- Krypto kaufen

- Märkte

- Futures

- Spot

- Copy-Trade

WE-Launch

WE-Launch

Arthur Hayes New Article: Federal Reserve Shift in Policy Signals Emerge, Can Bitcoin Break $250,000 by Year-End?

Original Title: The BBC

Original Source: Arthur Hayes

Original Translation: Yuliya, PANews

Within the global central bank circle, Jerome Powell and Haruhiko Kuroda have established a deep friendship. Since Haruhiko Kuroda stepped down as Governor of the Bank of Japan (BOJ) a few years ago, Powell has often sought his advice or engaged in casual chats with him. In early March this year, a meeting between Powell and the newly appointed US Treasury Secretary Scott Benette left him deeply troubled. This meeting left a psychological scar on him, prompting him to seek someone to confide in. Here is what you can imagine:

· In one conversation, Powell confided his troubles to Kuroda. Through their discussion, Kuroda recommended to him a specialized service for central bank governors called the "Jung Center". This institution, originating from the time of the Reichsbank, was founded by the renowned psychologist Carl Jung and aims to help top central bankers cope with stress. After World War II, this service expanded to London, Paris, Tokyo, and New York.

· The next day, Powell arrived at the office of the psychotherapist Justin located at 740 Park Avenue. Here, he underwent a deep psychological counseling session. Justin astutely observed that Powell was experiencing a "financial dominance" dilemma. During the counseling process, Powell revealed the humiliating experience of his meeting with Treasury Secretary Benette, an experience that severely bruised his self-esteem as the Fed Chair.

· Justin reassured him that this situation was not unprecedented. She suggested that Powell read Arthur Burns' speech "The Dilemma of the Central Bank" to help him understand and accept this predicament.

Fed Chair Powell hinted at the possibility of soon resuming quantitative easing (QE) focused on the US Treasury market during the latest March meeting, signaling a significant shift in the global US dollar liquidity landscape. Powell outlined a possible path for this, with the policy shift expected to begin implementation as early as this summer. Meanwhile, while the market is still debating the pros and cons of tariff policy, this may be good news for the cryptocurrency market.

This article will focus on the political, mathematical, and philosophical reasons for Powell's concession. It will first discuss President Trump's consistent campaign promise and why mathematically it necessitates the Fed and the US commercial banking system to print money to purchase government bonds. Then, it will discuss why the Fed has never had the opportunity to maintain tight enough monetary conditions to reduce inflation.

The Promise Made Will Surely Be Kept

Recently, macroeconomic analysts have been discussing Trump's policy intentions. Some views suggest that Trump may adopt a radical strategy and will only adjust it once his approval rating falls below 30%; others believe that Trump's goal in his final term is to reshape the world order and reform America's financial, political, and military systems. In short, he is willing to tolerate significant economic pain and a plunge in approval ratings to implement policies he believes are beneficial for the United States.

However, for investors, the key is to abandon subjective judgments of policy "rightness or wrongness" and instead focus on probability and mathematical models. The performance of a portfolio depends more on changes in legal currency liquidity globally rather than the strength of the U.S. compared to other countries. Therefore, rather than trying to speculate on Trump's policy inclination, it is better to focus on relevant data charts and mathematical relationships to better understand market trends.

Since 2016, Trump has continuously emphasized that the U.S. has been treated unfairly in recent decades due to its trading partners taking advantage. While there is controversy over the effectiveness of his policies, his core intent has remained unchanged. On the Democratic side, although their stance on adjusting the global order may not be as strong as Trump's, they generally agree with this direction. During his presidency, Biden continued Trump's policy of restricting China's access to semiconductors and other key areas of the American market. Vice President Kamala Harris had also used strong rhetoric against China in her previous presidential campaign. Although the two parties may differ in the pace and depth of implementation, they are aligned on driving this change.

The blue line represents the U.S. current account balance, basically the trade balance. It can be seen that since the mid-1990s, the U.S. has imported far more goods than it has exported, a trend that accelerated after 2000. What happened during this period? The answer is China's rise.

In 1994, China significantly devalued the renminbi, beginning its journey as an export-driven superpower. In 2001, U.S. President Bill Clinton allowed China to join the World Trade Organization, significantly reducing tariffs on Chinese exports to the U.S. As a result, the U.S. manufacturing base shifted to China, altering history.

Trump's supporters are precisely those who have been negatively affected by the outsourcing of U.S. manufacturing. These people do not have college degrees, live inland in the U.S., and have little to no financial assets. Hillary Clinton referred to them as "deplorables." Vice President JD Vance affectionately referred to them and himself as "hillbillies."

The orange dashed line in the chart and the upper panel represent the U.S. financial account balance. It is almost a mirror image of the current account balance. China and other exporting countries have been able to accumulate huge trade surpluses because when they earn U.S. dollars by selling goods to the U.S., they do not reinvest these dollars back domestically. Instead, they sell these dollars to buy their local currency like the renminbi, causing their currency to appreciate and increasing the price of their export goods. In contrast, they use these dollars to buy U.S. government bonds and U.S. stocks. This allows the U.S. to maintain a large deficit without disrupting the bond market and to have the best-performing stock market globally over the past few decades.

U.S. 10-Year Treasury Yield (White) saw a slight decrease, while the outstanding debt at the same time increased 7-fold (Yellow).

Since 2009, the performance of the MSCI USA Index (White) has outpaced the MSCI Global Index (Yellow) by 200%.

Trump believes that by bringing back manufacturing jobs to the U.S., he can provide good jobs for about 65% of the population without a college degree, strengthen the military (as weapons, etc., will be produced in sufficient quantities to counter similar or near-similar adversaries), and elevate economic growth above trend levels, such as achieving a real GDP growth of 3%.

This plan has some obvious issues:

· First, if China and other countries do not have U.S. dollars to support Treasury bonds and the stock market, prices will fall. U.S. Treasury Secretary Scott Beset needs buyers to purchase the massive debt that must be rolled over and future ongoing federal deficits. His plan is to reduce the deficit from about 7% to 3% by 2028.

· The second issue is that the capital gains taxes resulting from a rising stock market are a driving factor for the government's marginal revenue. When the wealthy cannot make money by trading stocks, the deficit increases. Trump's campaign agenda is not to stop military spending or cut welfare programs like healthcare and social security but to focus on growth and eliminating fraudulent spending. Therefore, he needs capital gains tax revenue, even though the wealthy, who own all the stocks, did not, on average, vote for him in 2024.

The Mathematical Dilemma of Debt Growth vs. Economic Growth

Assuming Trump successfully reduces the deficit from 7% to 3% by 2028, the government would still be a net borrower year after year, unable to pay down any existing stock of debt. From a mathematical perspective, this means that interest payments will continue to grow exponentially.

It sounds dire, but the U.S. can theoretically grow its way out of the issue mathematically and deleverage its balance sheet. If the real GDP grows at 3%, with a long-term inflation rate of 2% (although unlikely), this means the nominal GDP growth would be at 5%. If the government issues debt at a rate of GDP growth of 3%, but the economy's nominal growth rate is at 5%, then mathematically, the debt-to-GDP ratio will decrease over time. However, there is a key missing factor here: at what rate can the government finance itself?

In theory, if the U.S. economy grows nominally by 5%, bond investors should demand at least a 5% return. But this would significantly increase interest costs, as the current weighted average interest rate the Treasury pays on its roughly $36 trillion (and growing) debt is 3.282%.

Unless Bézeth can find a buyer of government bonds at an unreasonably high price or low yield, the math doesn't work out. With Trump currently preoccupied with reshaping the global financial and trade system, China and other export countries cannot and will not buy government bonds. Private investors won't either because the yield is too low. Only U.S. commercial banks and the Federal Reserve have the firepower to buy debt at levels the government can sustain.

The Fed can print money to buy bonds, a process known as Quantitative Easing (QE). Banks can create money to buy bonds, known as fractional reserve banking. However, the actual mechanics are not that simple.

On the surface, the Fed is busy with its unrealistic task of driving down manipulated and false inflation indicators below their fictional 2% target. They are doing this by reducing their balance sheet to remove money/credit from the system, a process called Quantitative Tightening (QT). Due to banks' poor performance in the 2008 Global Financial Crisis (GFC), regulators have required them to pledge more of their own capital against purchased government bonds, known as the Supplementary Leverage Ratio (SLR). Thus, banks cannot use unlimited leverage to fund the government.

However, changing this dynamic and making the Fed and banks inflexible buyers of government bonds is straightforward. The Fed can decide to at least end Quantitative Tightening, ramp up QE to the maximum, and exempt banks from complying with the SLR, allowing them to use unlimited leverage to buy government bonds.

The question then becomes why would Jerome Powell's-led Fed assist Trump in achieving his policy goals? The Fed notably aided Harris's campaign by cutting rates by 0.5% in September 2024, but acted stubbornly after Trump's victory by increasing the money supply to lower long-term bond yields. To understand why Powell would eventually do what the government asks of him, one may need to look back to the historical context of 1979.

Undermined Chair

Currently, Powell finds himself in a very awkward position, watching as fiscal policy dominates and undermines the Fed's credibility in fighting inflation.

In essence, when government debt becomes too large, the Fed has to relinquish its independence, using low rates to finance the government rather than truly combating inflation.

This is not a new issue. Former Fed Chair Burns faced a similar situation in the 1970s. He explained in his 1979 speech "The Pain of Central Banks" why central banks struggle to control inflation:

“Economic life in the United States and elsewhere has, since the 1930s, become colored by political and philosophical trends that have perpetuated an inflationary bias.”

In short: The politicians made me do it.

Burns pointed out that the government has become increasingly interventionist in the economy, not only assisting those in distress but also subsidizing "valuable" activities and restricting "harmful" competition. Despite the country's wealth growing, the 1960s saw unrest in American society. Minority groups, the poor, the elderly, the disabled, and others felt marginalized, while young middle-class individuals began to reject the existing institutional and cultural values. Just like then, as now, "prosperity" was not evenly distributed, and people demanded that the government address this issue.

Government action and popular demand interacted and escalated. When the government began addressing the "unfinished business" of reducing unemployment and eliminating poverty in the mid-1960s, it awakened new expectations and demands.

Now, Powell faces a similar dilemma, wanting to be a tough anti-inflation hero like Volcker, but in reality, he may be forced to capitulate to political pressure like Burns.

The history of government intervention in attempting to address key voter group issues dates back decades. The actual effects of such interventions often vary depending on the circumstances, and the outcomes are not always the same.

Many of the results of government interaction with active citizen participation have indeed had a positive impact. However, the cumulative effects of these actions have injected a strong inflationary tendency into the U.S. economy. The surge in government projects has gradually increased the tax burden on individuals and businesses. Nevertheless, there is a clear reluctance to tax as much as the tendency to spend.

A general consensus has emerged in society: problem-solving is the government's responsibility. And the primary way the government solves problems is by increasing spending, embedding inflationary factors deeply into the economic system.

In fact, the significant expansion of government spending is largely driven by the commitment to full employment. Inflation is gradually seen as a temporary phenomenon—or, as long as it remains mild, it is considered an acceptable condition.

The Fed's Inflation Tolerance and Policy Contradictions

Why does the Fed tolerate 2% inflation annually? Why does the Fed use terms like "transitory" when describing inflation? A 2% inflation compounded over 30 years would result in an 82% increase in price levels. But if the unemployment rate rises by 1%, it's considered a disaster. These are things worth pondering.

In theory, the Fed system had the ability to nip inflation in the bud or stop it at any point thereafter. It could have restricted the money supply, caused enough stress in the financial and industrial markets to quickly stop the inflation. However, the Fed did not take such action because it too was influenced by the philosophies and political trends that were changing American life and culture.

The Federal Reserve appears to maintain independence on the surface, but as a government institution philosophically inclined to address broad societal issues, it neither will nor can prevent inflation that necessitates intervention. The Federal Reserve has effectively become a collaborator, in the process creating the inflation it was supposed to control.

Faced with political realities, the Federal Reserve has indeed at times pursued contractionary monetary policies — such as in 1966, 1969, and 1974 — but its restrictive stances have not been sustained long enough to decisively quell inflation. Overall, monetary policy has been governed by the principle of "sustaining a low-level nurturing inflation process while adapting to most market pressures."

This is precisely the path that has been taken in monetary policy during Powell's current term as Chair of the Federal Reserve. This reflects the phenomenon of "fiscal dominance." The Federal Reserve will take necessary actions to provide funding support to the government. There may be differing views on the merits of policy objectives, but the message conveyed by Berns is clear: when one becomes Chair of the Federal Reserve, there is an implicit agreement to do whatever is necessary to ensure the government can finance itself at a sustainable level.

Current Policy Shift

In a recent Federal Reserve press conference, Powell displayed signs of the Federal Reserve continuing to yield to political pressures. He had to explain why, with strong economic indicators in the U.S., loose monetary conditions, the pace of Quantitative Tightening (QT) should be slowed down. The current low unemployment rate, historically high stock market, and inflation still above the 2% target should have supported a more tightening monetary policy.

Reuters reports: "The Federal Reserve said on Wednesday that starting next month, it will slow the pace of its balance sheet reduction as the issue over the government's borrowing limit remains unresolved, with this shift potentially continuing for the remainder of the process."

According to Federal Reserve historical records, despite former Federal Reserve Chair Paul Volcker being known for his strict monetary policy, in the summer of 1982, he chose to ease policy in the face of an economic recession and political pressure. At the time, the majority leader of the U.S. House of Representatives, James C. Wright Jr., met with Volcker multiple times to try to make him understand the impact of high-interest rates on the economy, but with little effect. However, by July 1982, data showed that the economic recession had bottomed out. Volcker then told congressional members that he would abandon the previously set tightening monetary policy target and predicted a "highly probable" economic recovery in the latter half of the year. This decision also aligned with the long-standing recovery expectations of the Reagan administration. It is worth noting that despite Volcker being seen as one of the most respected Federal Reserve Chairs, he also could not completely resist political pressures. Moreover, the U.S. government's debt situation at that time was far better than the current situation, with debt-to-GDP ratio only around 30%, compared to the current 130%.

Fiscal Dominance Proof

Last week, Powell proved that fiscal dominance still exists. Therefore, in the short to medium term, the QT targeting Treasuries will cease. Furthermore, Powell stated that while the Fed may maintain the natural runoff of Mortgage-Backed Securities, it will be net buying Treasuries. Mathematically, this keeps the Fed's balance sheet constant; however, this is effectively Treasury Quantitative Easing. Once formally announced, the Bitcoin price will soar.

Additionally, due to demands from banks and the Treasury, the Fed will provide SLR exemptions for banks, which is another form of Treasury Quantitative Easing. The ultimate reason is that the above mathematical calculations would otherwise not work, and Powell cannot stand by and let the U.S. government flounder, even if he detests Trump.

Powell mentioned the balance sheet adjustment plan at the March 19 FOMC press conference. He stated that the Fed will at some point halt the net asset reduction but has not made any decisions yet. At the same time, he emphasized the hope to eventually let MBS (Mortgage-Backed Securities) exit the Fed's balance sheet gradually. However, he also mentioned that the Fed might let MBS naturally expire while keeping the overall balance sheet size constant. The specific timing and method of these adjustments are currently undecided.

Treasury Secretary Yellen talked about the Supplementary Leverage Ratio (SLR) in a recent podcast, pointing out that if the SLR is removed, this policy might become a constraint for banks and could lead to a 30 to 70 basis points drop in U.S. Treasury yields. She noted that each basis point change is equivalent to an economic impact of about $1 billion per year.

Furthermore, Fed Chair Powell stated at the post-March FOMC press conference that regarding the inflationary impact of the tariff policies proposed by the Trump administration, he believes this inflation effect may be "transitory." He thinks that although tariffs could spark inflation, this impact is not expected to last long. This assessment of "transitory" inflation allows the Fed room to continue with accommodative policies when facing inflation caused by tariff hikes. Powell pointed out that the current consensus is that tariffs' price-pushing effect will not persist long-term, but he also stressed that there is still uncertainty about the future. Analysts suggest that this stance implies that the impact of tariffs on asset prices may be diminishing, especially for those assets relying solely on statutory liquidity.

Fed Chair Powell stated at the FOMC meeting in March that the inflation effect caused by tariffs may be "transitory." He believes this "transitory" inflation expectation allows the Fed to continue implementing accommodative policies even in the face of inflation due to significant tariff increases.

During a post-meeting press conference, Powell emphasized that the current baseline expectation is that the price increases caused by tariffs will be temporary, but he also added, "We can't be sure of the future specifics." Market analysts noted that the impact of tariffs may have gradually diminished for assets relying on fiat currency liquidity.

Furthermore, Trump's planned "Liberation Day" on April 2 and the potential tariff hike seem to have had no significant impact on market expectations.

USD Liquidity Calculation

It is important to look at the prospective change in USD liquidity relative to prior expectations.

· Previous pace of Treasury Quantitative Tightening (QT): $250 billion reduction per month

· Post April 1 Treasury QT pace: $50 billion reduction per month

· Net effect: Positive USD liquidity change of $240 billion annually

· Reversal effect of QT: Maximum $350 billion MBS reduction per month

· If the Fed's balance sheet remains unchanged, it could purchase: Up to $350 billion Treasuries per month or $4.2 trillion annually

Starting April 1, an additional $240 billion in relative USD liquidity will be created. In the near future, by at least the third quarter of this year, this $240 billion will rise to an annualized $420 billion. Once quantitative easing begins, it will not stop for a long time; as the economy needs more money printing to maintain the status quo, it will increase.

How the Treasury manages its General Account (TGA) is also a critical factor affecting USD liquidity. The TGA is currently around $360 billion, below the approximately $750 billion at the beginning of the year. Due to the debt ceiling constraint, the TGA is used to support government spending.

Traditionally, once the debt ceiling is raised, the TGA is replenished, which has a negative impact on USD liquidity. However, maintaining excessively high cash balances is not always economically rational; during former Treasury Secretary Yellen's tenure, the target TGA balance was set at $850 billion.

Considering that the Fed can provide liquidity support as needed, the Treasury may adopt a more flexible TGA management strategy. Analysts expect that in the upcoming Quarterly Refunding Announcement (QRA) in early May, the Treasury may not significantly increase the TGA target relative to its current level. This will mitigate any negative USD liquidity impact following the debt ceiling increase, providing a more stable environment for the market.

2008 Financial Crisis Case Study

During the 2008 Global Financial Crisis (GFC), gold and the S&P 500 exhibited different reactions to fiat currency liquidity increases. Gold, as a counter-establishment commodity financial asset, responded more quickly to liquidity injections, while the S&P 500 relied on the legal support of the national system, making its response potentially more delayed when the economic system's solvency was questioned. Data shows that during the peak of the crisis and the subsequent recovery period, gold outperformed the S&P 500. This case study suggests that even with significant current USD liquidity increases, a negative economic environment may still adversely affect the price trend of Bitcoin and cryptocurrencies.

On October 3, 2008, the U.S. government announced the initiation of the Troubled Asset Relief Program (TARP) in response to the market turmoil caused by Lehman Brothers' bankruptcy. However, this plan failed to halt the continued decline of the financial markets, with both gold and U.S. stocks falling. Subsequently, Federal Reserve Chairman Ben Bernanke announced in early December 2008 the launch of a large-scale asset purchase program (later known as quantitative easing QE1). As a result, gold began to rebound while U.S. stocks continued to fall until the Fed officially started its money printing operations in March 2009. By early 2010, the price of gold had risen by 30% since the Lehman Brothers bankruptcy, while U.S. stocks had only risen by 1% during the same period.

Bitcoin Value Equation

Bitcoin did not exist during the 2008 financial crisis, but it has now become a significant financial asset. The value of Bitcoin can be simplified as:

Bitcoin Value = Technology + Fiat Currency Liquidity

Bitcoin's technology is functioning well, with no recent significant changes, for better or worse. Therefore, Bitcoin's transactions are entirely based on the market's expectations of future fiat currency supply. If the analysis of a significant shift from Fed's quantitative tightening to Treasury quantitative easing is correct, then Bitcoin, which hit a local low of $76,500 last month, is expected to start climbing towards the year-end target of $250,000.

Although this prediction is not an exact science, considering gold's performance pattern in a similar environment, Bitcoin is more likely to first touch $110,000 than revisit $76,500. Even if the U.S. stock market continues to decline due to tariff policies, collapsing earnings expectations, or weakened foreign demand, Bitcoin is still more likely to continue its upward trend. Investors should deploy funds cautiously, avoid using leverage, and purchase small positions relative to the total portfolio size.

However, Bitcoin still has the potential to reach $250,000 by the end of the year. This optimistic outlook is based on several factors, including the possibility of the Federal Reserve injecting liquidity into the market and the People's Bank of China easing monetary policy to maintain the stability of the RMB against the USD. Furthermore, European countries increasing military spending due to security concerns may also lead to the printing of Euros, indirectly boosting market liquidity.

Das könnte Ihnen auch gefallen

WEEXPERIENCE Whales Night: KI-Handel, Krypto-Community und Krypto-Markteinblicke

Am 12. Dezember 2025 veranstaltete WEEX die WEEXPERIENCE Whales Night, ein Offline-Gemeinschaftstreffen, das lokale Kryptowährungs-Communitymitglieder zusammenbringen sollte. Die Veranstaltung kombinierte Content Sharing, interaktive Spiele und Projektpräsentationen, um ein entspanntes und dennoch ansprechendes Offline-Erlebnis zu schaffen.

AI Trading Risk in Kryptowährung: Warum können bessere Krypto-Handelsstrategien größere Verluste verursachen?

Risiko sitzt nicht mehr in erster Linie in schlechten Entscheidungen oder emotionalen Fehlern. Sie lebt zunehmend in Marktstruktur, Ausführungswegen und kollektivem Verhalten. Diesen Wandel zu verstehen ist wichtiger als die nächste „bessere“ Strategie zu finden.

KI-Agenten ersetzen Kryptoforschung? Wie autonome KI den Kryptohandel verändert

KI entwickelt sich von der Unterstützung von Händlern zur Automatisierung des gesamten Research-to-Execution-Prozesses in Kryptomärkten. Der Vorsprung hat sich von menschlichen Erkenntnissen hin zu Datenpipelines, Geschwindigkeit und ausführungsbereiten KI-Systemen verlagert, wodurch Verzögerungen bei der KI-Integration zu einem Wettbewerbsnachteil werden.

AI Trading Bots und Copy Trading: Wie synchronisierte Strategien die Volatilität des Kryptomarktes verändern

Krypto-Händler im Einzelhandel stehen seit langem vor denselben Herausforderungen: schlechtes Risikomanagement, späte Einstiege, emotionale Entscheidungen und inkonsequente Ausführung. KI-Handelstools versprachen eine Lösung. Heute helfen KI-gestützte Copy-Trading-Systeme und Breakout-Bots Händlern, Positionen zu vergrößern, Stopps zu setzen und schneller als je zuvor zu handeln. Über Geschwindigkeit und Präzision hinaus verändern diese Tools die Märkte im Stillen – Trader handeln nicht nur intelligenter, sie bewegen sich synchron und schaffen eine neue Dynamik, die sowohl Risiken als auch Chancen verstärkt.

AI Trading in Crypto Erklärt: Wie autonomer Handel Kryptomärkte und Kryptobörsen verändert

KI-Handel verändert die Krypto-Landschaft rasant. Traditionelle Strategien haben Schwierigkeiten, mit der Nonstop-Volatilität und komplexen Marktstruktur von Krypto Schritt zu halten, während KI massive Daten verarbeiten, adaptive Strategien generieren, Risiken managen und Trades autonom ausführen kann. Dieser Artikel führt WEEX-Nutzer durch, was KI-Handel ist, warum Krypto seine Einführung beschleunigt, wie sich die Branche hin zu autonomen Agenten entwickelt und warum WEEX das KI-Handelsökosystem der nächsten Generation aufbaut.

Aufruf zur Teilnahme an AI Wars: WEEX Alpha Awakens — Globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool

Jetzt rufen wir KI-Händler aus aller Welt dazu auf, sich AI Wars anzuschließen: WEEX Alpha Awakens, ein globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool.

AI Trading in Crypto Markets: Von automatisierten Trading Bots zu algorithmischen Strategien

KI-gesteuerter Handel verlagert Krypto von Einzelhandelsspekulationen zu institutionellem Wettbewerb, bei dem Ausführung und Risikomanagement wichtiger sind als Richtung. Da der KI-Handel skaliert, steigen Systemrisiken und regulatorischer Druck, was langfristige Leistung, robuste Systeme und Compliance zu den wichtigsten Unterscheidungsmerkmalen macht.

AI Sentiment Analysis and Cryptocurrency Volatility: Was bewegt Kryptopreise

KI-Sentiment beeinflusst zunehmend die Kryptomärkte, wobei sich Verschiebungen der KI-bezogenen Erwartungen in Volatilität für wichtige digitale Assets niederschlagen. Kryptomärkte neigen dazu, KI-Narrative zu verstärken, so dass sentimentgetriebene Ströme kurzfristig die Fundamentaldaten überwiegen. Zu verstehen, wie sich KI-Sentiments bilden und verbreiten, hilft Anlegern, Risikozyklen und Positionierungsmöglichkeiten in digitalen Assets besser zu antizipieren.

AI Wars: Teilnehmerleitfaden

In diesem ultimativen Showdown werden Top-Entwickler, Quants und Trader aus aller Welt ihre Algorithmen in realen Marktkämpfen einsetzen und um einen der höchsten Preispools in der Geschichte des KI-Kryptohandels konkurrieren: 880.000 USD, einschließlich eines Bentley Bentayga S für den Champion. Dieser Leitfaden führt Sie durch alle erforderlichen Schritte von der Anmeldung bis zum offiziellen Start des Wettbewerbs.

Zentralbankwoche und Kryptomarktvolatilität: Wie Zinsentscheidungen die Handelsbedingungen an WEEX prägen

Zinsentscheidungen großer Zentralbanken wie der Federal Reserve sind bedeutende makroökonomische Ereignisse, die die globalen Finanzmärkte beeinflussen und die Liquiditätserwartungen und die Risikobereitschaft der Märkte unmittelbar beeinflussen. Da sich der Kryptowährungsmarkt weiter entwickelt und seine Handelsstruktur und Teilnehmer reifen, wird der Kryptomarkt schrittweise in das makroökonomische Preissystem integriert.

WEEX API Testing: Offizieller Leitfaden für KI Trading Hackathon und Krypto Trading APIs

WEEX API Testing wurde entwickelt, um sicherzustellen, dass jeder Teilnehmer Handelslogik in echte Ausführung umsetzen kann. Alle API-Interaktionen finden auf dem Live-Trading-System von WEEX statt, sodass die Teilnehmer unter authentischen Marktbedingungen und nicht unter Simulationen arbeiten können. Mit einer geringen Einstiegsvoraussetzung ist die Aufgabe sowohl für erfahrene Entwickler als auch für motivierte Anfänger zugänglich und validiert dennoch wesentliche technische Fähigkeiten.

AI Wars: Teilnehmerführung test

Teil 1: Die empfohlene Methode (Cloud-Server)

Für beste Stabilität empfehlen wir dringend die Verwendung eines Cloud-Servers mit statischer öffentlicher IP und Unterstützung für einen unterbrechungsfreien Betrieb rund um die Uhr, wie z. B.: AWS (Amazon Web Services), Alibaba Cloud und Tencent Cloud.

Teil 2: Die alternative Methode (lokaler Computer)

Wenn Sie Ihren Handelsbot über einen PC oder ein Heimnetzwerk ausführen möchten, müssen Sie bestätigen, dass Ihre ausgehende IP-Adresse statisch ist. Eine sich ändernde IP führt zu Verbindungsproblemen.

Sie haben zwei Hauptoptionen, um eine stabile ausgehende IP zu gewährleisten:

Verwenden Sie eine statische IP, die von Ihrem Internet Service Provider (ISP) bereitgestellt wird.Verwenden Sie einen VPN- oder Proxydienst mit einer festen Ausgangs-IP (und stellen Sie sicher, dass das VPN/Proxy konsistent aktiviert ist, ohne Server zu wechseln).Schritte zum Auffinden Ihrer lokalen öffentlichen IP:

Deaktivieren Sie alle VPNs, oder behalten Sie nur das einzelne VPN bei, dessen IP Sie auf die Whitelist setzen möchten.Besuchen Sie whatismyip.com in Ihrem Browser.Die Seite zeigt Ihre öffentliche IPv4-Adresse an.Kopieren Sie diese IP und senden Sie sie an die Whitelist.Hinweis: Die meisten Heim-Breitband-IPv4-Adressen sind dynamisch und können sich periodisch ändern. Es wird dringend empfohlen, eine Cloud-Serverumgebung zu verwenden, um Verbindungsausfälle während des Wettbewerbs zu vermeiden.

1.3 Fehlende Informationen? Wir folgen weiterNachdem Sie Ihre BUIDL eingereicht haben, wird das WEEX-Team Ihre Bewerbung anhand der Wettbewerbsanforderungen prüfen. Der Überprüfungsprozess dauert normalerweise einen Geschäftstag.

Wenn Informationen fehlen oder geklärt werden müssen, wird unser Team Sie über einen der folgenden Kanäle kontaktieren:

DoraHacks NachrichtensystemOffizielles WEEX Messaging-SystemIhre registrierten Kontaktdaten (Telegramm, X, etc.)Bitte halten Sie Ihre Kontaktdaten aktiv und zugänglich.

Sobald Ihr BUIDL genehmigt ist, erhalten Sie Ihr Gewinnspielkonto und den exklusiven API Key, mit dem Sie zur nächsten Stufe übergehen können: API-Test und Modellintegration.

. Bitte lesen Sie die offizielle WEEX API Dokumentation sorgfältig durch: https://www.weex.com/api-doc/ai/intro

2. Verbinden Sie sich mit einem Cloud-Server und führen Sie den untenstehenden Code aus. Sie sollten eine Antwort erhalten, die bestätigt, ob Ihre Netzwerkverbindung ordnungsgemäß funktioniert.

curl -s --max-time 10 "https://api-contract.weex.com/capi/v2/market/time"{"epoch":"1765423487.896","iso":"2025-12-11T03:24:47.896Z","timestamp":1765423487896

2. Verbinden Sie sich mit einem Cloud-Server und führen Sie den untenstehenden Code aus. Sie sollten eine Antwort erhalten, die bestätigt, ob Ihre Netzwerkverbindung ordnungsgemäß funktioniert.

import time import hmac import hashlib import base64 import requests api_key = "" secret_key = "" access_passphrase = "" def generate_signature_get(secret_key, timestamp, method, request_path, query_string): message = timestamp + method.upper() + request_path + query_string signature = hmac.new(secret_key.encode(), message.encode(), hashlib.sha256).digest() return base64.b64encode(signature).decode() def send_request_get(api_key, secret_key, access_passphrase, method, request_path, query_string): timestamp = str(int(time.time() * 1000)) signature = generate_signature_get(secret_key, timestamp, method, request_path, query_string) headers = "ACCESS-KEY": api_key, "ACCESS-SIGN": signature, "ACCESS-TIMESTAMP": timestamp, "ACCESS-PASSPHRASE": access_passphrase, "Inhaltstyp": "application/json", "locale": "en-US" } url = "https://api-contract.weex.com/" # Bitte ersetzen Sie durch die tatsächliche API-Adresse, wenn Methode == "GET": response = requests.get(url + request_path+query_string, headers=headers) return response def assets(): request_path = "/capi/v2/account/assets" query_string = "" response = send_request_get(api_key, secret_key, access_passphrase, "GET", request_path, query_string) print(response.status_code) print(response.text) if __name__ == '__main__': assets()

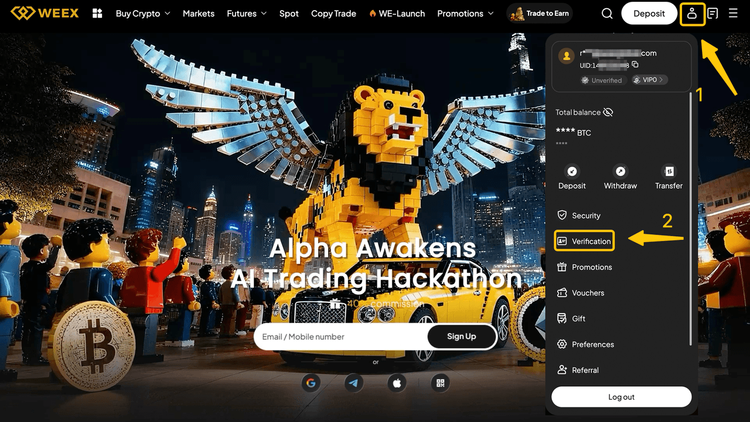

WEEX AI Trading Hackathon Guide: Finden Sie Ihre WEEX-UID und registrieren Sie sich

Bis Februar 2026 veranstaltet WEEX die AI Wars: WEEX Alpha Awakens, den weltweit ersten globalen Krypto-KI-Trading-Hackathon. Melden Sie sich mit Ihrer UID für den WEEX Global AI Trading Hackathon an.

Warum ist WEEX Alpha Awakens der beste KI-Handelswettbewerb 2025? Alles, was Sie wissen müssen

Um die Durchbrüche an der Schnittstelle von KI und Krypto zu beschleunigen, startet WEEX den weltweit ersten globalen KI Trading Hackathon – AI Wars: Alpha Erwacht. Das Event verfügt über einen bahnbrechenden Preispool von mehr als 880.000 US-Dollar, einschließlich eines Bentley Bentayga S für den ultimativen Champion.

AI Wars: WEEX Alpha Awakens | WEEX Global Hackathon API Test Process Guide

AI Wars: Die Registrierung für WEEX Alpha Awakens ist nun geöffnet. Diese Anleitung beschreibt, wie Sie auf den API-Test zugreifen und den Prozess erfolgreich abschließen können.

Was ist WEEX Alpha Awakens und wie kann man teilnehmen? Eine vollständige Anleitung

Um die Durchbrüche an der Schnittstelle von KI und Krypto zu beschleunigen, startet WEEX den weltweit ersten globalen KI Trading Hackathon – AI Wars: Alpha Erwacht.

Der WEEX HODL’em Trading Royale und Dubai Offline Trading Competition erfolgreich abgeschlossen

Am 4. Dezember 2025 veranstaltete die WEEX ihren ersten Dubai HODL’em Trading Royale und Dubai Offline Trading Competition, der die Leidenschaft von AI WARS in die reale Welt brachte.

Beitritt zu AI Wars: WEEX Alpha Erwacht!Global Call for AI Trading Alphas

AI Wars: WEEX Alpha Awakens ist ein globaler KI-Handelshackathon in Dubai, der Quantenteams, algorithmische Händler und KI-Entwickler aufruft, ihre KI-Krypto-Handelsstrategien in Live-Märkten für einen Anteil von 880.000 US-Dollar Preispool freizusetzen.

WEEXPERIENCE Whales Night: KI-Handel, Krypto-Community und Krypto-Markteinblicke

Am 12. Dezember 2025 veranstaltete WEEX die WEEXPERIENCE Whales Night, ein Offline-Gemeinschaftstreffen, das lokale Kryptowährungs-Communitymitglieder zusammenbringen sollte. Die Veranstaltung kombinierte Content Sharing, interaktive Spiele und Projektpräsentationen, um ein entspanntes und dennoch ansprechendes Offline-Erlebnis zu schaffen.

AI Trading Risk in Kryptowährung: Warum können bessere Krypto-Handelsstrategien größere Verluste verursachen?

Risiko sitzt nicht mehr in erster Linie in schlechten Entscheidungen oder emotionalen Fehlern. Sie lebt zunehmend in Marktstruktur, Ausführungswegen und kollektivem Verhalten. Diesen Wandel zu verstehen ist wichtiger als die nächste „bessere“ Strategie zu finden.

KI-Agenten ersetzen Kryptoforschung? Wie autonome KI den Kryptohandel verändert

KI entwickelt sich von der Unterstützung von Händlern zur Automatisierung des gesamten Research-to-Execution-Prozesses in Kryptomärkten. Der Vorsprung hat sich von menschlichen Erkenntnissen hin zu Datenpipelines, Geschwindigkeit und ausführungsbereiten KI-Systemen verlagert, wodurch Verzögerungen bei der KI-Integration zu einem Wettbewerbsnachteil werden.

AI Trading Bots und Copy Trading: Wie synchronisierte Strategien die Volatilität des Kryptomarktes verändern

Krypto-Händler im Einzelhandel stehen seit langem vor denselben Herausforderungen: schlechtes Risikomanagement, späte Einstiege, emotionale Entscheidungen und inkonsequente Ausführung. KI-Handelstools versprachen eine Lösung. Heute helfen KI-gestützte Copy-Trading-Systeme und Breakout-Bots Händlern, Positionen zu vergrößern, Stopps zu setzen und schneller als je zuvor zu handeln. Über Geschwindigkeit und Präzision hinaus verändern diese Tools die Märkte im Stillen – Trader handeln nicht nur intelligenter, sie bewegen sich synchron und schaffen eine neue Dynamik, die sowohl Risiken als auch Chancen verstärkt.

AI Trading in Crypto Erklärt: Wie autonomer Handel Kryptomärkte und Kryptobörsen verändert

KI-Handel verändert die Krypto-Landschaft rasant. Traditionelle Strategien haben Schwierigkeiten, mit der Nonstop-Volatilität und komplexen Marktstruktur von Krypto Schritt zu halten, während KI massive Daten verarbeiten, adaptive Strategien generieren, Risiken managen und Trades autonom ausführen kann. Dieser Artikel führt WEEX-Nutzer durch, was KI-Handel ist, warum Krypto seine Einführung beschleunigt, wie sich die Branche hin zu autonomen Agenten entwickelt und warum WEEX das KI-Handelsökosystem der nächsten Generation aufbaut.

Aufruf zur Teilnahme an AI Wars: WEEX Alpha Awakens — Globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool

Jetzt rufen wir KI-Händler aus aller Welt dazu auf, sich AI Wars anzuschließen: WEEX Alpha Awakens, ein globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool.

Beliebte Coins

Neueste Krypto-Nachrichten

Kundenservice:@weikecs

Geschäftliche Zusammenarbeit:@weikecs

Quant-Trading & MM:[email protected]

VIP-Services:[email protected]