- Acheter crypto

- Marchés

- Futures

- Spot

- Copy trading

WE-Launch

WE-Launch

a16z: How will stablecoins eat into the payments industry? What happens after that?

Original title: How stablecoins will eat payments, and what happens next

Original author: Sam Broner, a16z crypto investment partner

Original translation: 0xjs, Golden Finance

Today's payments landscape is dominated by gatekeepers who charge high fees, undercut the profitability of every business they touch, and justify those fees in the name of ubiquity and convenience — while they stifle competition and limit the creativity of builders.

Stablecoins can do better.

Stablecoins have lower fees, more competition among payment providers, and wider accessibility. Because stablecoins reduce transaction costs to almost zero, they can free businesses from the friction of existing alternatives. Adoption of stablecoins will start with businesses most affected by current payment methods, a process that will disrupt the payments industry.

Stablecoins have become the cheapest way to transfer dollars. Last month, 28.5 million unique stablecoin users sent over 600 million transactions. Stablecoin users are found in nearly every country and use stablecoins because they offer a safe, cheap, and inflation-resistant way to save and spend. Aside from cash and gold, stablecoins are the only widely adopted payment method that can operate without gatekeepers such as banks, payment networks, or central banks. At the same time, stablecoins are permissionless, programmable, scalable, and integrable—anyone can help build a stablecoin payment platform on top of a stablecoin payment rail.

This disruption may take time, but it may happen faster than many expect. Businesses such as restaurants, retailers, enterprises, and payment processors will benefit the most from stablecoin platforms, with significantly higher profit margins. This demand will drive adoption, and as stablecoin adoption continues to increase, the other benefits of stablecoins—permissionless composability and improved programmability—will bring more benefits to on-chain users, businesses, and products. I’ll share more whys and hows below, but first some background on the payments industry.

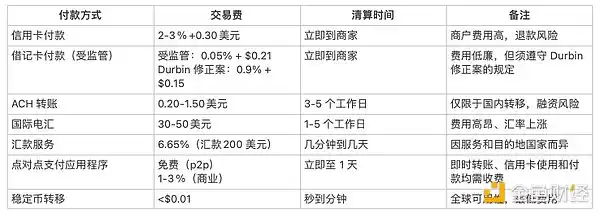

Payment Tracks

• Payment Channels: The technology, rules, and networks that process transactions

• Payment Processors: Operators on the payment rails that facilitate transactions

• Payment Service Providers: Entities that provide access to payment systems to end users or other systems

• Payment Solutions: Products provided by payment service providers

• Payment Platforms: A suite of interrelated payment solutions across providers, processors, and rails

Payments Industry Background

The size of the payments industry cannot be underestimated. In 2023, the global payments industry processed 3.4 trillion transactions worth $1.8 trillion and generated $2.4 trillion in revenue. In the United States alone, credit card payments accounted for $5.6 trillion and debit card payments accounted for $4.4 trillion.

Despite the industry’s ubiquity and scale, payment solutions remain expensive and complex, and payment apps are often shielded from the consumer experience. For example, while peer-to-peer payment app Venmo may look simple on the front end, on the back end, the product hides a maze of bank integrations, debit card vulnerabilities, and countless compliance obligations. Payment solutions are often interdependent, which adds to the complexity, and people still use a variety of payment methods: cash, debit cards, credit cards, peer-to-peer payment apps, ACH (Automated Clearing House), checks, etc.

The four main metrics for payment products are timeliness, cost, reliability, and convenience.

Consumers prioritize questions like “How much will I pay?” Merchants ask “Will I get paid?” But in fact, all four metrics are essential for both parties.

Ever since businesses had to find fraudulent credit cards in physical ledgers, waves of innovation have continuously improved the payment experience. Each wave of innovation has brought faster, more reliable, more convenient, and cheaper payment methods, which in turn has led to an increase in transaction volume and the amount spent.

But many customers are still not enjoying modern services, or are underserved. For merchants, credit cards are expensive, directly eating into their profits. Despite growing adoption of real-time payments (RTP), U.S. bank transfers are still too slow, taking days. And peer-to-peer applications are region- and network-specific, making transfers between ecosystems slow, costly, and complex.

While businesses and consumers have come to expect more sophisticated functionality from payment platforms, not all users benefit from existing solutions. In fact, most users pay too much in fees and don’t use all of the bundled payment products. But they accept the current state of affairs.

Where Stablecoins Fit In

The key to stablecoins disrupting the industry is the failure of existing payment solutions (high cost, low availability, or high friction), and the fact that bundled products of payment solutions (including identity, lending, compliance, fraud protection, and bank integration) are least necessary.

Take remittances as an example. It was born out of desperation. Many remittance users are underbanked and use highly fragmented banking services. As a result, these users see little value in native integrations between traditional payments and banking services. Stablecoin payments offer instant finality, low costs, and no middlemen, which are structural advantages for any payment user or builder. After all, with stablecoins, it costs less than $0.01 to send $200 from the United States to Colombia, but $12.13 on traditional corridors. (Remittance users need to send money home regardless of transaction costs, but will benefit greatly from lower fees.)

International commercial payments, especially for small businesses in emerging markets, also face high fees, slow processing times, and low bank acceptance. For example, a payment between a Mexican apparel manufacturer and a Vietnamese textile manufacturer will involve four or more intermediaries – local bank, foreign exchange, correspondent bank, correspondent bank, foreign exchange, local bank. Each intermediary charges a percentage and there is a risk of middleman bankruptcy.

Fortunately, these transactions occur between partners with a regular relationship. With stablecoins, Mexican payers and Vietnamese payees can experiment and eliminate slow, bureaucratic, and expensive intermediaries. They may have to work hard to find local channels and workflows, but in the end they can enjoy faster, cheaper transactions and more control over the payment process.

Small-value transactions (especially low-fraud face-to-face transactions, such as those conducted in restaurants, coffee shops, or corner stores) are also a promising opportunity. These businesses are cost-sensitive due to their low profit margins, so the 15-cent transaction fee charged by payment solutions has a big impact on their profitability.

For every $2 a customer spends on a cup of coffee, only $1.70 to $1.80 goes to the coffee shop, with the remaining nearly 15% going to the credit card company—just for facilitating the transaction. But credit cards are here for convenience: neither the consumer nor the store needs additional features to justify the charges. Consumers don’t need fraud protection (they’re just getting a cup of coffee) or loans (the coffee was only $2). And coffee shops have limited compliance and bank integration needs (they typically use integrated restaurant management software or none at all). So if there’s a cheap, reliable alternative, these businesses will take advantage of it.

Cheaper Payments Improve Profitability

Current payment system transaction fees directly hurt the bottom line for many businesses. Lowering these fees would provide a huge boost to profitability. The first shoe has already dropped: Stripe announced they will charge 1.5% on stablecoin payments, 30% less than what they charge for credit card payments. To support this effort, Stripe announced the acquisition of Bridge.xyz for approximately $1 billion.

Wider adoption of stablecoins would significantly improve profitability for many businesses—not just small businesses like coffee shops or restaurants. Let’s look at the financials for three public companies in fiscal 2024 to get a rough idea of the impact of reducing payment processing rates to 0.1%. (For simplicity, this assessment assumes that businesses pay a 1.6% hybrid payment processor cost and that on- and off-ramps have minimal costs. More on this below.)

· Walmart, with $648 billion in annual revenue, could pay $10 billion in credit card fees and make $15.5 billion in profit. Do the math: Given the elimination of payment fees and Walmart's profitability, its valuation (controlling for all other factors) could increase by more than 60% just through a cheaper payment solution.

· Chipotle is a fast-growing fast-food restaurant with $9.8 billion in annual revenue. It makes $1.2 billion in profit each year, of which it pays $148 million in credit card fees. Just by reducing fees, Chipotle could increase profitability by 12%—an astonishing number not available elsewhere on its income statement.

· National grocer Krogers has the lowest margins and therefore makes the most money. Surprisingly, Krogers’ net revenue and payment costs may be nearly equal. Like many grocery stores, its profit margin is less than 2%, which is less than the fees businesses pay to process credit card payments. With stablecoin payments, Krogers’ profits could double.

How will Walmart, Chipotle, and Krogers reduce transaction fees with stablecoins? First, consider an idealized scenario: consumers will not accept stablecoins all at once, and there will still be considerable fees until stablecoins gain enough acceptance, especially when starting and stopping use. Second, both retailers and payment processors oppose high-fee payment solutions. Payment processors are also low-margin businesses that give up most of their profits to credit card networks and issuing banks. When payment processors process transactions, most of their fees are passed on to payment networks. So when Stripe handles the online retail checkout process, they take a 2.9% cut of the total transaction and a $0.30 fee, but they pay more than 70% to Visa and the issuing bank. As more payment processors like Block- formerly Square, Fiserv, Stripe, and Toast adopt stablecoins to improve their profit margins, they will make stablecoins more accessible to more businesses.

Stablecoins have low fees and no network gatekeeper fees to pay. This means payment processors earn much higher margins on revenue from stablecoin transactions. Higher margins could lead payment processors to support and encourage more businesses and use cases to use stablecoins. But as payment processors begin to adopt stablecoins, expect stablecoin payment fees to compress over time: Stripe’s 1.5% fee is likely to fall.

Next Steps: Mass Consumer Adoption

Today, stablecoins are a new permissionless way to send and store money. Entrepreneurs are already building solutions to turn stablecoin rails into stablecoin platforms. As with previous innovations, adoption will occur gradually, starting at the fringes of consumer demand, then forward-thinking businesses, until the platform matures enough to meet the needs of everyday users and cautious businesses. Three trends will drive more mainstream enterprise adoption of stablecoins.

1. Increase back-end integration through stablecoin aggregation

Stablecoin aggregation (the ability to monitor, guide, and integrate stablecoins) will soon be integrated into payment processors such as Stripe. These aggregation products enable businesses to process payments at a much lower cost than current mechanisms without major process or engineering changes. Consumers may end up with cheaper products without knowing it, because invoices, payrolls, and subscriptions have lower structural costs by default.

Many of these stablecoin aggregation businesses have begun to attract customers who want instant settlement, low-cost, and widely available business-to-business or business-to-consumer payments. By integrating stablecoins in the backend, businesses will benefit from the advantages of stablecoins—without interrupting or reducing the quality of service that users expect from payment providers, while the adoption of stablecoins will increase.

2. Improve the enterprise entry process and increase shared incentives

The stablecoin business is becoming more and more mature in bringing end users into the chain by sharing incentives and improving entry solutions.

Entry is becoming cheaper, faster, and more ubiquitous, making it easier for users to get started with cryptocurrencies. At the same time, more and more consumer applications support cryptocurrencies, allowing users to benefit from the expanded stablecoin ecosystem—without adopting new applications or user behaviors. Popular applications such as Venmo, ApplePay, Paypal, CashApp, Nubank, and Revolut allow their customers to use stablecoins.

Moreover, companies are more motivated to use these channels to integrate stablecoins and deposit funds in stablecoins. Fiat-backed stablecoin issuers such as Circle, Paypal, and Tether are sharing profits with ordinary businesses, just as Visa shares profits with United and Chase for signed credit card users. Such cooperation and integration benefit stablecoin issuers because they can create a larger pool of assets to earn returns. But they can also benefit businesses that successfully convert users from credit cards to stablecoins. These businesses can now earn a portion of the revenue generated by the funds their products generate, a business model that is usually only available to banks, fintech companies and gift card issuers that make money from user float.

3. Improve regulatory clarity and availability of compliance solutions

When businesses are confident in the regulatory environment, they are more likely to adopt stablecoins. While we have not yet seen comprehensive global regulation of stablecoins, many jurisdictions have issued rules and guidance on stablecoins, allowing entrepreneurs to start the hard work of building compliant, user-friendly businesses.

For example, the EU's Markets in Crypto-Assets Regulation (MiCA) sets rules for stablecoin issuers, including prudential and behavioral requirements. Since the stablecoin provisions came into effect earlier this year, the regulation has significantly changed the European stablecoin market.

Despite the current lack of a stablecoin framework in the United States, policymakers from both parties are increasingly recognizing the need for effective stablecoin legislation. Such regulation needs to ensure that issuers fully back their tokens with high-quality assets, have their reserves audited by third parties, and take comprehensive measures to combat illegal financial activities. At the same time, legislation needs to preserve the ability of creators to create decentralized stablecoins, reduce user risks by eliminating intermediaries, and take advantage of decentralization.

These policy efforts will get companies across industries to consider moving from traditional payment methods to stablecoin infrastructure. While compliance solutions are unattractive, everyone who adopts stablecoins helps prove to incumbents that stablecoins are a reliable, secure, regulated, and improved solution to traditional payment problems.

As stablecoins gain popularity, the platform’s network effects will grow stronger. While it may still be a few years before stablecoins can be used at point-of-sale or as a replacement for bank accounts, as the number of stablecoin users grows, stablecoin-centric solutions will become more mainstream and more attractive to consumers, businesses, and entrepreneurs.

Trend: Why Stablecoins Will Continue to Improve

As adoption progresses, the product itself will continue to improve. The web3 community is celebrating stablecoin adoption for good reason: stablecoins are climbing the value innovation S-curve thanks to years of investment in infrastructure and on-chain applications. As infrastructure improves, on-chain applications become more abundant, and on-chain networks grow, stablecoins will become more attractive to users. This will happen in two ways.

First, the painstaking engineering of crypto infrastructure has made stablecoin payments of less than a cent possible. Future investments will continue to make transactions cheaper and faster. At the same time, stablecoin aggregation and an improved onboarding experience are only possible through better wallets, bridges, deposits and withdrawals, developer experience, and AMMs.

This technological foundation provides increasing incentives for entrepreneurs to build stablecoins that provide a better developer experience, a rich ecosystem, broad applications, and permissionless composability of on-chain currencies.

Second, stablecoins unlock new user scenarios through the permissionless composability of on-chain currencies. Other payment platforms have gatekeepers that force entrepreneurs to work with extraction networks, such as costly intermediaries in credit card transactions or international payments. But stablecoins are self-custodial and programmable, lowering the threshold for creating new payment experiences and integrating value-added services. Stablecoins are also composable, allowing users to benefit from increasingly powerful on-chain applications and increasing competition. For example, stablecoin users have benefited from DeFi, on-chain subscriptions, and social applications.

Conclusion

Stablecoins can lead us into a world of free, scalable, and instant payments. As Stripe CEO Patrick Collison said, stablecoins are "room temperature superconductors for financial services." They will enable businesses to pursue new opportunities that would otherwise not be able to withstand the burden of existing payment channels or the friction of traditional gatekeepers.

In the short term, stablecoins will have a structural change to financial products as payments become free and open. Incumbent payment companies will seek new ways to monetize, either by taking a percentage of revenue or by selling services that are complementary to this newly commoditized platform. As these traditional businesses recognize the changing landscape, entrepreneurs will create new solutions that help these businesses leverage stablecoins.

In the long run, as stablecoins become more common and the technology advances, startups will seize the opportunities presented by a world of feeless, frictionless, and instant payments. These startups will be founded today, unlocking new and unexpected scenarios and further democratizing the opportunities afforded by the global financial system.

Acknowledgements: Special thanks to Tim Sullivan, Aiden Slavin, Eddy Lazzarin, Robert Hackett, Jay Drain, Liz Harkavy, Miles Jennings, and Scott Kominers for their thoughtful feedback and suggestions that made this article possible.

Vous pourriez aussi aimer

WEEXPERIENCE Nuit des baleines : Trading IA, communauté crypto et marché crypto

Le 12 décembre 2025, WEEX a organisé WEEXPERIENCE Whales Night, un rassemblement communautaire hors ligne conçu pour rassembler les membres de la communauté crypto locale. L'événement a combiné le partage de contenu, des jeux interactifs et des présentations de projets pour créer une expérience hors ligne détendue et attrayante.

Risque de trading d'IA en cryptomonnaie : Pourquoi de meilleures stratégies de trading crypto peuvent-elles générer des pertes plus importantes ?

Le risque ne réside plus principalement dans une mauvaise prise de décision ou des erreurs émotionnelles. Il vit de plus en plus dans la structure du marché, les parcours d'exécution et le comportement collectif. Comprendre ce changement est plus important que de trouver la prochaine stratégie « meilleure ».

Les agents de l'IA remplacent-ils la recherche crypto ? Comment l'IA autonome remodele le trading crypto

L'IA passe de l'assistance aux traders à l'automatisation de l'ensemble du processus de recherche à l'exécution sur les marchés crypto. L'avantage est passé de l'information humaine aux pipelines de données, à la vitesse et aux systèmes d'IA prêts à être exécutés, ce qui fait des retards dans l'intégration de l'IA un désavantage concurrentiel.

Boots de trading et copy trading IA : Comment les stratégies synchronisées remodèlent la volatilité du marché crypto

Les traders crypto de détail sont confrontés depuis longtemps aux mêmes défis : mauvaise gestion des risques, entrées tardives, décisions émotionnelles et exécution incohérente. Les outils de trading IA promettaient une solution. Aujourd'hui, les systèmes de copy trading et les bots de cassage alimentés par l'IA aident les traders à dimensionner leurs positions, à définir des stops et à agir plus rapidement que jamais. Au-delà de la vitesse et de la précision, ces outils remodèlent tranquillement les marchés : les traders ne tradent pas seulement plus malin, ils évoluent de façon synchronisée, créant une nouvelle dynamique qui amplifie à la fois les risques et les opportunités.

Le trading d'IA en crypto expliqué : Comment le trading autonome remodele les marchés crypto et les plateformes d’échange crypto

L’IA Trading transforme rapidement le paysage crypto. Les stratégies traditionnelles peinent à suivre la volatilité constante de la crypto et la structure complexe du marché, tandis que l'IA peut traiter des données massives, générer des stratégies adaptatives, gérer les risques et exécuter des trades de manière autonome. Cet article guide les utilisateurs de WEEX sur ce qu'est le trading d'IA, pourquoi la crypto accélère son adoption, comment le secteur évolue vers des agents autonomes et pourquoi WEEX construit l'écosystème de trading d'IA de nouvelle génération.

Appelez à rejoindre AI Wars : WEEX Alpha Awakens – Tournoi mondial de trading d’IA avec une cagnotte de 880 000 $

Maintenant, nous lançons un appel aux traders d'IA du monde entier pour qu'ils rejoignent AI Wars : WEEX Alpha Awakens, un tournoi mondial de trading d'IA doté d'une cagnotte de 880 000 $.

Trading d'IA sur les marchés crypto : Des bots de trading automatisés aux stratégies algorithmiques

Le trading basé sur l'IA fait passer la crypto de la spéculation au détail à une concurrence de niveau institutionnel, où l'exécution et la gestion des risques comptent plus que dans le sens. À mesure que le trading de l'IA prend de l'ampleur, les risques systémiques et la pression réglementaire augmentent, faisant des performances à long terme, des systèmes robustes et de la conformité les principaux facteurs de différenciation.

Analyse du sentiment de l'IA et volatilité des cryptomonnaies : Ce qui fait bouger les prix crypto

Le sentiment lié à l'IA influence de plus en plus les marchés crypto, les changements d'attente liés à l'IA se traduisant par une certaine volatilité pour les principaux actifs numériques. Les marchés crypto ont tendance à amplifier les discours sur l'IA, permettant aux flux basés sur les sentiments de l'emporter sur les fondamentaux à court terme. Comprendre comment le sentiment IA se forme et se propage aide les investisseurs à mieux anticiper les cycles de risque et les opportunités de positionnement sur les actifs numériques.

Guerres de l'IA : Guide du participant

Dans cette confrontation ultime, les meilleurs développeurs, quants et traders du monde entier déploieront leurs algorithmes dans des batailles sur le marché réel, en compétition pour l'un des prix les plus importants de l'histoire du trading crypto basé sur l'IA : 880 000 dollars américains, dont une Bentley Bentayga S pour le champion. Ce guide vous accompagnera à travers toutes les étapes nécessaires, de l'inscription au début officiel de la compétition.

Semaine des banques centrales et volatilité des marchés crypto : Comment les décisions relatives aux taux d'intérêt influencent les conditions de trading sur WEEX

Les décisions relatives aux taux d'intérêt prises par les grandes banques centrales, comme la Réserve fédérale, sont des événements macroéconomiques importants qui ont un impact sur les marchés financiers mondiaux et influencent directement les attentes de liquidité des marchés et l'appétence au risque. À mesure que le marché des cryptomonnaies continue de se développer et que sa structure de trading et ses participants mûrissent, le marché des cryptomonnaies est progressivement intégré dans le système d'établissement des prix macroéconomiques.

Test de l'API WEEX : Guide officiel des API de trading de Hackathon et de Crypto pour le trading d’IA

WEEX API Testing est conçu pour garantir que chaque participant peut transformer la logique de trading en exécution réelle. Toutes les interactions API ont lieu sur le système de trading en direct de WEEX, ce qui permet aux participants de travailler dans des conditions de marché authentiques plutôt que dans des simulations. Avec une faible exigence d'entrée, la tâche est accessible à la fois aux développeurs expérimentés et aux débutants motivés, tout en validant les compétences techniques essentielles.

Pourquoi WEEX Alpha se réveille-t-il le meilleur tournoi de trading d'IA de 2025 ? Tout ce que vous devez savoir

Pour accélérer les percées à l'intersection de l'IA et de la crypto, WEEX lance le premier Hackathon mondial de trading d'IA – AI Wars: Alpha se réveille. L'événement propose une cagnotte révolutionnaire dépassant 880 000 $, dont une Bentley Bentayga S pour le champion ultime.

AI Wars: WEEX Alpha Awakens | Guide des processus de test de l'API WEEX Global Hackathon

AI Wars : L'inscription au Réveil Alpha WEEX est maintenant ouverte. Ce guide explique comment accéder au test API et terminer le processus avec succès.

Qu'est-ce que le réveil de WEEX Alpha et comment participer ? Un guide complet

Pour accélérer les percées à l'intersection de l'IA et de la crypto, WEEX lance le premier Hackathon mondial de trading d'IA – AI Wars: Alpha se réveille.

Join AI Wars: WEEK Alpha se réveille !Appel mondial pour les Alphas de Trading IA

AI Wars: WEEX Alpha Awakens est un hackathon mondial de trading sur l'IA à Dubaï, appelant les équipes quantiques, les traders algorithmiques et les développeurs d'IA à lancer leurs stratégies de trading crypto sur les marchés en direct pour une part d'une cagnotte de 880 000 $ US.

WEEX dévoile le trade to Earn: Jusqu'à 30 % de remise instantanée + 2 M$ WXT Rachat

WEEX est heureuse d’annoncer le lancement de son programme Trade to Earn, qui vous accorde automatiquement jusqu’à 30% de rabais sur les frais de trading. Toutes les récompenses sont créditées directement sur votre compte au comptant en WXT $, soutenu par notre plan de rachat de WXT $2,000,000 qui alimente la valeur à long terme des jetons.

Nouveau: Prix de liquidation estimé sur les graphiques App Candlestick

WEEX a introduit un nouveau prix estimatif de liquidation (Est. Liq. Price) figure sur le graphique en chandelier pour aider les traders à mieux gérer le risque et à identifier des fourchettes sûres pour leurs positions.

WEEX AI Hackathon Guide: Trouvez votre UID WEEK et inscrivez-vous

D'ici février 2026, WEEX lance AI Wars: WEEK Alpha Awakens, le premier hackathon mondial de trading de crypto-IA. Venez votre UID et inscrivez-vous au WEEX Global AI Trading Hackathon.

WEEXPERIENCE Nuit des baleines : Trading IA, communauté crypto et marché crypto

Le 12 décembre 2025, WEEX a organisé WEEXPERIENCE Whales Night, un rassemblement communautaire hors ligne conçu pour rassembler les membres de la communauté crypto locale. L'événement a combiné le partage de contenu, des jeux interactifs et des présentations de projets pour créer une expérience hors ligne détendue et attrayante.

Risque de trading d'IA en cryptomonnaie : Pourquoi de meilleures stratégies de trading crypto peuvent-elles générer des pertes plus importantes ?

Le risque ne réside plus principalement dans une mauvaise prise de décision ou des erreurs émotionnelles. Il vit de plus en plus dans la structure du marché, les parcours d'exécution et le comportement collectif. Comprendre ce changement est plus important que de trouver la prochaine stratégie « meilleure ».

Les agents de l'IA remplacent-ils la recherche crypto ? Comment l'IA autonome remodele le trading crypto

L'IA passe de l'assistance aux traders à l'automatisation de l'ensemble du processus de recherche à l'exécution sur les marchés crypto. L'avantage est passé de l'information humaine aux pipelines de données, à la vitesse et aux systèmes d'IA prêts à être exécutés, ce qui fait des retards dans l'intégration de l'IA un désavantage concurrentiel.

Boots de trading et copy trading IA : Comment les stratégies synchronisées remodèlent la volatilité du marché crypto

Les traders crypto de détail sont confrontés depuis longtemps aux mêmes défis : mauvaise gestion des risques, entrées tardives, décisions émotionnelles et exécution incohérente. Les outils de trading IA promettaient une solution. Aujourd'hui, les systèmes de copy trading et les bots de cassage alimentés par l'IA aident les traders à dimensionner leurs positions, à définir des stops et à agir plus rapidement que jamais. Au-delà de la vitesse et de la précision, ces outils remodèlent tranquillement les marchés : les traders ne tradent pas seulement plus malin, ils évoluent de façon synchronisée, créant une nouvelle dynamique qui amplifie à la fois les risques et les opportunités.

Le trading d'IA en crypto expliqué : Comment le trading autonome remodele les marchés crypto et les plateformes d’échange crypto

L’IA Trading transforme rapidement le paysage crypto. Les stratégies traditionnelles peinent à suivre la volatilité constante de la crypto et la structure complexe du marché, tandis que l'IA peut traiter des données massives, générer des stratégies adaptatives, gérer les risques et exécuter des trades de manière autonome. Cet article guide les utilisateurs de WEEX sur ce qu'est le trading d'IA, pourquoi la crypto accélère son adoption, comment le secteur évolue vers des agents autonomes et pourquoi WEEX construit l'écosystème de trading d'IA de nouvelle génération.

Appelez à rejoindre AI Wars : WEEX Alpha Awakens – Tournoi mondial de trading d’IA avec une cagnotte de 880 000 $

Maintenant, nous lançons un appel aux traders d'IA du monde entier pour qu'ils rejoignent AI Wars : WEEX Alpha Awakens, un tournoi mondial de trading d'IA doté d'une cagnotte de 880 000 $.

Pièces populaires

Dernières actus crypto

Assistance client:@weikecs

Collaborations commerciales:@weikecs

Trading quantitatif/Market makers:[email protected]

Programme VIP:[email protected]