- Acheter crypto

- Marchés

- Futures

- Spot

- Copy trading

WE-Launch

WE-Launch

Web3 New Tale of Two Cities: Stablecoins and Money Market Funds

Original Article Title: Stablecoins and the parallels with Money Market Funds

Original Article Authors: @shawnwlim, @artichokecap Founders

Original Article Translation: zhouzhou, BlockBeats

Editor's Note: The regulatory dispute over stablecoins bears resemblance to the experience of Money Market Funds (MMFs) half a century ago. MMFs were initially designed for corporate cash management but faced criticism due to lack of deposit insurance and vulnerability to runs, impacting bank stability and monetary policy. Nevertheless, MMF assets now exceed $7.2 trillion. The 2008 financial crisis led to the collapse of the Reserve Fund, and in 2023, the SEC is still pushing for MMF regulatory reform. The history of MMFs suggests that stablecoins may face similar regulatory challenges but could ultimately become a crucial part of the financial system.

The following is the original content (slightly edited for readability):

Stablecoins are exciting, and the upcoming stablecoin legislation in the US represents a rare opportunity to upgrade the existing financial system. Those studying financial history will notice parallels between it and the invention and development of Money Market Funds about half a century ago.

Money Market Funds were invented in the 1970s as a cash management solution, primarily for corporates. At that time, US banks were prohibited from paying interest on balances in checking accounts, and corporations were often unable to maintain savings accounts. If a business wanted to earn interest on idle cash, they had to buy US Treasuries, engage in repurchase agreements, invest in commercial paper, or certificates of deposit. Managing cash was a cumbersome and operationally intensive process.

The design of Money Market Funds was to maintain a stable share value, with each share pegged at $1. The Reserve Fund, Inc. was the first MMF. Launched in 1971, it was introduced as "a convenient alternative for investing temporary cash balances," which would typically be placed in money market instruments like Treasuries, commercial paper, bank acceptances, or CDs, with an initial asset size of $1 million.

Other investment giants quickly followed suit: Dreyfus (now part of BNYglobal), Fidelity, Vanguard_Group. In the 1980s, almost half of Vanguard's legendary mutual fund business growth was attributable to its Money Market Fund.

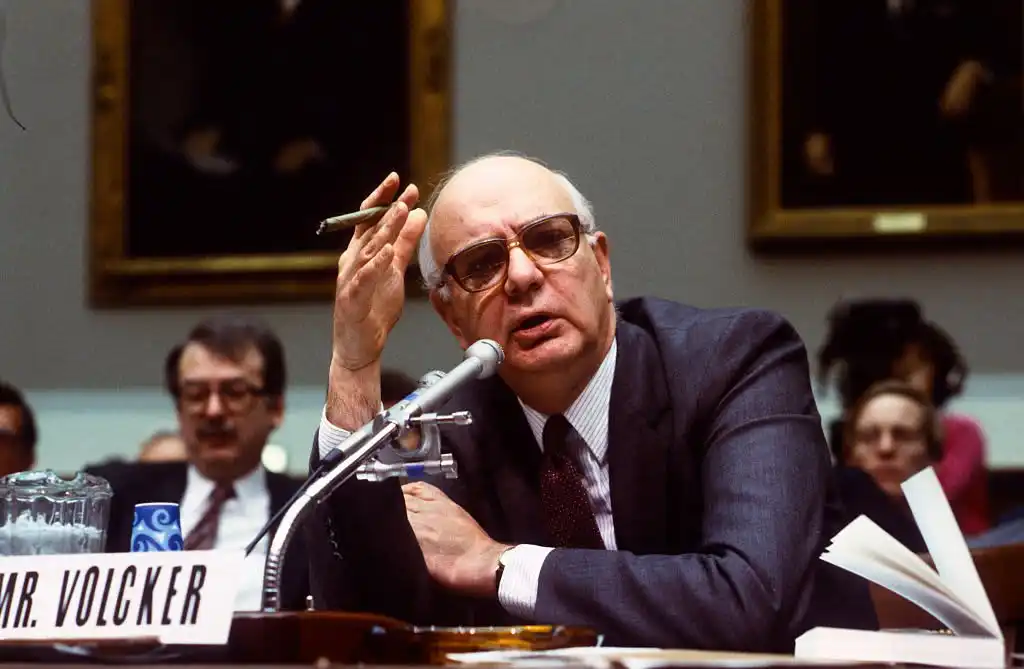

During his tenure as Chairman of the Federal Reserve from 1979 to 1987, Paul Volcker was highly critical of Money Market Funds (MMFs). He continued his criticism of MMFs as late as 2011.

Today, many of the criticisms raised by policymakers against stablecoins echo those from half a century ago against Money Market Funds:

· Systemic Risk and Banking Safety Concerns: MMFs lack deposit insurance and a lender of last resort mechanism, unlike insured banks. Because of this, MMFs are susceptible to rapid runs, which could exacerbate financial instability and lead to contagion. There are also concerns that deposits shifting from insured banks to MMFs could weaken the banking sector as banks lose their low-cost and stable deposit base.

· Unfair Regulatory Arbitrage: MMFs provide bank-like services, maintaining a stable $1 share price, but without rigorous regulatory oversight or capital requirements.

· Weakening of Monetary Policy Transmission Mechanism: MMFs could weaken the Fed's monetary policy tools, as traditional monetary policy instruments like bank reserves are less effective when funds flow from banks to MMFs.

Today, MMFs have financial assets exceeding $7.2 trillion. For reference, M2 (excluding MMF assets) is $21.7 trillion.

In the late 1990s, the rapid growth in MMF assets was a result of financial deregulation (the Gramm-Leach-Bliley Act repealed the Glass-Steagall Act, fueling a wave of financial innovation), while the prosperity of the internet facilitated better electronic and online trading systems, speeding up fund inflows into MMFs.

Do you see a pattern here? (I would like to point out that even half a century later, the regulatory struggle around MMFs is far from over. The SEC adopted MMF reforms in 2023, including raising minimum liquidity requirements and removing fund manager restrictions on investor redemptions.)

Unfortunately, the Reserve Fund met its end after the 2008 financial crisis. It held some Lehman Brothers debt securities, which were written down to zero, leading to the fund's breaking of the buck event and significant redemptions.

Vous pourriez aussi aimer

WEEXPERIENCE Nuit des baleines : Trading IA, communauté crypto et marché crypto

Le 12 décembre 2025, WEEX a organisé WEEXPERIENCE Whales Night, un rassemblement communautaire hors ligne conçu pour rassembler les membres de la communauté crypto locale. L'événement a combiné le partage de contenu, des jeux interactifs et des présentations de projets pour créer une expérience hors ligne détendue et attrayante.

Risque de trading d'IA en cryptomonnaie : Pourquoi de meilleures stratégies de trading crypto peuvent-elles générer des pertes plus importantes ?

Le risque ne réside plus principalement dans une mauvaise prise de décision ou des erreurs émotionnelles. Il vit de plus en plus dans la structure du marché, les parcours d'exécution et le comportement collectif. Comprendre ce changement est plus important que de trouver la prochaine stratégie « meilleure ».

Les agents de l'IA remplacent-ils la recherche crypto ? Comment l'IA autonome remodele le trading crypto

L'IA passe de l'assistance aux traders à l'automatisation de l'ensemble du processus de recherche à l'exécution sur les marchés crypto. L'avantage est passé de l'information humaine aux pipelines de données, à la vitesse et aux systèmes d'IA prêts à être exécutés, ce qui fait des retards dans l'intégration de l'IA un désavantage concurrentiel.

Boots de trading et copy trading IA : Comment les stratégies synchronisées remodèlent la volatilité du marché crypto

Les traders crypto de détail sont confrontés depuis longtemps aux mêmes défis : mauvaise gestion des risques, entrées tardives, décisions émotionnelles et exécution incohérente. Les outils de trading IA promettaient une solution. Aujourd'hui, les systèmes de copy trading et les bots de cassage alimentés par l'IA aident les traders à dimensionner leurs positions, à définir des stops et à agir plus rapidement que jamais. Au-delà de la vitesse et de la précision, ces outils remodèlent tranquillement les marchés : les traders ne tradent pas seulement plus malin, ils évoluent de façon synchronisée, créant une nouvelle dynamique qui amplifie à la fois les risques et les opportunités.

Le trading d'IA en crypto expliqué : Comment le trading autonome remodele les marchés crypto et les plateformes d’échange crypto

L’IA Trading transforme rapidement le paysage crypto. Les stratégies traditionnelles peinent à suivre la volatilité constante de la crypto et la structure complexe du marché, tandis que l'IA peut traiter des données massives, générer des stratégies adaptatives, gérer les risques et exécuter des trades de manière autonome. Cet article guide les utilisateurs de WEEX sur ce qu'est le trading d'IA, pourquoi la crypto accélère son adoption, comment le secteur évolue vers des agents autonomes et pourquoi WEEX construit l'écosystème de trading d'IA de nouvelle génération.

Appelez à rejoindre AI Wars : WEEX Alpha Awakens – Tournoi mondial de trading d’IA avec une cagnotte de 880 000 $

Maintenant, nous lançons un appel aux traders d'IA du monde entier pour qu'ils rejoignent AI Wars : WEEX Alpha Awakens, un tournoi mondial de trading d'IA doté d'une cagnotte de 880 000 $.

Trading d'IA sur les marchés crypto : Des bots de trading automatisés aux stratégies algorithmiques

Le trading basé sur l'IA fait passer la crypto de la spéculation au détail à une concurrence de niveau institutionnel, où l'exécution et la gestion des risques comptent plus que dans le sens. À mesure que le trading de l'IA prend de l'ampleur, les risques systémiques et la pression réglementaire augmentent, faisant des performances à long terme, des systèmes robustes et de la conformité les principaux facteurs de différenciation.

Analyse du sentiment de l'IA et volatilité des cryptomonnaies : Ce qui fait bouger les prix crypto

Le sentiment lié à l'IA influence de plus en plus les marchés crypto, les changements d'attente liés à l'IA se traduisant par une certaine volatilité pour les principaux actifs numériques. Les marchés crypto ont tendance à amplifier les discours sur l'IA, permettant aux flux basés sur les sentiments de l'emporter sur les fondamentaux à court terme. Comprendre comment le sentiment IA se forme et se propage aide les investisseurs à mieux anticiper les cycles de risque et les opportunités de positionnement sur les actifs numériques.

Guerres de l'IA : Guide du participant

Dans cette confrontation ultime, les meilleurs développeurs, quants et traders du monde entier déploieront leurs algorithmes dans des batailles sur le marché réel, en compétition pour l'un des prix les plus importants de l'histoire du trading crypto basé sur l'IA : 880 000 dollars américains, dont une Bentley Bentayga S pour le champion. Ce guide vous accompagnera à travers toutes les étapes nécessaires, de l'inscription au début officiel de la compétition.

Semaine des banques centrales et volatilité des marchés crypto : Comment les décisions relatives aux taux d'intérêt influencent les conditions de trading sur WEEX

Les décisions relatives aux taux d'intérêt prises par les grandes banques centrales, comme la Réserve fédérale, sont des événements macroéconomiques importants qui ont un impact sur les marchés financiers mondiaux et influencent directement les attentes de liquidité des marchés et l'appétence au risque. À mesure que le marché des cryptomonnaies continue de se développer et que sa structure de trading et ses participants mûrissent, le marché des cryptomonnaies est progressivement intégré dans le système d'établissement des prix macroéconomiques.

Test de l'API WEEX : Guide officiel des API de trading de Hackathon et de Crypto pour le trading d’IA

WEEX API Testing est conçu pour garantir que chaque participant peut transformer la logique de trading en exécution réelle. Toutes les interactions API ont lieu sur le système de trading en direct de WEEX, ce qui permet aux participants de travailler dans des conditions de marché authentiques plutôt que dans des simulations. Avec une faible exigence d'entrée, la tâche est accessible à la fois aux développeurs expérimentés et aux débutants motivés, tout en validant les compétences techniques essentielles.

Pourquoi WEEX Alpha se réveille-t-il le meilleur tournoi de trading d'IA de 2025 ? Tout ce que vous devez savoir

Pour accélérer les percées à l'intersection de l'IA et de la crypto, WEEX lance le premier Hackathon mondial de trading d'IA – AI Wars: Alpha se réveille. L'événement propose une cagnotte révolutionnaire dépassant 880 000 $, dont une Bentley Bentayga S pour le champion ultime.

AI Wars: WEEX Alpha Awakens | Guide des processus de test de l'API WEEX Global Hackathon

AI Wars : L'inscription au Réveil Alpha WEEX est maintenant ouverte. Ce guide explique comment accéder au test API et terminer le processus avec succès.

Qu'est-ce que le réveil de WEEX Alpha et comment participer ? Un guide complet

Pour accélérer les percées à l'intersection de l'IA et de la crypto, WEEX lance le premier Hackathon mondial de trading d'IA – AI Wars: Alpha se réveille.

Join AI Wars: WEEK Alpha se réveille !Appel mondial pour les Alphas de Trading IA

AI Wars: WEEX Alpha Awakens est un hackathon mondial de trading sur l'IA à Dubaï, appelant les équipes quantiques, les traders algorithmiques et les développeurs d'IA à lancer leurs stratégies de trading crypto sur les marchés en direct pour une part d'une cagnotte de 880 000 $ US.

WEEX dévoile le trade to Earn: Jusqu'à 30 % de remise instantanée + 2 M$ WXT Rachat

WEEX est heureuse d’annoncer le lancement de son programme Trade to Earn, qui vous accorde automatiquement jusqu’à 30% de rabais sur les frais de trading. Toutes les récompenses sont créditées directement sur votre compte au comptant en WXT $, soutenu par notre plan de rachat de WXT $2,000,000 qui alimente la valeur à long terme des jetons.

Nouveau: Prix de liquidation estimé sur les graphiques App Candlestick

WEEX a introduit un nouveau prix estimatif de liquidation (Est. Liq. Price) figure sur le graphique en chandelier pour aider les traders à mieux gérer le risque et à identifier des fourchettes sûres pour leurs positions.

WEEX AI Hackathon Guide: Trouvez votre UID WEEK et inscrivez-vous

D'ici février 2026, WEEX lance AI Wars: WEEK Alpha Awakens, le premier hackathon mondial de trading de crypto-IA. Venez votre UID et inscrivez-vous au WEEX Global AI Trading Hackathon.

WEEXPERIENCE Nuit des baleines : Trading IA, communauté crypto et marché crypto

Le 12 décembre 2025, WEEX a organisé WEEXPERIENCE Whales Night, un rassemblement communautaire hors ligne conçu pour rassembler les membres de la communauté crypto locale. L'événement a combiné le partage de contenu, des jeux interactifs et des présentations de projets pour créer une expérience hors ligne détendue et attrayante.

Risque de trading d'IA en cryptomonnaie : Pourquoi de meilleures stratégies de trading crypto peuvent-elles générer des pertes plus importantes ?

Le risque ne réside plus principalement dans une mauvaise prise de décision ou des erreurs émotionnelles. Il vit de plus en plus dans la structure du marché, les parcours d'exécution et le comportement collectif. Comprendre ce changement est plus important que de trouver la prochaine stratégie « meilleure ».

Les agents de l'IA remplacent-ils la recherche crypto ? Comment l'IA autonome remodele le trading crypto

L'IA passe de l'assistance aux traders à l'automatisation de l'ensemble du processus de recherche à l'exécution sur les marchés crypto. L'avantage est passé de l'information humaine aux pipelines de données, à la vitesse et aux systèmes d'IA prêts à être exécutés, ce qui fait des retards dans l'intégration de l'IA un désavantage concurrentiel.

Boots de trading et copy trading IA : Comment les stratégies synchronisées remodèlent la volatilité du marché crypto

Les traders crypto de détail sont confrontés depuis longtemps aux mêmes défis : mauvaise gestion des risques, entrées tardives, décisions émotionnelles et exécution incohérente. Les outils de trading IA promettaient une solution. Aujourd'hui, les systèmes de copy trading et les bots de cassage alimentés par l'IA aident les traders à dimensionner leurs positions, à définir des stops et à agir plus rapidement que jamais. Au-delà de la vitesse et de la précision, ces outils remodèlent tranquillement les marchés : les traders ne tradent pas seulement plus malin, ils évoluent de façon synchronisée, créant une nouvelle dynamique qui amplifie à la fois les risques et les opportunités.

Le trading d'IA en crypto expliqué : Comment le trading autonome remodele les marchés crypto et les plateformes d’échange crypto

L’IA Trading transforme rapidement le paysage crypto. Les stratégies traditionnelles peinent à suivre la volatilité constante de la crypto et la structure complexe du marché, tandis que l'IA peut traiter des données massives, générer des stratégies adaptatives, gérer les risques et exécuter des trades de manière autonome. Cet article guide les utilisateurs de WEEX sur ce qu'est le trading d'IA, pourquoi la crypto accélère son adoption, comment le secteur évolue vers des agents autonomes et pourquoi WEEX construit l'écosystème de trading d'IA de nouvelle génération.

Appelez à rejoindre AI Wars : WEEX Alpha Awakens – Tournoi mondial de trading d’IA avec une cagnotte de 880 000 $

Maintenant, nous lançons un appel aux traders d'IA du monde entier pour qu'ils rejoignent AI Wars : WEEX Alpha Awakens, un tournoi mondial de trading d'IA doté d'une cagnotte de 880 000 $.

Pièces populaires

Dernières actus crypto

Assistance client:@weikecs

Collaborations commerciales:@weikecs

Trading quantitatif/Market makers:[email protected]

Programme VIP:[email protected]