A medida que el mercado criptomonedas continúa desarrollándose y su estructura tradeando y participantes maduran, el mercado cripto se está incorporando gradualmente al sistema de precios macroeconómicos.

WEEX API Testing: Official Guide for AI Trading Hackathon and Crypto Trading APIs

WEEX API Testing está diseñado para garantizar que cada participante pueda convertir la lógica tradeando en una ejecución real. Todas las interacciones de la API tienen lugar en el sistema tradeando en tiempo real de WEEX, lo que permite que los participantes trabajen en condiciones auténticas del mercado en lugar de simulaciones. Con un requisito de entrada bajo, bot desarrolladores experimentados como principiantes motivados pueden acceder a la tarea, sin dejar de validar las habilidades técnicas esenciales.

Why is WEEX Alpha Awakens the Best AI Trading Competition of 2025? Everything You Need to Know

Para acelerar los avances en la intersección de la IA y las criptomonedas, WEEX lanzar el primer Hackathon de tradear de IA global del mundo: AI Wars: Alpha Despierta. El evento presenta un innovador pool de premios que supera los $880.000, incluyendo un Bentley Bentayga S para el campeón final.

AI Wars: WEEX Alpha Awakens | WEEX Global Hackathon API Test Process Guide

Guerras de IA: El registro de WEEX Alpha Awakens ya está abierto. y esta guía describe cómo acceder a la prueba de API y completar el proceso con éxito.

What is WEEX Alpha Awakens and How to Participate? A Complete Guide

Para acelerar los avances en la intersección de la IA y las criptomonedas, WEEX lanzar el primer Hackathon de tradear de IA global del mundo: AI Wars: Alpha Despierta.

Join AI Wars: WEEX Alpha Awakens!Global Call for AI Trading Alphas

Guerras de IA: WEEX Alpha Awakens es un hackathon global de IA tradeando en Dubái, que llama a equipos cuánticos, trades algorítmicos y desarrolladores de IA para que den rienda suelta a sus estrategias de IA tradeando cripto en mercados en tiempo real por una parte de un pool de premios de US$880.000.

WEEX Unveils Trade to Earn: Up to 30% Instant Rebate + $2M WXT Buyback

WEEX se complace en anunciar el lanza de nuestro programa Tradea para Ganar, que te otorga automáticamente hasta un 30% tradeando cashbacks. Todas las recompensas se crédito directamente en tu cuenta spot en $WXT, con el respaldo de nuestro plan de comprar de $2.000.000 en WXT, que alimenta el valor de los token a en long plazo.

New: Estimated Liquidation Price on App Candlestick Charts

WEEX presentó un nuevo precio de liquidación estimado (Est. Liq. Price) función en el gráfico de velas para ayudar a los trades gestionar mejor el riesgo e identificar rangos seguros para sus posiciones.

WEEX AI Hackathon Guide: Find Your WEEX UID and Register

Desde ahora hasta febrero 2026, WEEX lanza AI Wars: Alpha Awakens de WEEX, el primer hackathon global de IA cripto tradeando. Accede a tu UID y registro para el Hackathon de tradear de IA global de WEEX.

WEEXPERIENCE Whales Night: AI Trading, Crypto Community & Crypto Market Insights

El 12 de diciembre de 2025, WEEX organizó WEEXPERIENCE Whales Night, un encuentro comunitario offline diseñado para reunir a los miembros de la comunidad criptomoneda local. El evento combinó el intercambio de contenido, juegos interactivos y presentaciones de proyectos para crear una experiencia offline relajada pero atractiva.

AI Trading Risk in Cryptocurrency: Why Better Crypto Trading Strategies Can Create Bigger Losses?

El riesgo en long no reside principalmente en una mala toma de decisiones o errores emocionales. Cada vez más en tiempo real en la estructura del mercado, las vías de ejecución y el comportamiento colectivo. Comprender este cambio es más importante que encontrar la próxima estrategia “mejor”.

AI Agents Are Replacing Crypto Research? How Autonomous AI Is Reshaping Crypto Trading

La IA está pasando de asistir trades a automatizar todo el proceso de investigación a ejecución en mercados de criptomonedas. La ventaja cambió de la perspectiva humana a los sistemas de flujos de datos, velocidad y listos para la ejecución, lo que hace que los retrasos en la integración de la IA sean una desventaja competitiva.

AI Trading Bots and Copy Trading: How Synchronized Strategies Reshape Crypto Market Volatility

Los trades minoristas de criptomonedas han enfrentado en long los mismos desafíos: mala gestión de riesgos, entradas tardías, decisiones emocionales y ejecución inconsistente. Las herramientas de tradear de IA prometían una solución. Hoy en día, los sistemas de copy trading potenciados por IA y bots de ruptura ayudan a los trades a dimensionar posiciones, establecer stops y actuar más rápido que nunca. Más allá de velocidad y precisión, estas herramientas están remodelando los mercados silenciosamente: los trades no solo tradean más inteligentemente, sino que se mueven en sincronización, creando una nueva dinámica que amplifica bot riesgo como oportunidad.

AI Trading in Crypto Explained: How Autonomous Trading Is Reshaping Crypto Markets and Crypto Exchanges

AI tradeando está transformando rápidamente el panorama cripto. Las estrategias tradicionales luchan por mantenerse al día con la volatilidad continua de las criptomonedas y su compleja estructura de mercado, mientras que la IA puede procesar datos masivos, generar estrategias adaptativas, gestionar el riesgo y ejecutar trades de forma autónoma. Este artículo guía a los usuarios de WEEX a través de qué es el AI tradear, por qué las criptomonedas acelerar su adopción, cómo evoluciona el sector hacia los agentes autónomos y por qué WEEX está construyendo el ecosistema de tradear de IA de la próxima generación.

Call to Join AI Wars: WEEX Alpha Awakens — Global AI Trading Competition with $880,000 Prize Pool

Ahora, pedimos que trades de IA de todo el mundo se unan a las Guerras de IA: Alpha Awakens de WEEX, una Competencia de trading global de IA con un pool de premios de $880.000.

Monedas populares

Últimas noticias sobre criptomonedas

Atención al cliente:@weikecs

Cooperación empresarial:@weikecs

Trading cuantitativo y MM:[email protected]

Programa VIP:[email protected]