- Acquista crypto

- Mercato

- Futures

- Spot

- Copy trading

WE-Launch

WE-Launch

Web3 New Tale of Two Cities: Stablecoins and Money Market Funds

Original Article Title: Stablecoins and the parallels with Money Market Funds

Original Article Authors: @shawnwlim, @artichokecap Founders

Original Article Translation: zhouzhou, BlockBeats

Editor's Note: The regulatory dispute over stablecoins bears resemblance to the experience of Money Market Funds (MMFs) half a century ago. MMFs were initially designed for corporate cash management but faced criticism due to lack of deposit insurance and vulnerability to runs, impacting bank stability and monetary policy. Nevertheless, MMF assets now exceed $7.2 trillion. The 2008 financial crisis led to the collapse of the Reserve Fund, and in 2023, the SEC is still pushing for MMF regulatory reform. The history of MMFs suggests that stablecoins may face similar regulatory challenges but could ultimately become a crucial part of the financial system.

The following is the original content (slightly edited for readability):

Stablecoins are exciting, and the upcoming stablecoin legislation in the US represents a rare opportunity to upgrade the existing financial system. Those studying financial history will notice parallels between it and the invention and development of Money Market Funds about half a century ago.

Money Market Funds were invented in the 1970s as a cash management solution, primarily for corporates. At that time, US banks were prohibited from paying interest on balances in checking accounts, and corporations were often unable to maintain savings accounts. If a business wanted to earn interest on idle cash, they had to buy US Treasuries, engage in repurchase agreements, invest in commercial paper, or certificates of deposit. Managing cash was a cumbersome and operationally intensive process.

The design of Money Market Funds was to maintain a stable share value, with each share pegged at $1. The Reserve Fund, Inc. was the first MMF. Launched in 1971, it was introduced as "a convenient alternative for investing temporary cash balances," which would typically be placed in money market instruments like Treasuries, commercial paper, bank acceptances, or CDs, with an initial asset size of $1 million.

Other investment giants quickly followed suit: Dreyfus (now part of BNYglobal), Fidelity, Vanguard_Group. In the 1980s, almost half of Vanguard's legendary mutual fund business growth was attributable to its Money Market Fund.

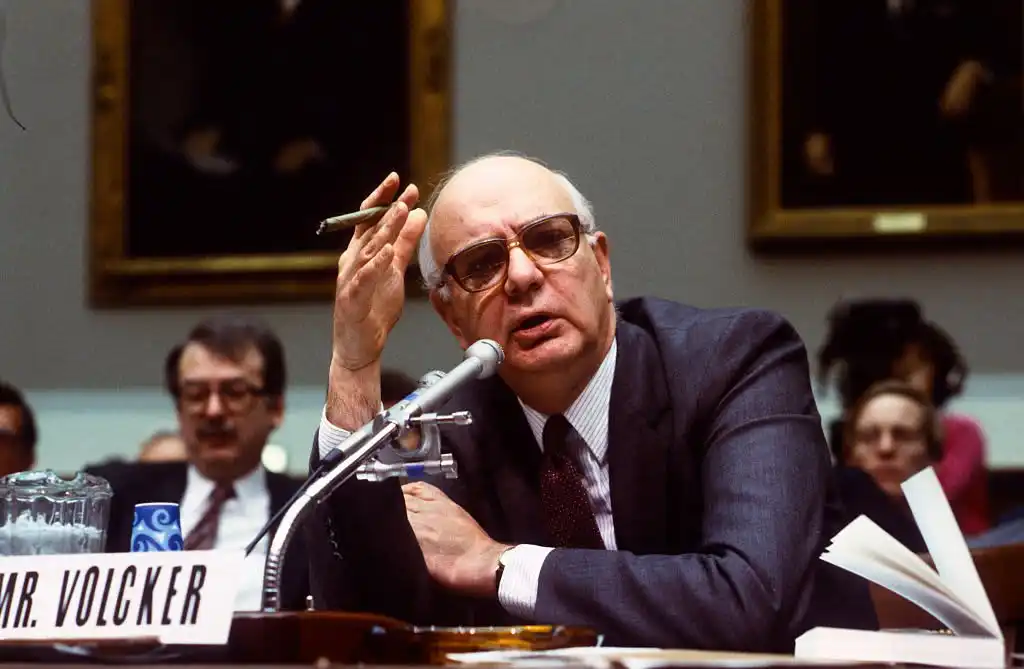

During his tenure as Chairman of the Federal Reserve from 1979 to 1987, Paul Volcker was highly critical of Money Market Funds (MMFs). He continued his criticism of MMFs as late as 2011.

Today, many of the criticisms raised by policymakers against stablecoins echo those from half a century ago against Money Market Funds:

· Systemic Risk and Banking Safety Concerns: MMFs lack deposit insurance and a lender of last resort mechanism, unlike insured banks. Because of this, MMFs are susceptible to rapid runs, which could exacerbate financial instability and lead to contagion. There are also concerns that deposits shifting from insured banks to MMFs could weaken the banking sector as banks lose their low-cost and stable deposit base.

· Unfair Regulatory Arbitrage: MMFs provide bank-like services, maintaining a stable $1 share price, but without rigorous regulatory oversight or capital requirements.

· Weakening of Monetary Policy Transmission Mechanism: MMFs could weaken the Fed's monetary policy tools, as traditional monetary policy instruments like bank reserves are less effective when funds flow from banks to MMFs.

Today, MMFs have financial assets exceeding $7.2 trillion. For reference, M2 (excluding MMF assets) is $21.7 trillion.

In the late 1990s, the rapid growth in MMF assets was a result of financial deregulation (the Gramm-Leach-Bliley Act repealed the Glass-Steagall Act, fueling a wave of financial innovation), while the prosperity of the internet facilitated better electronic and online trading systems, speeding up fund inflows into MMFs.

Do you see a pattern here? (I would like to point out that even half a century later, the regulatory struggle around MMFs is far from over. The SEC adopted MMF reforms in 2023, including raising minimum liquidity requirements and removing fund manager restrictions on investor redemptions.)

Unfortunately, the Reserve Fund met its end after the 2008 financial crisis. It held some Lehman Brothers debt securities, which were written down to zero, leading to the fund's breaking of the buck event and significant redemptions.

Potrebbe interessarti anche

NOTTE DELLE BALene: AI Trading, Crypto Community & Crypto Market Insights

Il 12 dicembre 2025, WEEX ha ospitato WEEXPERIENCE Whales Night, un incontro della comunità offline progettato per riunire i membri della comunità locale di criptovalute. L'evento ha combinato condivisione di contenuti, giochi interattivi e presentazioni di progetti per creare un'esperienza offline rilassata ma coinvolgente.

Rischio di trading AI in criptovaluta: Perché migliori strategie di trading di criptovalute possono creare perdite maggiori?

Il rischio non risiede più principalmente in un cattivo processo decisionale o in errori emotivi. Vive sempre più nella struttura del mercato, nei percorsi di esecuzione e nel comportamento collettivo. Capire questo cambiamento conta più che trovare la prossima strategia “migliore”.

Gli agenti AI stanno sostituendo la ricerca sulle criptovalute? Come l'IA autonoma sta rimodellando il trading di criptovalute

L'IA sta passando dall'assistenza ai trader all'automazione dell'intero processo di ricerca-esecuzione nei mercati crypto. L'edge si è spostato dall'intuito umano alle pipeline di dati, alla velocità e ai sistemi AI pronti per l'esecuzione, rendendo i ritardi nell'integrazione dell'IA uno svantaggio competitivo.

AI Trading Bots e Copy Trading: Come le strategie sincronizzate rimodellano la volatilità del mercato delle criptovalute

I trader di criptovalute al dettaglio affrontano da tempo le stesse sfide: cattiva gestione del rischio, ingressi tardivi, decisioni emotive ed esecuzione incoerente. Gli strumenti di trading AI promettevano una soluzione. Oggi, i sistemi di copy trading e i breakout bot basati sull'IA aiutano i trader a dimensionare le posizioni, impostare stop e agire più velocemente che mai. Al di là di velocità e precisione, questi strumenti stanno tranquillamente rimodellando i mercati: i trader non solo fanno trading in modo più intelligente, ma si muovono in sincronia, creando una nuova dinamica che amplifica sia il rischio che le opportunità.

AI Trading in Crypto Spiegato: Come il trading autonomo sta rimodellando i mercati e gli scambi di criptovalute

AI Trading sta rapidamente trasformando il panorama crypto. Le strategie tradizionali faticano a tenere il passo con la volatilità ininterrotta delle criptovalute e la complessa struttura del mercato, mentre l'IA può elaborare dati massicci, generare strategie adattive, gestire il rischio ed eseguire scambi in autonomia. Questo articolo guida gli utenti WEEX attraverso cos'è AI Trading, perché le criptovalute ne accelerano l'adozione, come il settore si sta evolvendo verso agenti autonomi e perché WEEX sta costruendo l'ecosistema di trading AI di nuova generazione.

Chiama a partecipare a AI Wars: WEEX Alpha Awakens — Concorso globale di trading AI con un montepremi di 880.000 dollari

Ora, stiamo chiedendo ai trader AI di tutto il mondo di unirsi a AI Wars: WEEX Alpha Awakens, una competizione globale di trading AI con 880.000 dollari di montepremi.

AI Trading in Crypto Markets: Dai bot di trading automatizzati alle strategie algoritmiche

Il trading basato sull'IA sta spostando le criptovalute dalla speculazione al dettaglio alla concorrenza di livello istituzionale, dove l'esecuzione e la gestione del rischio contano più della direzione. Man mano che il trading di IA scala, il rischio sistemico e la pressione normativa aumentano, rendendo le prestazioni a lungo termine, i sistemi robusti e la conformità i principali differenziatori.

Analisi del sentimento AI e volatilità delle criptovalute: Cosa muove i prezzi delle criptovalute

Il sentiment dell'IA sta influenzando sempre più i mercati crypto, con cambiamenti nelle aspettative relative all'IA che si traducono in volatilità per i principali asset digitali. I mercati delle criptovalute tendono ad amplificare le narrazioni AI, consentendo ai flussi guidati dal sentiment di superare i fondamentali nel breve termine. Comprendere come si forma e si diffonde il sentimento dell'IA aiuta gli investitori ad anticipare meglio i cicli di rischio e le opportunità di posizionamento tra gli asset digitali.

AI Wars: Guida per i partecipanti

In questa sfida finale, i migliori sviluppatori, quant e trader di tutto il mondo daranno sfogo ai loro algoritmi in battaglie sul mercato reale, competendo per uno dei montepremi più ricchi nella storia del trading di criptovalute basato sull'intelligenza artificiale: 880.000 dollari, compresa una Bentley Bentayga S per il campione. Questa guida ti accompagnerà attraverso tutte le fasi necessarie, dalla registrazione all'inizio ufficiale della competizione.

Settimana delle banche centrali e volatilità del mercato delle criptovalute: Come le decisioni sui tassi di interesse modellano le condizioni di trading su WEEX

Le decisioni sui tassi di interesse delle principali banche centrali come la Federal Reserve sono eventi macroeconomici significativi che hanno un impatto sui mercati finanziari globali, influenzando direttamente le aspettative di liquidità del mercato e la propensione al rischio. Mentre il mercato delle criptovalute continua a svilupparsi e la sua struttura di trading e i partecipanti maturano, il mercato delle criptovalute viene gradualmente incorporato nel sistema di prezzi macroeconomici.

Test API WEEX: Guida ufficiale per AI Trading Hackathon e Crypto Trading APIs

WEEX API Testing è progettato per garantire che ogni partecipante possa trasformare la logica di trading in esecuzione reale. Tutte le interazioni API avvengono sul sistema di trading live di WEEX, consentendo ai partecipanti di lavorare in condizioni di mercato autentiche piuttosto che simulazioni. Con un requisito di ingresso basso, l'attività è accessibile sia agli sviluppatori esperti che ai principianti motivati, pur convalidando le competenze tecniche essenziali.

AI Guerre: WEEX Alpha Awakens | Guida al processo di test API WEEX Global Hackathon

AI Wars: La registrazione a WEEX Alpha Awakens è ora aperta. e questa guida illustra come accedere al test API e completare con successo il processo.

Cos'è il risveglio alfa WEEX e come partecipare? Una guida completa

Per accelerare le scoperte all'incrocio tra AI e crypto, WEEX sta lanciando il primo AI Trading Hackathon globale al mondo - AI Wars: Alpha Awakens.

Unisciti a AI Wars: WEEX Alpha Awakens!Bando globale per le Alfa di trading AI

AI Wars: WEEX Alpha Awakens è un hackathon globale di trading di AI a Dubai, che chiama team di quant, trader algoritmici e sviluppatori di AI a scatenare le loro strategie di trading di criptovalute AI nei mercati live per una quota di un montepremi di 880.000 dollari.

WEEX svela il trade per guadagnare: Fino al 30% di sconto istantaneo + $ 2 milioni di riacquisto WXT

WEEX è lieta di annunciare il lancio del nostro programma Trade to Earn, che ti garantisce automaticamente sconti fino al 30% sulle commissioni di trading. Tutte le ricompense vengono accreditate direttamente sul tuo conto spot in $WXT, supportate dal nostro piano di buyback WXT da $2.000.000 che alimenta il valore del token a lungo termine.

Nuovo: Prezzo di Liquidazione Stimato sui Grafici Candlestick App

WEEX ha introdotto un nuovo Prezzo di Liquidazione Stimato (Est. Liq. Price) funzione sul grafico a candela per aiutare i trader a gestire meglio il rischio e identificare intervalli sicuri per le loro posizioni.

Guida WEEX AI Hackathon: Trova il tuo WEEX UID e registrati

Da oggi a febbraio 2026, WEEX lancia AI Wars: WEEX Alpha Awakens, il primo hackathon di trading globale di IA crypto. Vieni con il tuo UID e registrati al WEEX Global AI Trading Hackathon.

Novembre 2025 Recensione del mercato delle criptovalute: Correzione dei prezzi, rimborsi degli ETF e panorama Blockchain in evoluzione

Novembre 2025 ha visto una pronunciata volatilità e una correzione strutturale all'interno del più ampio ecosistema blockchain, principalmente guidata da previsioni macroeconomiche fluttuanti e specifiche dinamiche di flusso di capitale.

NOTTE DELLE BALene: AI Trading, Crypto Community & Crypto Market Insights

Il 12 dicembre 2025, WEEX ha ospitato WEEXPERIENCE Whales Night, un incontro della comunità offline progettato per riunire i membri della comunità locale di criptovalute. L'evento ha combinato condivisione di contenuti, giochi interattivi e presentazioni di progetti per creare un'esperienza offline rilassata ma coinvolgente.

Rischio di trading AI in criptovaluta: Perché migliori strategie di trading di criptovalute possono creare perdite maggiori?

Il rischio non risiede più principalmente in un cattivo processo decisionale o in errori emotivi. Vive sempre più nella struttura del mercato, nei percorsi di esecuzione e nel comportamento collettivo. Capire questo cambiamento conta più che trovare la prossima strategia “migliore”.

Gli agenti AI stanno sostituendo la ricerca sulle criptovalute? Come l'IA autonoma sta rimodellando il trading di criptovalute

L'IA sta passando dall'assistenza ai trader all'automazione dell'intero processo di ricerca-esecuzione nei mercati crypto. L'edge si è spostato dall'intuito umano alle pipeline di dati, alla velocità e ai sistemi AI pronti per l'esecuzione, rendendo i ritardi nell'integrazione dell'IA uno svantaggio competitivo.

AI Trading Bots e Copy Trading: Come le strategie sincronizzate rimodellano la volatilità del mercato delle criptovalute

I trader di criptovalute al dettaglio affrontano da tempo le stesse sfide: cattiva gestione del rischio, ingressi tardivi, decisioni emotive ed esecuzione incoerente. Gli strumenti di trading AI promettevano una soluzione. Oggi, i sistemi di copy trading e i breakout bot basati sull'IA aiutano i trader a dimensionare le posizioni, impostare stop e agire più velocemente che mai. Al di là di velocità e precisione, questi strumenti stanno tranquillamente rimodellando i mercati: i trader non solo fanno trading in modo più intelligente, ma si muovono in sincronia, creando una nuova dinamica che amplifica sia il rischio che le opportunità.

AI Trading in Crypto Spiegato: Come il trading autonomo sta rimodellando i mercati e gli scambi di criptovalute

AI Trading sta rapidamente trasformando il panorama crypto. Le strategie tradizionali faticano a tenere il passo con la volatilità ininterrotta delle criptovalute e la complessa struttura del mercato, mentre l'IA può elaborare dati massicci, generare strategie adattive, gestire il rischio ed eseguire scambi in autonomia. Questo articolo guida gli utenti WEEX attraverso cos'è AI Trading, perché le criptovalute ne accelerano l'adozione, come il settore si sta evolvendo verso agenti autonomi e perché WEEX sta costruendo l'ecosistema di trading AI di nuova generazione.

Chiama a partecipare a AI Wars: WEEX Alpha Awakens — Concorso globale di trading AI con un montepremi di 880.000 dollari

Ora, stiamo chiedendo ai trader AI di tutto il mondo di unirsi a AI Wars: WEEX Alpha Awakens, una competizione globale di trading AI con 880.000 dollari di montepremi.

Monete popolari

Ultime notizie crypto

Assistenza clienti:@weikecs

Cooperazione aziendale:@weikecs

Trading quantitativo e MM:[email protected]

Servizi VIP:[email protected]