- Купити крипту

- Ринок

- Ф’ючерси

- Спот

- Копітрейдинг

WE-Launch

WE-Launch

Web3 New Tale of Two Cities: Stablecoins and Money Market Funds

Original Article Title: Stablecoins and the parallels with Money Market Funds

Original Article Authors: @shawnwlim, @artichokecap Founders

Original Article Translation: zhouzhou, BlockBeats

Editor's Note: The regulatory dispute over stablecoins bears resemblance to the experience of Money Market Funds (MMFs) half a century ago. MMFs were initially designed for corporate cash management but faced criticism due to lack of deposit insurance and vulnerability to runs, impacting bank stability and monetary policy. Nevertheless, MMF assets now exceed $7.2 trillion. The 2008 financial crisis led to the collapse of the Reserve Fund, and in 2023, the SEC is still pushing for MMF regulatory reform. The history of MMFs suggests that stablecoins may face similar regulatory challenges but could ultimately become a crucial part of the financial system.

The following is the original content (slightly edited for readability):

Stablecoins are exciting, and the upcoming stablecoin legislation in the US represents a rare opportunity to upgrade the existing financial system. Those studying financial history will notice parallels between it and the invention and development of Money Market Funds about half a century ago.

Money Market Funds were invented in the 1970s as a cash management solution, primarily for corporates. At that time, US banks were prohibited from paying interest on balances in checking accounts, and corporations were often unable to maintain savings accounts. If a business wanted to earn interest on idle cash, they had to buy US Treasuries, engage in repurchase agreements, invest in commercial paper, or certificates of deposit. Managing cash was a cumbersome and operationally intensive process.

The design of Money Market Funds was to maintain a stable share value, with each share pegged at $1. The Reserve Fund, Inc. was the first MMF. Launched in 1971, it was introduced as "a convenient alternative for investing temporary cash balances," which would typically be placed in money market instruments like Treasuries, commercial paper, bank acceptances, or CDs, with an initial asset size of $1 million.

Other investment giants quickly followed suit: Dreyfus (now part of BNYglobal), Fidelity, Vanguard_Group. In the 1980s, almost half of Vanguard's legendary mutual fund business growth was attributable to its Money Market Fund.

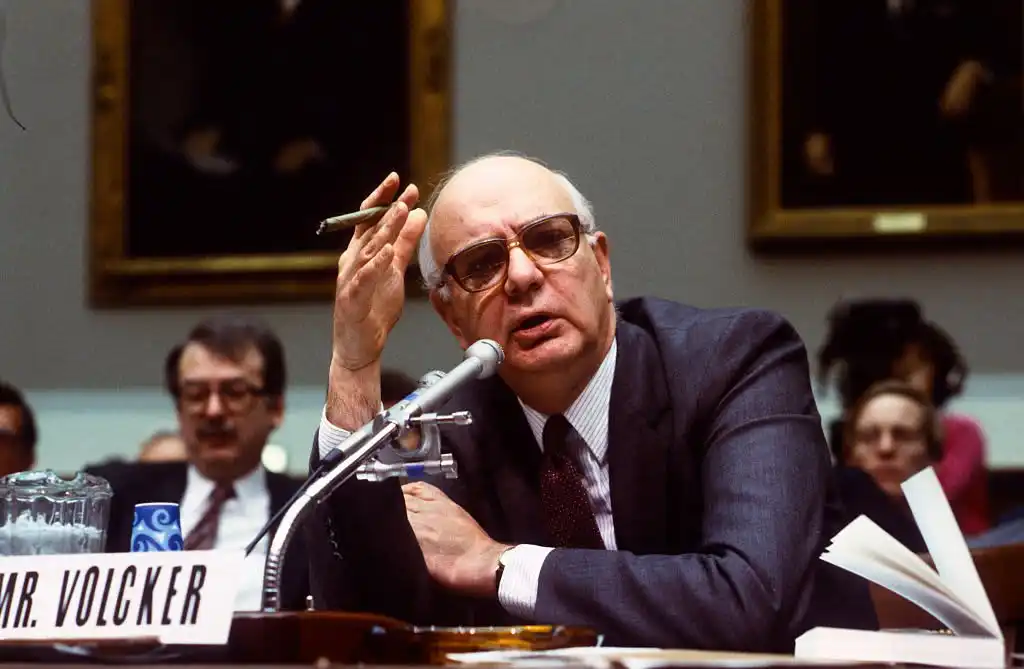

During his tenure as Chairman of the Federal Reserve from 1979 to 1987, Paul Volcker was highly critical of Money Market Funds (MMFs). He continued his criticism of MMFs as late as 2011.

Today, many of the criticisms raised by policymakers against stablecoins echo those from half a century ago against Money Market Funds:

· Systemic Risk and Banking Safety Concerns: MMFs lack deposit insurance and a lender of last resort mechanism, unlike insured banks. Because of this, MMFs are susceptible to rapid runs, which could exacerbate financial instability and lead to contagion. There are also concerns that deposits shifting from insured banks to MMFs could weaken the banking sector as banks lose their low-cost and stable deposit base.

· Unfair Regulatory Arbitrage: MMFs provide bank-like services, maintaining a stable $1 share price, but without rigorous regulatory oversight or capital requirements.

· Weakening of Monetary Policy Transmission Mechanism: MMFs could weaken the Fed's monetary policy tools, as traditional monetary policy instruments like bank reserves are less effective when funds flow from banks to MMFs.

Today, MMFs have financial assets exceeding $7.2 trillion. For reference, M2 (excluding MMF assets) is $21.7 trillion.

In the late 1990s, the rapid growth in MMF assets was a result of financial deregulation (the Gramm-Leach-Bliley Act repealed the Glass-Steagall Act, fueling a wave of financial innovation), while the prosperity of the internet facilitated better electronic and online trading systems, speeding up fund inflows into MMFs.

Do you see a pattern here? (I would like to point out that even half a century later, the regulatory struggle around MMFs is far from over. The SEC adopted MMF reforms in 2023, including raising minimum liquidity requirements and removing fund manager restrictions on investor redemptions.)

Unfortunately, the Reserve Fund met its end after the 2008 financial crisis. It held some Lehman Brothers debt securities, which were written down to zero, leading to the fund's breaking of the buck event and significant redemptions.

Вам також може сподобатися

WEEXPERIENCE Ніч китів: ШІ-торгівля, криптоспільнота та аналітика крипторинку

12 грудня 2025 року WEEX провела WEEXPERIENCE Whales Night, офлайн-зустріч спільноти, призначену для об'єднання членів місцевої криптовалютної спільноти. Захід поєднував обмін контентом, інтерактивні ігри та презентації проектів, щоб створити невимушений, але водночас захопливий офлайн-досвід.

Ризик торгівлі криптовалютою за допомогою штучного інтелекту: Чому кращі стратегії криптовалютної торгівлі можуть призвести до більших збитків?

Ризик більше не полягає переважно в поганих рішеннях чи емоційних помилках. Воно дедалі більше проявляється в ринковій структурі, шляхах виконання та колективній поведінці. Розуміння цього зрушення важливіше, ніж пошук наступної «кращої» стратегії.

Чи замінюють агенти штучного інтелекту криптодослідження? Як автономний штучний інтелект змінює криптовалютну торгівлю

Штучний інтелект переходить від допомоги трейдерам до автоматизації всього процесу від дослідження до виконання на криптовалютних ринках. Перевага змістилася від людського розуміння до конвеєрів даних, швидкості та систем штучного інтелекту, готових до виконання, що робить затримки в інтеграції штучного інтелекту конкурентним недоліком.

Торговельні боти на основі штучного інтелекту та копіювання торгівлі: Як синхронізовані стратегії змінюють волатильність крипторинку

Роздрібні криптотрейдери вже давно стикаються з тими ж проблемами: погане управління ризиками, пізні входи, емоційні рішення та непослідовне виконання. Інструменти торгівлі на основі штучного інтелекту обіцяли рішення. Сьогодні системи копіювальної торгівлі на базі штучного інтелекту та боти для проривів допомагають трейдерам визначати розмір позицій, встановлювати стоп-стопи та діяти швидше, ніж будь-коли. Окрім швидкості та точності, ці інструменти непомітно змінюють ринки — трейдери не просто торгують розумніше, вони рухаються синхронно, створюючи нову динаміку, яка посилює як ризик, так і можливості.

Пояснення торгівлі криптовалютою за допомогою штучного інтелекту: Як автономна торгівля змінює крипторинки та криптобіржі

ШІ-трейдинг швидко змінює криптоландшафт. Традиційні стратегії намагаються встигати за безперервною волатильністю криптовалют та складною структурою ринку, тоді як штучний інтелект може обробляти величезні обсяги даних, генерувати адаптивні стратегії, керувати ризиками та виконувати угоди автономно. Ця стаття розповідає користувачам WEEX, що таке торгівля на основі штучного інтелекту, чому криптовалюта прискорює її впровадження, як галузь розвивається в напрямку автономних агентів і чому WEEX створює екосистему торгівлі на основі штучного інтелекту наступного покоління.

Заклик до участі у AI Wars: WEEX Alpha Awakens — Глобальні змагання зі штучного інтелекту з призовим фондом $880 000

Зараз ми закликаємо трейдерів, що використовують штучний інтелект, з усього світу приєднатися до AI Wars: WEEX Alpha Awakens — глобальні змагання з торгівлі на основі штучного інтелекту з призовим фондом у 880 000 доларів.

Торгівля на криптовалютних ринках за допомогою штучного інтелекту: Від автоматизованих торгових ботів до алгоритмічних стратегій

Торгівля на основі штучного інтелекту переводить криптовалюту з роздрібної спекуляції в конкуренцію інституційного рівня, де виконання та управління ризиками важливіші за напрямок. Зі зростанням торгівлі на базі штучного інтелекту зростають системні ризики та регуляторний тиск, що робить довгострокову ефективність, надійні системи та відповідність вимогам ключовими відмінними рисами.

Аналіз настроїв за допомогою ШІ та волатильність криптовалюти: Що впливає на ціни на криптовалюту

Настрої щодо штучного інтелекту дедалі більше впливають на криптовалютні ринки, а зміни в очікуваннях, пов'язаних зі штучним інтелектом, призводять до волатильності основних цифрових активів. Крипторинки схильні посилювати наративи штучного інтелекту, дозволяючи потокам, зумовленим настроями, переважати фундаментальні фактори в короткостроковій перспективі. Розуміння того, як формуються та поширюються настрої щодо ШІ, допомагає інвесторам краще передбачати цикли ризику та можливості позиціонування цифрових активів.

AI Wars: посібник учасника

У цьому фінальному протистоянні провідні розробники, квантові аналітики та трейдери з усього світу використають свої алгоритми в реальних ринкових битвах, змагаючись за один з наймасштабніших призових фондів в історії ШІ-криптотрейдингу: 880 000 дол. США, зокрема Bentley Bentayga S для чемпіона. Цей посібник проведе вас через кожен необхідний крок від реєстрації до офіційного початку змагань.

Тиждень центрального банку та волатильність криптовалютного ринку: Як рішення щодо процентних ставок формують умови торгівлі на WEEX

Рішення щодо процентних ставок, прийняті основними центральними банками, такими як Федеральна резервна система, є значними макроекономічними подіями, що впливають на світові фінансові ринки, безпосередньо впливаючи на очікування ліквідності ринку та схильність до ризику. У міру того, як ринок криптовалют продовжує розвиватися, а його торгова структура та учасники стають зрілими, крипторинок поступово інтегрується в макроекономічну систему ціноутворення.

Тестування WEEX API: Офіційний посібник з хакатону зі штучним інтелектом та API для криптовалютної торгівлі

Тестування API WEEX розроблено для того, щоб кожен учасник міг перетворити торговельну логіку на реальне виконання. Усі взаємодії API відбуваються в системі живої торгівлі WEEX, що дозволяє учасникам працювати в реальних ринкових умовах, а не в симуляціях. Завдяки низьким вступним вимогам, це завдання доступне як для досвідчених розробників, так і для мотивованих новачків, водночас підтверджуючи необхідні технічні навички.

Війни ШІ: Тест для учасників

Частина 1: Рекомендований метод (хмарні сервери)

Для найкращої стабільності ми наполегливо рекомендуємо використовувати хмарний сервер зі статичною публічною IP-адресою та підтримкою цілодобової безперебійної роботи, наприклад: AWS (Amazon Web Services), Alibaba Cloud та Tencent Cloud.

**Частина 2:** Альтернативний метод (локальний комп’ютер)

Якщо ви вирішите запускати свого торгового бота з персонального комп’ютера або домашньої мережі, ви **повинні** підтвердити, що ваша вихідна IP-адреса є статичною. Зміна IP-адреси призведе до проблем із підключенням.

У вас є два основні варіанти для забезпечення стабільної вихідної IP-адреси:

Використовуйте статичну IP-адресу, надану вашим інтернет-провайдером (ISP).Використовуйте VPN або проксі-сервіс з фіксованою вихідною IP-адресою (і переконайтеся, що VPN/проксі постійно ввімкнено без перемикання серверів).Кроки для пошуку вашої локальної публічної IP-адреси:

Вимкніть усі VPN або залиште лише ту VPN, IP-адресу якої ви плануєте додати до білого списку.Відвідайте whatismyip.com у вашому браузері.На сторінці буде відображено вашу публічну IPv4-адресу.Скопіюйте цю IP-адресу та додайте її до білого списку.Примітка: Більшість домашніх широкосмугових IPv4-адрес є динамічними та можуть періодично змінюватися. Наполегливо рекомендується використовувати хмарне серверне середовище, щоб уникнути збоїв з’єднання під час змагань.

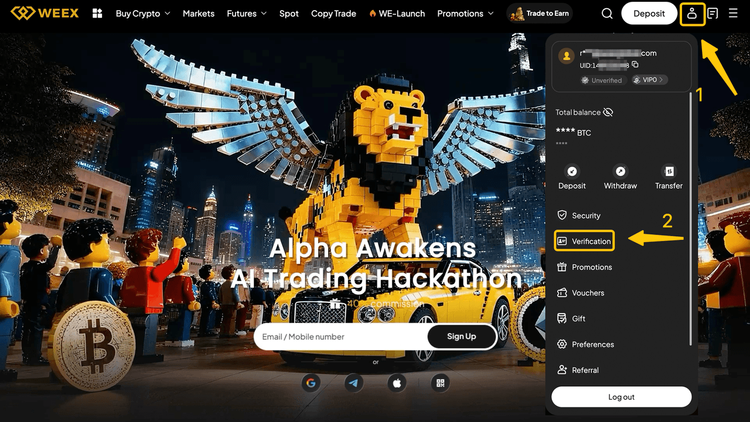

1.3 Бракує інформації? Ми будемо стежити за ситуацієюПісля того, як ви надішлете свою BUIDL, команда WEEX розгляне вашу заявку на основі вимог конкурсу. Процес перевірки зазвичай триває один робочий день.

Якщо якась інформація відсутня або потребує уточнення, наша команда зв’яжеться з вами одним із наступних каналів:

Система обміну повідомленнями DoraHacksОфіційна система повідомлень WEEXВаша зареєстрована контактна інформація (Telegram, X тощо)Будь ласка, тримайте свої контактні дані активними та доступними.

Після схвалення вашого BUIDL ви отримаєте свій аккаунт для участі в змаганнях та ексклюзивний ключ API, який дозволить вам перейти до наступного етапу: Тестування API та інтеграція моделей.

. Будь ласка, уважно прочитайте офіційну документацію WEEX API: https://www.weex.com/api-doc/ai/intro

2. Підключіться до хмарного сервера та запустіть код нижче. Ви повинні отримати відповідь, яка підтверджує, чи ваше мережеве з’єднання працює належним чином.

curl -s --max-time 10 "https://api-contract.weex.com/capi/v2/market/time"{"epoch":"1765423487.896","iso":"2025-12-11T03:24:47.896Z","timstamp":1765423487896

2. Підключіться до хмарного сервера та запустіть код нижче. Ви повинні отримати відповідь, яка підтверджує, чи ваше мережеве з’єднання працює належним чином.

import time import hmac import hashlib import base64 import requests api_key = "" secret_key = "" access_passphrase = "" def generate_signature_get(secret_key, timestamp, method, request_path, query_string): message = timestamp + method.upper() + request_path + query_string signature = hmac.new(secret_key.encode(), message.encode(), hashlib.sha256).digest() return base64.b64encode(signature).decode() def send_request_get(api_key, secret_key, access_passphrase, method, request_path, query_string): timestamp = str(int(time.time() * 1000)) signature = generate_signature_get(secret_key, timestamp, method, request_path, query_string) headers = { "ACCESS-KEY": api_key, "ACCESS-SIGN": signature, "ACCESS-TIMESTAMP": позначка часу, "ACCESS-PASSPHRASE": пароль_доступу, "Content-Type": "додаток/json", "локалізація": "uk-US" } url = "https://api-contract.weex.com/" # Будь ласка, замініть фактичною адресою API if method == "GET": response = requests.get(url + request_path+query_string, headers=headers) return response def assets(): request_path = "/capi/v2/account/assets" query_string = "" response = send_request_get(api_key, secret_key, access_passphrase, "GET", request_path, query_string) print(response.status_code) print(response.text) if __name__ == '__main__': assets()

Чому WEEX Alpha Awakens – найкраще змагання з торгівлі на основі штучного інтелекту 2025 року? Все, що вам потрібно знати

Щоб пришвидшити прориви на перетині штучного інтелекту та криптовалют, WEEX запускає перший у світі глобальний хакатон з торгівлі на основі штучного інтелекту — AI Wars: Альфа пробуджується. Призовий фонд заходу перевищує 880 000 доларів США, включаючи Bentley Bentayga S для абсолютного чемпіона.

Війни ШІ: WEEX Alpha Awakens | Посібник з процесу тестування API WEEX Global Hackathon

Війни ШІ: Реєстрація на WEEX Alpha Awakens вже відкрита, і в цьому посібнику описано, як отримати доступ до тестування API та успішно завершити процес.

Що таке WEEX Alpha Awakens і як взяти участь? Повний посібник

Щоб пришвидшити прориви на перетині штучного інтелекту та криптовалют, WEEX запускає перший у світі глобальний хакатон з торгівлі на основі штучного інтелекту — AI Wars: Альфа пробуджується.

Приєднуйтесь до війн штучного інтелекту: WEEX Альфа пробуджується!Глобальний заклик до альфа-версій торгівлі зі штучним інтелектом

Війни ШІ: WEEX Alpha Awakens – це глобальний хакатон з торгівлі на основі штучного інтелекту в Дубаї, який запрошує квантові команди, алгоритмічних трейдерів та розробників штучного інтелекту розкрити свої стратегії торгівлі на основі штучного інтелекту в криптовалюті на реальних ринках та виграти частину призового фонду в розмірі 880 000 доларів США.

WEEX представляє платформу «Торгуй, щоб заробляти»: Миттєвий ребейт до 30% + викуп WXT на суму $2 млн

WEEX рада оголосити про запуск нашої програми «Trade to Earn», яка автоматично надає вам знижку на торговельні комісії до 30%. Усі винагороди зараховуються безпосередньо на ваш спотовий рахунок у $WXT, що підтримується нашим планом викупу WXT на суму $2 000 000, який сприяє довгостроковому зростанню вартості токенів.

Нове: Орієнтовна ціна ліквідації на графіках свічок у додатку

WEEX представила нову **Очікувану ліквідаційну ціну** (Est. Liq. Ціна) на графіку свічок, щоб допомогти трейдерам краще керувати ризиками та визначати безпечні діапазони для своїх позицій.

WEEXPERIENCE Ніч китів: ШІ-торгівля, криптоспільнота та аналітика крипторинку

12 грудня 2025 року WEEX провела WEEXPERIENCE Whales Night, офлайн-зустріч спільноти, призначену для об'єднання членів місцевої криптовалютної спільноти. Захід поєднував обмін контентом, інтерактивні ігри та презентації проектів, щоб створити невимушений, але водночас захопливий офлайн-досвід.

Ризик торгівлі криптовалютою за допомогою штучного інтелекту: Чому кращі стратегії криптовалютної торгівлі можуть призвести до більших збитків?

Ризик більше не полягає переважно в поганих рішеннях чи емоційних помилках. Воно дедалі більше проявляється в ринковій структурі, шляхах виконання та колективній поведінці. Розуміння цього зрушення важливіше, ніж пошук наступної «кращої» стратегії.

Чи замінюють агенти штучного інтелекту криптодослідження? Як автономний штучний інтелект змінює криптовалютну торгівлю

Штучний інтелект переходить від допомоги трейдерам до автоматизації всього процесу від дослідження до виконання на криптовалютних ринках. Перевага змістилася від людського розуміння до конвеєрів даних, швидкості та систем штучного інтелекту, готових до виконання, що робить затримки в інтеграції штучного інтелекту конкурентним недоліком.

Торговельні боти на основі штучного інтелекту та копіювання торгівлі: Як синхронізовані стратегії змінюють волатильність крипторинку

Роздрібні криптотрейдери вже давно стикаються з тими ж проблемами: погане управління ризиками, пізні входи, емоційні рішення та непослідовне виконання. Інструменти торгівлі на основі штучного інтелекту обіцяли рішення. Сьогодні системи копіювальної торгівлі на базі штучного інтелекту та боти для проривів допомагають трейдерам визначати розмір позицій, встановлювати стоп-стопи та діяти швидше, ніж будь-коли. Окрім швидкості та точності, ці інструменти непомітно змінюють ринки — трейдери не просто торгують розумніше, вони рухаються синхронно, створюючи нову динаміку, яка посилює як ризик, так і можливості.

Пояснення торгівлі криптовалютою за допомогою штучного інтелекту: Як автономна торгівля змінює крипторинки та криптобіржі

ШІ-трейдинг швидко змінює криптоландшафт. Традиційні стратегії намагаються встигати за безперервною волатильністю криптовалют та складною структурою ринку, тоді як штучний інтелект може обробляти величезні обсяги даних, генерувати адаптивні стратегії, керувати ризиками та виконувати угоди автономно. Ця стаття розповідає користувачам WEEX, що таке торгівля на основі штучного інтелекту, чому криптовалюта прискорює її впровадження, як галузь розвивається в напрямку автономних агентів і чому WEEX створює екосистему торгівлі на основі штучного інтелекту наступного покоління.

Заклик до участі у AI Wars: WEEX Alpha Awakens — Глобальні змагання зі штучного інтелекту з призовим фондом $880 000

Зараз ми закликаємо трейдерів, що використовують штучний інтелект, з усього світу приєднатися до AI Wars: WEEX Alpha Awakens — глобальні змагання з торгівлі на основі штучного інтелекту з призовим фондом у 880 000 доларів.

Популярні монети

Останні новини криптовалют

Підтримка клієнтів:@weikecs

Співпраця:@weikecs

Кількісна торгівля та маркетмейкінг:[email protected]

VIP-послуги:[email protected]