- Kup krypto

- Rynki

- Kontrakty futures

- Spot

- Copy trading

WE-Launch

WE-Launch

Web3 New Tale of Two Cities: Stablecoins and Money Market Funds

Original Article Title: Stablecoins and the parallels with Money Market Funds

Original Article Authors: @shawnwlim, @artichokecap Founders

Original Article Translation: zhouzhou, BlockBeats

Editor's Note: The regulatory dispute over stablecoins bears resemblance to the experience of Money Market Funds (MMFs) half a century ago. MMFs were initially designed for corporate cash management but faced criticism due to lack of deposit insurance and vulnerability to runs, impacting bank stability and monetary policy. Nevertheless, MMF assets now exceed $7.2 trillion. The 2008 financial crisis led to the collapse of the Reserve Fund, and in 2023, the SEC is still pushing for MMF regulatory reform. The history of MMFs suggests that stablecoins may face similar regulatory challenges but could ultimately become a crucial part of the financial system.

The following is the original content (slightly edited for readability):

Stablecoins are exciting, and the upcoming stablecoin legislation in the US represents a rare opportunity to upgrade the existing financial system. Those studying financial history will notice parallels between it and the invention and development of Money Market Funds about half a century ago.

Money Market Funds were invented in the 1970s as a cash management solution, primarily for corporates. At that time, US banks were prohibited from paying interest on balances in checking accounts, and corporations were often unable to maintain savings accounts. If a business wanted to earn interest on idle cash, they had to buy US Treasuries, engage in repurchase agreements, invest in commercial paper, or certificates of deposit. Managing cash was a cumbersome and operationally intensive process.

The design of Money Market Funds was to maintain a stable share value, with each share pegged at $1. The Reserve Fund, Inc. was the first MMF. Launched in 1971, it was introduced as "a convenient alternative for investing temporary cash balances," which would typically be placed in money market instruments like Treasuries, commercial paper, bank acceptances, or CDs, with an initial asset size of $1 million.

Other investment giants quickly followed suit: Dreyfus (now part of BNYglobal), Fidelity, Vanguard_Group. In the 1980s, almost half of Vanguard's legendary mutual fund business growth was attributable to its Money Market Fund.

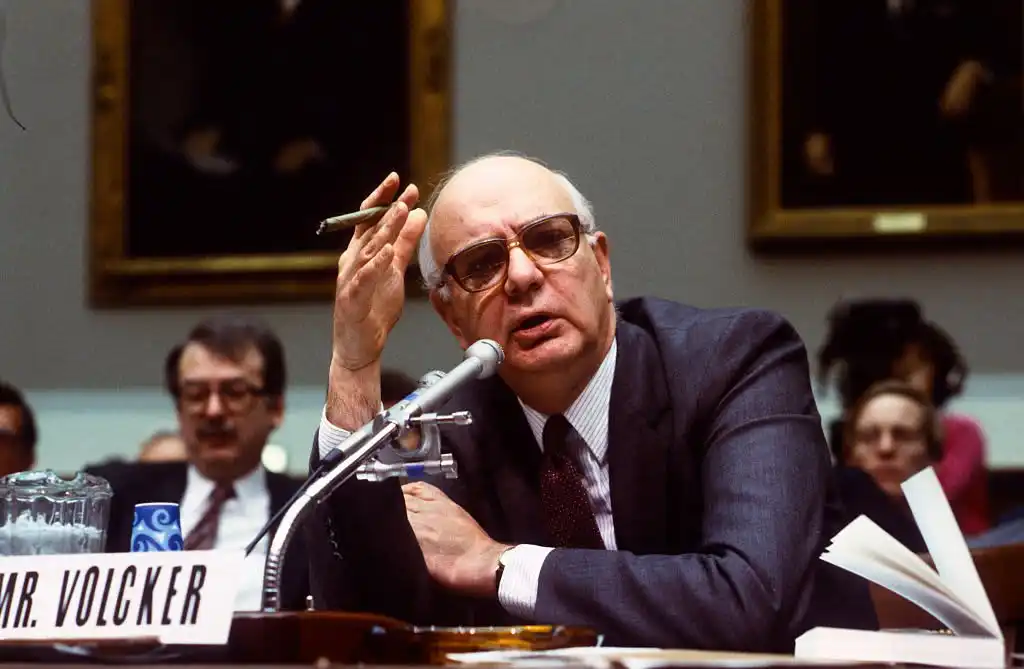

During his tenure as Chairman of the Federal Reserve from 1979 to 1987, Paul Volcker was highly critical of Money Market Funds (MMFs). He continued his criticism of MMFs as late as 2011.

Today, many of the criticisms raised by policymakers against stablecoins echo those from half a century ago against Money Market Funds:

· Systemic Risk and Banking Safety Concerns: MMFs lack deposit insurance and a lender of last resort mechanism, unlike insured banks. Because of this, MMFs are susceptible to rapid runs, which could exacerbate financial instability and lead to contagion. There are also concerns that deposits shifting from insured banks to MMFs could weaken the banking sector as banks lose their low-cost and stable deposit base.

· Unfair Regulatory Arbitrage: MMFs provide bank-like services, maintaining a stable $1 share price, but without rigorous regulatory oversight or capital requirements.

· Weakening of Monetary Policy Transmission Mechanism: MMFs could weaken the Fed's monetary policy tools, as traditional monetary policy instruments like bank reserves are less effective when funds flow from banks to MMFs.

Today, MMFs have financial assets exceeding $7.2 trillion. For reference, M2 (excluding MMF assets) is $21.7 trillion.

In the late 1990s, the rapid growth in MMF assets was a result of financial deregulation (the Gramm-Leach-Bliley Act repealed the Glass-Steagall Act, fueling a wave of financial innovation), while the prosperity of the internet facilitated better electronic and online trading systems, speeding up fund inflows into MMFs.

Do you see a pattern here? (I would like to point out that even half a century later, the regulatory struggle around MMFs is far from over. The SEC adopted MMF reforms in 2023, including raising minimum liquidity requirements and removing fund manager restrictions on investor redemptions.)

Unfortunately, the Reserve Fund met its end after the 2008 financial crisis. It held some Lehman Brothers debt securities, which were written down to zero, leading to the fund's breaking of the buck event and significant redemptions.

Możesz również polubić

WEEXPERIENCE Whales Night: Sztuczna inteligencja, społeczność kryptowalutowa i wgląd w rynek kryptowalut

12 grudnia 2025 roku WEEX zorganizował WEEXPERIENCE Whales Night, spotkanie społecznościowe offline, którego celem było zgromadzenie członków lokalnej społeczności kryptowalutowej. Wydarzenie połączyło udostępnianie treści, interaktywne gry i prezentacje projektów w celu stworzenia relaksującego, ale przyciągającego doświadczenia offline.

Ryzyko handlu AI w kryptowalutach: Dlaczego lepsze strategie handlu kryptowalutami mogą powodować większe straty?

Ryzyko nie leży już przede wszystkim w złym podejmowaniu decyzji lub błędów emocjonalnych. Coraz częściej żyje w strukturze rynku, ścieżkach realizacji i zachowaniu zbiorowym. Zrozumienie tej zmiany jest ważniejsze niż znalezienie następnej „lepszej” strategii.

Czy agenci AI zastępują badania kryptowalutowe? Jak autonomiczna sztuczna inteligencja zmienia kształt handlu kryptowalutami

AI przechodzi od wspomagania inwestorów do automatyzacji całego procesu od badania do realizacji na rynkach kryptowalut. Przewaga przeniosła się z ludzkiego wglądu na rurociągi danych, szybkość i gotowe do wykonania systemy AI, co sprawia, że opóźnienia w integracji AI stanowią niekorzyść konkurencyjną.

Tradowanie robotami AI i kopiowanie: Jak synchronizowane strategie odtwarzają zmienność rynku kryptowalut

Handlowcy kryptowalutami detalicznymi od dawna borykają się z tymi samymi wyzwaniami: słabe zarządzanie ryzykiem, późne zgłoszenia, emocjonalne decyzje i niespójne wykonanie. Narzędzia handlowe AI obiecały rozwiązanie. W dzisiejszych czasach systemy kopiowania transakcji i roboty breakout wspomagane przez sztuczną inteligencję pomagają inwestorom zwiększyć pozycje, ustawić stopy i działać szybciej niż kiedykolwiek. Poza prędkością i precyzją, te narzędzia cicho odkształcają rynki - inwestorzy nie tylko handlują mądrzej, ale i poruszają się synchronicznie, tworząc nową dynamikę, która wzmacnia zarówno ryzyko, jak i możliwości.

Trading AI w krypto wyjaśniono: Jak autonomiczny handel odtwarza rynki kryptowalut i giełdy kryptowalut

AI Trading szybko zmienia krajobraz kryptowalut. Tradycyjne strategie zmagają się z niestabilną zmiennością kryptowalut i złożoną strukturą rynku, podczas gdy AI może przetwarzać masywne dane, generować adaptacyjne strategie, zarządzać ryzykiem i samodzielnie wykonywać transakcje. Ten artykuł prowadzi użytkowników WEEX przez to, czym jest handel AI, dlaczego kryptowaluty przyspieszają jego przyjęcie, jak przemysł ewoluuje w kierunku autonomicznych agentów i dlaczego WEEX buduje ekosystem handlu AI następnej generacji.

Call to Join AI Wars: WEEX Alpha Awakens — Globalny konkurs handlowy AI z nagrodą w wysokości 880 000 $

Teraz apelujemy do handlowców AI z całego świata o przyłączenie się do AI Wars: WEEX Alpha Awakens, globalny konkurs handlowy AI z bazą nagród w wysokości 880 000 USD.

Trading AI na rynkach kryptowalut: Od automatycznych robotów handlowych po algorytmiczne strategie

Handel oparty na sztucznej inteligencji przesuwa kryptowaluty z spekulacji detalicznej na konkurencję na poziomie instytucji, gdzie wykonywanie i zarządzanie ryzykiem są ważniejsze niż kierunek. W miarę wzrostu liczby transakcji AI zwiększa się ryzyko systemowe i presja regulacyjna, co czyni z długoterminowej wydajności, solidnych systemów i zgodności kluczowymi czynnikiem różnicującym.

Analiza emocji AI i zmienność kryptowalut: Co zmienia ceny kryptowalut

Sentiment AI coraz bardziej wpływa na rynki kryptowalut, a zmiany w oczekiwaniach związanych z AI przekładają się na zmienność dla głównych aktywów cyfrowych. Rynki kryptowalutowe mają tendencję do wzmacniania narracji AI, pozwalając przepływom napędzanym sentymentem przewyższać fundamenty w krótkim czasie. Zrozumienie, w jaki sposób kształtuje się i rozprzestrzenia sentyment AI, pomaga inwestorom lepiej przewidywać cykle ryzyka i pozycjonowanie możliwości w ramach aktywów cyfrowych.

Przewodnik po hackathonie handlu AI WEEX: znajdź swój WEEX UID i zarejestruj się

Od teraz do lutego 2026 r. WEEX wprowadza na rynek AI Wars: WEEX Alpha Awakens, pierwszy na świecie globalny hackathon poświęcony handlowaniu kryptowalutami z wykorzystaniem sztucznej inteligencji. Znajdź swój identyfikator UID i zarejestruj się w globalnym hackathonie handlu AI WEEX.

AI Wars: Przewodnik uczestników

W tej ostatecznej rozgrywce najlepsi programiści, analitycy ilościowi i traderzy z całego świata wykorzystają swoje algorytmy w prawdziwych bitwach rynkowych, rywalizując o jedną z największych pul nagród w historii handlu kryptowalutami opartego na sztucznej inteligencji: 880,000 USD, w tym Bentley Bentayga S dla zwycięzcy. Ten przewodnik poprowadzi Cię przez każdy wymagany krok od rejestracji do oficjalnego rozpoczęcia konkursu.

Tydzień Banku Centralnego i zmienność rynku kryptowalut: Jak decyzje dotyczące stóp procentowych kształtują warunki handlowe w WEEX

Decyzje dotyczące stopy procentowej podejmowane przez główne banki centralne, takie jak Rezerwa Federalna, są istotnymi wydarzeniami makroekonomicznymi, wpływającymi na globalne rynki finansowe, bezpośrednio wpływając na oczekiwania rynku w zakresie płynności i apetytu na ryzyko. W miarę jak rynek kryptowalut nadal się rozwija, a jego struktura handlowa i uczestnicy dojrzewają, rynek kryptowalut jest stopniowo włączany do makroekonomicznego systemu cenowego.

WEEX API Testowanie: Oficjalny przewodnik dla AI Trading Hackathon i Crypto Trading API

WEEX API Testing ma na celu zapewnienie, że każdy uczestnik może przekształcić logikę transakcji w rzeczywiste wykonanie. Wszystkie interakcje API odbywają się w systemie WEEX Live Trading System, co pozwala uczestnikom pracować w autentycznych warunkach rynkowych, a nie w symulacjach. Dzięki wymaganiom low entry zadanie jest dostępne zarówno dla doświadczonych programistów, jak i motywowanych początkujących, jednocześnie weryfikując niezbędne umiejętności techniczne.

Wojny AI: WEEX Alpha Awakens | Przewodnik po procesie testów WEEX Global Hackathon API

AI Wars: WEEX Alpha Awakens rejestracja jest teraz otwarta. i ten przewodnik opisuje, jak uzyskać dostęp do testu API i pomyślnie zakończyć proces.

Co to jest WEEX Alpha Awakens i jak wziąć udział? Pełny przewodnik

Aby przyspieszyć przełom na skrzyżowaniu sztucznej inteligencji i kryptowalut, WEEX uruchamia pierwszy na świecie globalny hackathon handlowy AI – AI Wars: Alpha się budzi.

Dołącz do wojny AI: WEEX Alpha się budzi!Globalny Call for AI Trading Alphas

AI Wars: WEEX Alpha Awakens to globalny hackathon handlowy AI w Dubaju, wzywający zespoły kwantowe, handlowców algorytmicznych i deweloperów AI do uwolnienia swoich strategii handlu kryptowalutami AI na rynkach na żywo za udział w puli nagród w wysokości 880 000 USD.

WEEX Unveils Trade to Earn: Aż 30% zwrotu natychmiastowego + $2M WXT Buyback

WEEX z przyjemnością ogłasza uruchomienie naszego programu Trade to Earn, który automatycznie przyznaje Ci rabaty na opłaty handlowe do 30%. Wszystkie nagrody są przypisywane bezpośrednio do Twojego konta spotowego w $WXT - wspierane przez nasz plan zakupu $2,000,000 WXT, który zasila długoterminową wartość tokenów.

Nowe: Szacowana cena likwidacji w App Candlestick Charts

WEEX wprowadziła nową Stimated Liquidation Price (Est. Liq. Cena) funkcja na wykresie świecznika, aby pomóc inwestorom lepiej zarządzać ryzykiem i zidentyfikować bezpieczne zakresy dla ich pozycji.

Listopad 2025 Przegląd rynku kryptowalut: Korekta cen, zwroty ETF i ewoluujący krajobraz blockchain

W listopadzie 2025 r. nastąpiła wyraźna zmienność i korekta strukturalna w szerszym ekosystemie blockchain, głównie w wyniku zmiennych prognoz makroekonomicznych i dynamiki przepływu kapitału.

WEEXPERIENCE Whales Night: Sztuczna inteligencja, społeczność kryptowalutowa i wgląd w rynek kryptowalut

12 grudnia 2025 roku WEEX zorganizował WEEXPERIENCE Whales Night, spotkanie społecznościowe offline, którego celem było zgromadzenie członków lokalnej społeczności kryptowalutowej. Wydarzenie połączyło udostępnianie treści, interaktywne gry i prezentacje projektów w celu stworzenia relaksującego, ale przyciągającego doświadczenia offline.

Ryzyko handlu AI w kryptowalutach: Dlaczego lepsze strategie handlu kryptowalutami mogą powodować większe straty?

Ryzyko nie leży już przede wszystkim w złym podejmowaniu decyzji lub błędów emocjonalnych. Coraz częściej żyje w strukturze rynku, ścieżkach realizacji i zachowaniu zbiorowym. Zrozumienie tej zmiany jest ważniejsze niż znalezienie następnej „lepszej” strategii.

Czy agenci AI zastępują badania kryptowalutowe? Jak autonomiczna sztuczna inteligencja zmienia kształt handlu kryptowalutami

AI przechodzi od wspomagania inwestorów do automatyzacji całego procesu od badania do realizacji na rynkach kryptowalut. Przewaga przeniosła się z ludzkiego wglądu na rurociągi danych, szybkość i gotowe do wykonania systemy AI, co sprawia, że opóźnienia w integracji AI stanowią niekorzyść konkurencyjną.

Tradowanie robotami AI i kopiowanie: Jak synchronizowane strategie odtwarzają zmienność rynku kryptowalut

Handlowcy kryptowalutami detalicznymi od dawna borykają się z tymi samymi wyzwaniami: słabe zarządzanie ryzykiem, późne zgłoszenia, emocjonalne decyzje i niespójne wykonanie. Narzędzia handlowe AI obiecały rozwiązanie. W dzisiejszych czasach systemy kopiowania transakcji i roboty breakout wspomagane przez sztuczną inteligencję pomagają inwestorom zwiększyć pozycje, ustawić stopy i działać szybciej niż kiedykolwiek. Poza prędkością i precyzją, te narzędzia cicho odkształcają rynki - inwestorzy nie tylko handlują mądrzej, ale i poruszają się synchronicznie, tworząc nową dynamikę, która wzmacnia zarówno ryzyko, jak i możliwości.

Trading AI w krypto wyjaśniono: Jak autonomiczny handel odtwarza rynki kryptowalut i giełdy kryptowalut

AI Trading szybko zmienia krajobraz kryptowalut. Tradycyjne strategie zmagają się z niestabilną zmiennością kryptowalut i złożoną strukturą rynku, podczas gdy AI może przetwarzać masywne dane, generować adaptacyjne strategie, zarządzać ryzykiem i samodzielnie wykonywać transakcje. Ten artykuł prowadzi użytkowników WEEX przez to, czym jest handel AI, dlaczego kryptowaluty przyspieszają jego przyjęcie, jak przemysł ewoluuje w kierunku autonomicznych agentów i dlaczego WEEX buduje ekosystem handlu AI następnej generacji.

Call to Join AI Wars: WEEX Alpha Awakens — Globalny konkurs handlowy AI z nagrodą w wysokości 880 000 $

Teraz apelujemy do handlowców AI z całego świata o przyłączenie się do AI Wars: WEEX Alpha Awakens, globalny konkurs handlowy AI z bazą nagród w wysokości 880 000 USD.

Popularne monety

Najnowsze wiadomości kryptowalutowe

Obsługa klienta:@weikecs

Współpraca biznesowa:@weikecs

Quant trading i MM:[email protected]

Usługi VIP:[email protected]