- Krypto kaufen

- Märkte

- Futures

- Spot

- Copy-Trade

WE-Launch

WE-Launch

Ye Kai: Reframing Asset Liquidity — How RWA Reshapes Data Asset Management Model

Original Article Title: "Ye Kai: Rethinking Asset Liquidity — How RWA Reshapes Data Asset Management Models | China Data Asset Management 50+ Forum"

Original Source: Shanghai Data Exchange

1. High RWA Financing Cost in Hong Kong

The current RWA market in Hong Kong faces high financing costs. From a cost perspective, the financing cost for high-quality domestic enterprises through bank channels generally remains in the range of 3.5%-4%, while the comprehensive cost of issuing RWAs in Hong Kong (including HKD 4-5 million issuance expenses) is as high as 10%, showing a clear cost inversion phenomenon. In this context, the core appeal for listed companies to participate in RWA has shifted from simple financing to market value management. A typical case shows that a technology company, after issuing RWA, saw its market value climb from HKD 6.7 billion to HKD 14.6 billion within three to four months.

The transitional nature of the Hong Kong regulatory framework is particularly prominent. According to current regulations, debt-based RWAs are limited to professional investors (PIs) participation, and licensed trading platforms cannot open a secondary retail market. This restriction objectively drives the market to form a "securitization-first, tokenization-follow-up" Web2.5 model: companies need to first transform assets into fund products regulated by a Type 9 license before undergoing tokenization by licensed institutions. Although liquidity is constrained in the short term, it creates an opportunity to build a multi-level cross-border market system.

2. Multi-level Market Collaborative Architecture

The key to unlocking the liquidity dilemma in the Hong Kong market lies in establishing a cross-border collaborative mechanism, such as establishing a three-layer experimental architecture for Mainland China-Hong Kong-Singapore.

· The first layer is the onshore ownership layer, where data asset trading platforms in Mainland China conduct data asset standardization processing, prepare assets through a sandbox mechanism, and ensure onshore ownership of core data, among other operations.

· The second layer is the offshore issuance layer, where Hong Kong licensed institutions package processed data assets into compliant fund products and conduct private placements based on a Type 9 license.

· The third layer is the global circulation layer, where Singapore leverages the advantage of an RMO license to accommodate secondary market circulation, achieving compliant cross-border circulation through the China-Singapore international data channel.

The innovative value of this architecture lies in three dimensions: first, the onshore link strictly observes data security bottom line to avoid risks of Regulation 38; second, Hong Kong leverages the professional advantages of licensed institutions, focusing on primary market issuance; third, Singapore opens the secondary retail market, activating global capital participation.

3. Structured Financial Design Thinking

Mere asset tokenization cannot form effective financial products; instead, structured financial product design is needed. Taking BlackRock's fund operation model as an example, BlackRock combines mid-term US Treasury ETFs with smart contract collateralization to ensure a base return of 6-8% while unlocking premium floating space through native token issuance. This model has successfully attracted over 30% of crypto-native capital allocation demand.

Offshore support system is equally important. For example, in the Hainan Free Trade Port, the VIE structure + FT account combination can be tested to achieve cross-border asset transfer and fund circulation in a physically isolated framework. The "regulatory sandbox + whitelist network" design provides a solution for the circulation of sensitive assets. This model uses the VIE structure to achieve the outbound transfer of asset ownership in a legal sense, utilizes the FT account system to build a firewall for fund flow, and establishes a dedicated network channel to overcome cross-border operational barriers.

IV. Wall Street Stair-step Penetration Strategy

BlackRock's stair-step penetration strategy is worthy of special attention. From a Bitcoin spot ETF (with over $30 billion in AUM) to tokenized money market funds (BUIDL Fund surpassing $1 billion in scale), and then collaborating with Circle to issue the stablecoin USDB, its development path demonstrates a seamless transition from the institutional market to the retail market. Even more disruptive is the institution's plan to transform $11.6 trillion in medium to long-term assets into on-chain liquidity through collateralization, potentially reshaping the global fund circulation paradigm.

A Distributed Digital Identity (DID) system constitutes a strategic fulcrum. BlackRock explicitly positions DID as the infrastructure for inclusive finance in public documents, attempting to break down barriers between institutional and retail markets through a verifiable credit system. The insight for Hong Kong is that RWA development should not be limited to the professional investor market but should encompass forward-looking initiatives such as digital identity authentication and on-chain settlement capabilities.

V. Development Assessment and Path Selection

The Hong Kong RWA ecosystem is currently in a phase where regulatory arbitrage opportunities overlap with the key period of model standardization. The breakthrough direction presents three major trends: first, optimizing market structure to consolidate Hong Kong's position in the primary issuance market and complementing Singapore's secondary market. Second, upgrading product capabilities from simple asset securitization to structured designs such as ABS tranching and revenue rights passthrough. Third, prioritizing digital infrastructure development, accelerating the construction of DID systems, smart contract clearing platforms, and other foundational infrastructure.

For domestic businesses, the priorities are firstly to innovate development models by establishing a standardized process for "domestic asset preparation - offshore financial issuance," secondly to cultivate cross-border structured product design capabilities to gain a competitive advantage, and thirdly to focus on stablecoin and collateral derivative innovation to prevent overseas liquidity suction effects.

Das könnte Ihnen auch gefallen

WEEXPERIENCE Whales Night: KI-Handel, Krypto-Community und Krypto-Markteinblicke

Am 12. Dezember 2025 veranstaltete WEEX die WEEXPERIENCE Whales Night, ein Offline-Gemeinschaftstreffen, das lokale Kryptowährungs-Communitymitglieder zusammenbringen sollte. Die Veranstaltung kombinierte Content Sharing, interaktive Spiele und Projektpräsentationen, um ein entspanntes und dennoch ansprechendes Offline-Erlebnis zu schaffen.

AI Trading Risk in Kryptowährung: Warum können bessere Krypto-Handelsstrategien größere Verluste verursachen?

Risiko sitzt nicht mehr in erster Linie in schlechten Entscheidungen oder emotionalen Fehlern. Sie lebt zunehmend in Marktstruktur, Ausführungswegen und kollektivem Verhalten. Diesen Wandel zu verstehen ist wichtiger als die nächste „bessere“ Strategie zu finden.

KI-Agenten ersetzen Kryptoforschung? Wie autonome KI den Kryptohandel verändert

KI entwickelt sich von der Unterstützung von Händlern zur Automatisierung des gesamten Research-to-Execution-Prozesses in Kryptomärkten. Der Vorsprung hat sich von menschlichen Erkenntnissen hin zu Datenpipelines, Geschwindigkeit und ausführungsbereiten KI-Systemen verlagert, wodurch Verzögerungen bei der KI-Integration zu einem Wettbewerbsnachteil werden.

AI Trading Bots und Copy Trading: Wie synchronisierte Strategien die Volatilität des Kryptomarktes verändern

Krypto-Händler im Einzelhandel stehen seit langem vor denselben Herausforderungen: schlechtes Risikomanagement, späte Einstiege, emotionale Entscheidungen und inkonsequente Ausführung. KI-Handelstools versprachen eine Lösung. Heute helfen KI-gestützte Copy-Trading-Systeme und Breakout-Bots Händlern, Positionen zu vergrößern, Stopps zu setzen und schneller als je zuvor zu handeln. Über Geschwindigkeit und Präzision hinaus verändern diese Tools die Märkte im Stillen – Trader handeln nicht nur intelligenter, sie bewegen sich synchron und schaffen eine neue Dynamik, die sowohl Risiken als auch Chancen verstärkt.

AI Trading in Crypto Erklärt: Wie autonomer Handel Kryptomärkte und Kryptobörsen verändert

KI-Handel verändert die Krypto-Landschaft rasant. Traditionelle Strategien haben Schwierigkeiten, mit der Nonstop-Volatilität und komplexen Marktstruktur von Krypto Schritt zu halten, während KI massive Daten verarbeiten, adaptive Strategien generieren, Risiken managen und Trades autonom ausführen kann. Dieser Artikel führt WEEX-Nutzer durch, was KI-Handel ist, warum Krypto seine Einführung beschleunigt, wie sich die Branche hin zu autonomen Agenten entwickelt und warum WEEX das KI-Handelsökosystem der nächsten Generation aufbaut.

Aufruf zur Teilnahme an AI Wars: WEEX Alpha Awakens — Globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool

Jetzt rufen wir KI-Händler aus aller Welt dazu auf, sich AI Wars anzuschließen: WEEX Alpha Awakens, ein globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool.

AI Trading in Crypto Markets: Von automatisierten Trading Bots zu algorithmischen Strategien

KI-gesteuerter Handel verlagert Krypto von Einzelhandelsspekulationen zu institutionellem Wettbewerb, bei dem Ausführung und Risikomanagement wichtiger sind als Richtung. Da der KI-Handel skaliert, steigen Systemrisiken und regulatorischer Druck, was langfristige Leistung, robuste Systeme und Compliance zu den wichtigsten Unterscheidungsmerkmalen macht.

AI Sentiment Analysis and Cryptocurrency Volatility: Was bewegt Kryptopreise

KI-Sentiment beeinflusst zunehmend die Kryptomärkte, wobei sich Verschiebungen der KI-bezogenen Erwartungen in Volatilität für wichtige digitale Assets niederschlagen. Kryptomärkte neigen dazu, KI-Narrative zu verstärken, so dass sentimentgetriebene Ströme kurzfristig die Fundamentaldaten überwiegen. Zu verstehen, wie sich KI-Sentiments bilden und verbreiten, hilft Anlegern, Risikozyklen und Positionierungsmöglichkeiten in digitalen Assets besser zu antizipieren.

AI Wars: Teilnehmerleitfaden

In diesem ultimativen Showdown werden Top-Entwickler, Quants und Trader aus aller Welt ihre Algorithmen in realen Marktkämpfen einsetzen und um einen der höchsten Preispools in der Geschichte des KI-Kryptohandels konkurrieren: 880.000 USD, einschließlich eines Bentley Bentayga S für den Champion. Dieser Leitfaden führt Sie durch alle erforderlichen Schritte von der Anmeldung bis zum offiziellen Start des Wettbewerbs.

Zentralbankwoche und Kryptomarktvolatilität: Wie Zinsentscheidungen die Handelsbedingungen an WEEX prägen

Zinsentscheidungen großer Zentralbanken wie der Federal Reserve sind bedeutende makroökonomische Ereignisse, die die globalen Finanzmärkte beeinflussen und die Liquiditätserwartungen und die Risikobereitschaft der Märkte unmittelbar beeinflussen. Da sich der Kryptowährungsmarkt weiter entwickelt und seine Handelsstruktur und Teilnehmer reifen, wird der Kryptomarkt schrittweise in das makroökonomische Preissystem integriert.

WEEX API Testing: Offizieller Leitfaden für KI Trading Hackathon und Krypto Trading APIs

WEEX API Testing wurde entwickelt, um sicherzustellen, dass jeder Teilnehmer Handelslogik in echte Ausführung umsetzen kann. Alle API-Interaktionen finden auf dem Live-Trading-System von WEEX statt, sodass die Teilnehmer unter authentischen Marktbedingungen und nicht unter Simulationen arbeiten können. Mit einer geringen Einstiegsvoraussetzung ist die Aufgabe sowohl für erfahrene Entwickler als auch für motivierte Anfänger zugänglich und validiert dennoch wesentliche technische Fähigkeiten.

AI Wars: Teilnehmerführung test

Teil 1: Die empfohlene Methode (Cloud-Server)

Für beste Stabilität empfehlen wir dringend die Verwendung eines Cloud-Servers mit statischer öffentlicher IP und Unterstützung für einen unterbrechungsfreien Betrieb rund um die Uhr, wie z. B.: AWS (Amazon Web Services), Alibaba Cloud und Tencent Cloud.

Teil 2: Die alternative Methode (lokaler Computer)

Wenn Sie Ihren Handelsbot über einen PC oder ein Heimnetzwerk ausführen möchten, müssen Sie bestätigen, dass Ihre ausgehende IP-Adresse statisch ist. Eine sich ändernde IP führt zu Verbindungsproblemen.

Sie haben zwei Hauptoptionen, um eine stabile ausgehende IP zu gewährleisten:

Verwenden Sie eine statische IP, die von Ihrem Internet Service Provider (ISP) bereitgestellt wird.Verwenden Sie einen VPN- oder Proxydienst mit einer festen Ausgangs-IP (und stellen Sie sicher, dass das VPN/Proxy konsistent aktiviert ist, ohne Server zu wechseln).Schritte zum Auffinden Ihrer lokalen öffentlichen IP:

Deaktivieren Sie alle VPNs, oder behalten Sie nur das einzelne VPN bei, dessen IP Sie auf die Whitelist setzen möchten.Besuchen Sie whatismyip.com in Ihrem Browser.Die Seite zeigt Ihre öffentliche IPv4-Adresse an.Kopieren Sie diese IP und senden Sie sie an die Whitelist.Hinweis: Die meisten Heim-Breitband-IPv4-Adressen sind dynamisch und können sich periodisch ändern. Es wird dringend empfohlen, eine Cloud-Serverumgebung zu verwenden, um Verbindungsausfälle während des Wettbewerbs zu vermeiden.

1.3 Fehlende Informationen? Wir folgen weiterNachdem Sie Ihre BUIDL eingereicht haben, wird das WEEX-Team Ihre Bewerbung anhand der Wettbewerbsanforderungen prüfen. Der Überprüfungsprozess dauert normalerweise einen Geschäftstag.

Wenn Informationen fehlen oder geklärt werden müssen, wird unser Team Sie über einen der folgenden Kanäle kontaktieren:

DoraHacks NachrichtensystemOffizielles WEEX Messaging-SystemIhre registrierten Kontaktdaten (Telegramm, X, etc.)Bitte halten Sie Ihre Kontaktdaten aktiv und zugänglich.

Sobald Ihr BUIDL genehmigt ist, erhalten Sie Ihr Gewinnspielkonto und den exklusiven API Key, mit dem Sie zur nächsten Stufe übergehen können: API-Test und Modellintegration.

. Bitte lesen Sie die offizielle WEEX API Dokumentation sorgfältig durch: https://www.weex.com/api-doc/ai/intro

2. Verbinden Sie sich mit einem Cloud-Server und führen Sie den untenstehenden Code aus. Sie sollten eine Antwort erhalten, die bestätigt, ob Ihre Netzwerkverbindung ordnungsgemäß funktioniert.

curl -s --max-time 10 "https://api-contract.weex.com/capi/v2/market/time"{"epoch":"1765423487.896","iso":"2025-12-11T03:24:47.896Z","timestamp":1765423487896

2. Verbinden Sie sich mit einem Cloud-Server und führen Sie den untenstehenden Code aus. Sie sollten eine Antwort erhalten, die bestätigt, ob Ihre Netzwerkverbindung ordnungsgemäß funktioniert.

import time import hmac import hashlib import base64 import requests api_key = "" secret_key = "" access_passphrase = "" def generate_signature_get(secret_key, timestamp, method, request_path, query_string): message = timestamp + method.upper() + request_path + query_string signature = hmac.new(secret_key.encode(), message.encode(), hashlib.sha256).digest() return base64.b64encode(signature).decode() def send_request_get(api_key, secret_key, access_passphrase, method, request_path, query_string): timestamp = str(int(time.time() * 1000)) signature = generate_signature_get(secret_key, timestamp, method, request_path, query_string) headers = "ACCESS-KEY": api_key, "ACCESS-SIGN": signature, "ACCESS-TIMESTAMP": timestamp, "ACCESS-PASSPHRASE": access_passphrase, "Inhaltstyp": "application/json", "locale": "en-US" } url = "https://api-contract.weex.com/" # Bitte ersetzen Sie durch die tatsächliche API-Adresse, wenn Methode == "GET": response = requests.get(url + request_path+query_string, headers=headers) return response def assets(): request_path = "/capi/v2/account/assets" query_string = "" response = send_request_get(api_key, secret_key, access_passphrase, "GET", request_path, query_string) print(response.status_code) print(response.text) if __name__ == '__main__': assets()

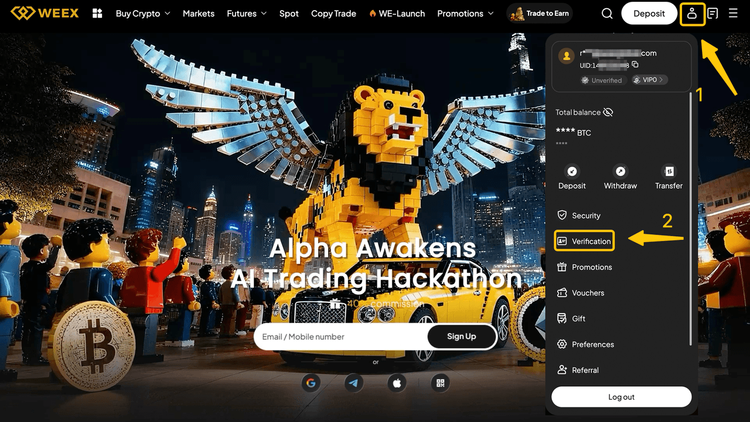

WEEX AI Trading Hackathon Guide: Finden Sie Ihre WEEX-UID und registrieren Sie sich

Bis Februar 2026 veranstaltet WEEX die AI Wars: WEEX Alpha Awakens, den weltweit ersten globalen Krypto-KI-Trading-Hackathon. Melden Sie sich mit Ihrer UID für den WEEX Global AI Trading Hackathon an.

Warum ist WEEX Alpha Awakens der beste KI-Handelswettbewerb 2025? Alles, was Sie wissen müssen

Um die Durchbrüche an der Schnittstelle von KI und Krypto zu beschleunigen, startet WEEX den weltweit ersten globalen KI Trading Hackathon – AI Wars: Alpha Erwacht. Das Event verfügt über einen bahnbrechenden Preispool von mehr als 880.000 US-Dollar, einschließlich eines Bentley Bentayga S für den ultimativen Champion.

AI Wars: WEEX Alpha Awakens | WEEX Global Hackathon API Test Process Guide

AI Wars: Die Registrierung für WEEX Alpha Awakens ist nun geöffnet. Diese Anleitung beschreibt, wie Sie auf den API-Test zugreifen und den Prozess erfolgreich abschließen können.

Was ist WEEX Alpha Awakens und wie kann man teilnehmen? Eine vollständige Anleitung

Um die Durchbrüche an der Schnittstelle von KI und Krypto zu beschleunigen, startet WEEX den weltweit ersten globalen KI Trading Hackathon – AI Wars: Alpha Erwacht.

Der WEEX HODL’em Trading Royale und Dubai Offline Trading Competition erfolgreich abgeschlossen

Am 4. Dezember 2025 veranstaltete die WEEX ihren ersten Dubai HODL’em Trading Royale und Dubai Offline Trading Competition, der die Leidenschaft von AI WARS in die reale Welt brachte.

Beitritt zu AI Wars: WEEX Alpha Erwacht!Global Call for AI Trading Alphas

AI Wars: WEEX Alpha Awakens ist ein globaler KI-Handelshackathon in Dubai, der Quantenteams, algorithmische Händler und KI-Entwickler aufruft, ihre KI-Krypto-Handelsstrategien in Live-Märkten für einen Anteil von 880.000 US-Dollar Preispool freizusetzen.

WEEXPERIENCE Whales Night: KI-Handel, Krypto-Community und Krypto-Markteinblicke

Am 12. Dezember 2025 veranstaltete WEEX die WEEXPERIENCE Whales Night, ein Offline-Gemeinschaftstreffen, das lokale Kryptowährungs-Communitymitglieder zusammenbringen sollte. Die Veranstaltung kombinierte Content Sharing, interaktive Spiele und Projektpräsentationen, um ein entspanntes und dennoch ansprechendes Offline-Erlebnis zu schaffen.

AI Trading Risk in Kryptowährung: Warum können bessere Krypto-Handelsstrategien größere Verluste verursachen?

Risiko sitzt nicht mehr in erster Linie in schlechten Entscheidungen oder emotionalen Fehlern. Sie lebt zunehmend in Marktstruktur, Ausführungswegen und kollektivem Verhalten. Diesen Wandel zu verstehen ist wichtiger als die nächste „bessere“ Strategie zu finden.

KI-Agenten ersetzen Kryptoforschung? Wie autonome KI den Kryptohandel verändert

KI entwickelt sich von der Unterstützung von Händlern zur Automatisierung des gesamten Research-to-Execution-Prozesses in Kryptomärkten. Der Vorsprung hat sich von menschlichen Erkenntnissen hin zu Datenpipelines, Geschwindigkeit und ausführungsbereiten KI-Systemen verlagert, wodurch Verzögerungen bei der KI-Integration zu einem Wettbewerbsnachteil werden.

AI Trading Bots und Copy Trading: Wie synchronisierte Strategien die Volatilität des Kryptomarktes verändern

Krypto-Händler im Einzelhandel stehen seit langem vor denselben Herausforderungen: schlechtes Risikomanagement, späte Einstiege, emotionale Entscheidungen und inkonsequente Ausführung. KI-Handelstools versprachen eine Lösung. Heute helfen KI-gestützte Copy-Trading-Systeme und Breakout-Bots Händlern, Positionen zu vergrößern, Stopps zu setzen und schneller als je zuvor zu handeln. Über Geschwindigkeit und Präzision hinaus verändern diese Tools die Märkte im Stillen – Trader handeln nicht nur intelligenter, sie bewegen sich synchron und schaffen eine neue Dynamik, die sowohl Risiken als auch Chancen verstärkt.

AI Trading in Crypto Erklärt: Wie autonomer Handel Kryptomärkte und Kryptobörsen verändert

KI-Handel verändert die Krypto-Landschaft rasant. Traditionelle Strategien haben Schwierigkeiten, mit der Nonstop-Volatilität und komplexen Marktstruktur von Krypto Schritt zu halten, während KI massive Daten verarbeiten, adaptive Strategien generieren, Risiken managen und Trades autonom ausführen kann. Dieser Artikel führt WEEX-Nutzer durch, was KI-Handel ist, warum Krypto seine Einführung beschleunigt, wie sich die Branche hin zu autonomen Agenten entwickelt und warum WEEX das KI-Handelsökosystem der nächsten Generation aufbaut.

Aufruf zur Teilnahme an AI Wars: WEEX Alpha Awakens — Globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool

Jetzt rufen wir KI-Händler aus aller Welt dazu auf, sich AI Wars anzuschließen: WEEX Alpha Awakens, ein globaler KI-Handelswettbewerb mit 880.000 US-Dollar Preispool.

Beliebte Coins

Neueste Krypto-Nachrichten

Kundenservice:@weikecs

Geschäftliche Zusammenarbeit:@weikecs

Quant-Trading & MM:[email protected]

VIP-Services:[email protected]