- Buy Crypto

- Markets

- Futures

- Spot

- Copy Trade

WE-Launch

WE-Launch

Next year, will Pump.fun still be able to tell a new story?

Original Article Title: Pump's Year Ahead: Reflections on Resilience, Creator Economics, and the Search for Direction

Original Article Author: @simononchain, Crypto KOL

Original Article Translation: Deep Tide TechFlow

The following content is excerpted from Delphi's upcoming "2026 App Outlook Report," focusing on Pump(.)fun— one of the consumer apps we are most interested in next year.

Since we published our initial Pump report (pre-funding), many things have changed. Many of the dynamics we predicted have been validated, but there are also areas where expectations have not been met, leaving users and investors disappointed. However, Pump's core challenges remain.

To achieve Pump's grand vision, the team needs to find a balance between the short-term profit-driven nature of the crypto industry and its long-term platform vision. It is worth noting that once a project launches a token, the operational environment shifts; the token itself becomes an independent product with inherent reflexivity and continues to influence user expectations, and Pump is no exception.

Since completing the funding, the Pump team has been increasingly investing in native crypto streaming, but the development in this area has not been as smooth as we expected, at least not yet at the desired level.

Pump has not successfully attracted core creators from outside the crypto ecosystem, and the rise of CCM Metaverse on the Pump platform has been short-lived. The most notable moment came from the "Bagwork" event, which not only demonstrated the potential of creator-driven tokens but also revealed structural issues hindering the development of this model.

This phenomenon was led by a group of teenagers who, with partial support from Pump, carried out a series of controversial events: stealing Bradley Martyn's hat, storming the Dodgers game venue, rushing onto the Knicks court, and even getting Pumpfun and Bagwork tattoos.

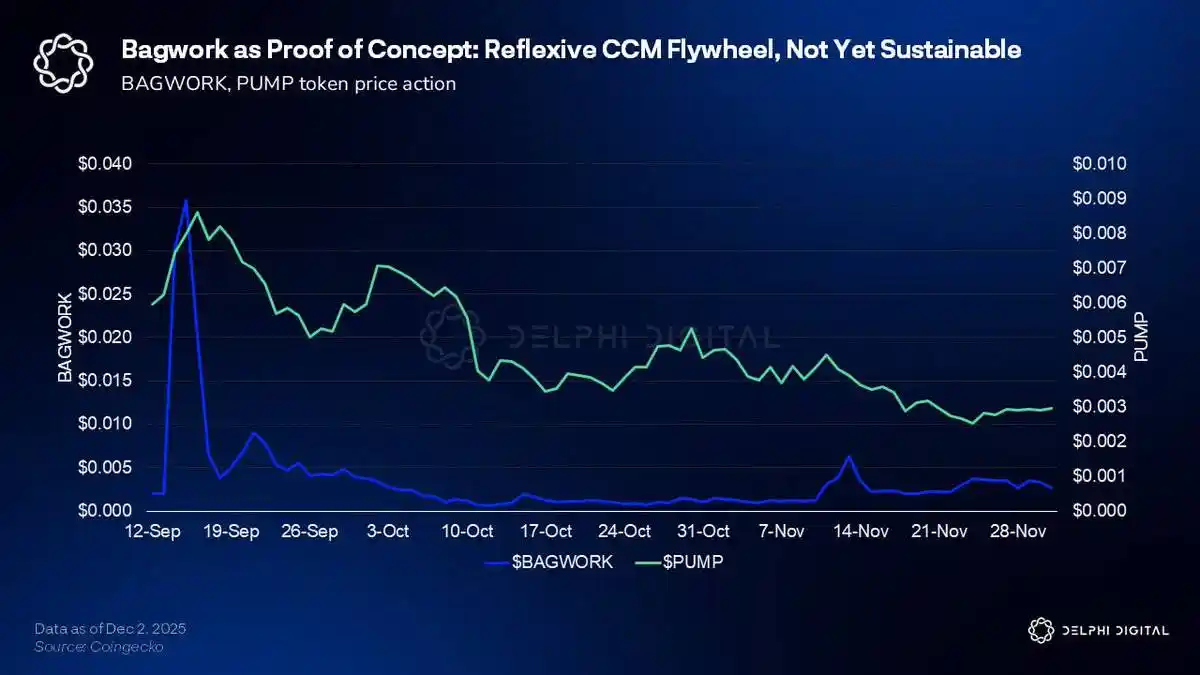

The rise of @onlybagwork was nearly perfectly synchronized with Pump.fun's peak hype in mid-September. At that time, $PUMP's fully diluted valuation (FDV) reached around $8.5 billion, and Bagwork's market cap also briefly surpassed $50 million.

However, since then, no creator token has been able to come close to such organic potential or reach a similar peak valuation.

The events at the Knicks arena happened more recently, long after the initial hype, and now Bagwork's market cap is only slightly above $2 million.

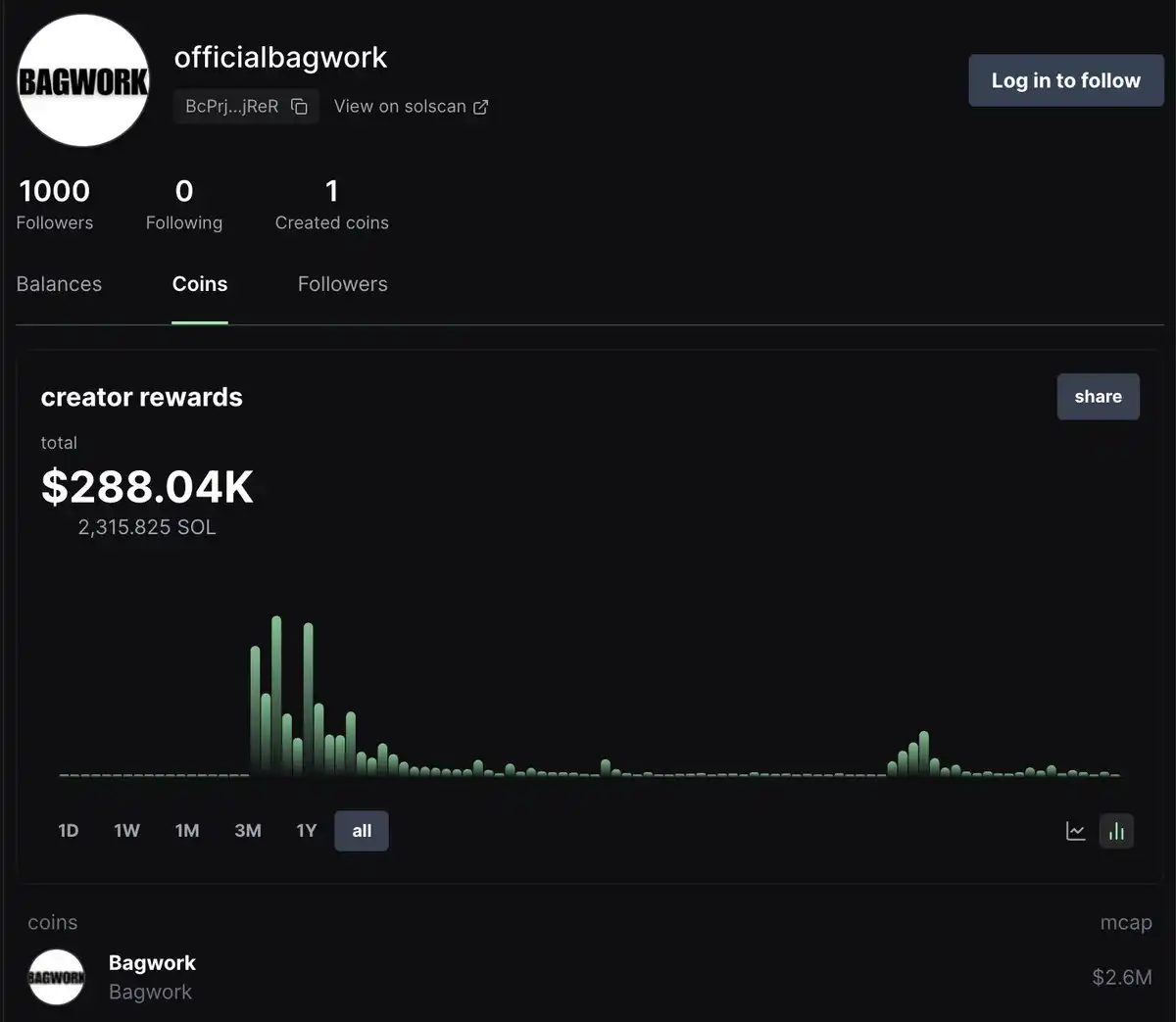

Bagwork is one of the few cases in the Pump streaming experiment that truly ran as expected. The Bagwork team earned over 2300 SOL in creator revenue through $BAGWORK's transaction fees (equivalent to around $300,000 at current prices).

It's worth noting that all of this was achieved without the team selling their holdings. The viral event directly converted into attention, trading volume, and fee revenue, creating the closest example Pump has had to a true creator token flywheel effect to date.

However, aside from Bagwork, Pump continues to struggle to realize its streaming vision. Creator tokens have consistently failed to hold their value. This can be traced back to a fundamental issue: the token is part of the product itself.

Currently, the economic rationale for owning or supporting a streamer token remains unclear. Bagwork's early success quickly faded, and since then, every major streamer token has failed to garner similar attention, ultimately dwindling to near zero.

Creators can earn short-term gains through CCM's fee structure, but the reputational risks associated with rug-pull tokens make this model unattractive to bigger names and more established creators who could have helped the platform reach a wider audience. From a trader's perspective, these tokens still exist in a zero-sum game environment rather than a true community.

This is the most critical issue Pump needs to address as it steps into 2026.

Currently, the team has yet to make meaningful attempts at a deeper creator incentive mechanism, and airdrop distribution remains untouched. Apart from informal support provided during the Bagwork craze, Pump has not taken any coordinated measures such as targeted airdrops, creator rewards, or other incentive mechanisms that could have been used to kickstart early activity, create more PvE (player versus environment) incentives, and provide a testing ground for creators without immediately disrupting their community ecosystem.

The good news is that this grants Pump significant flexibility.

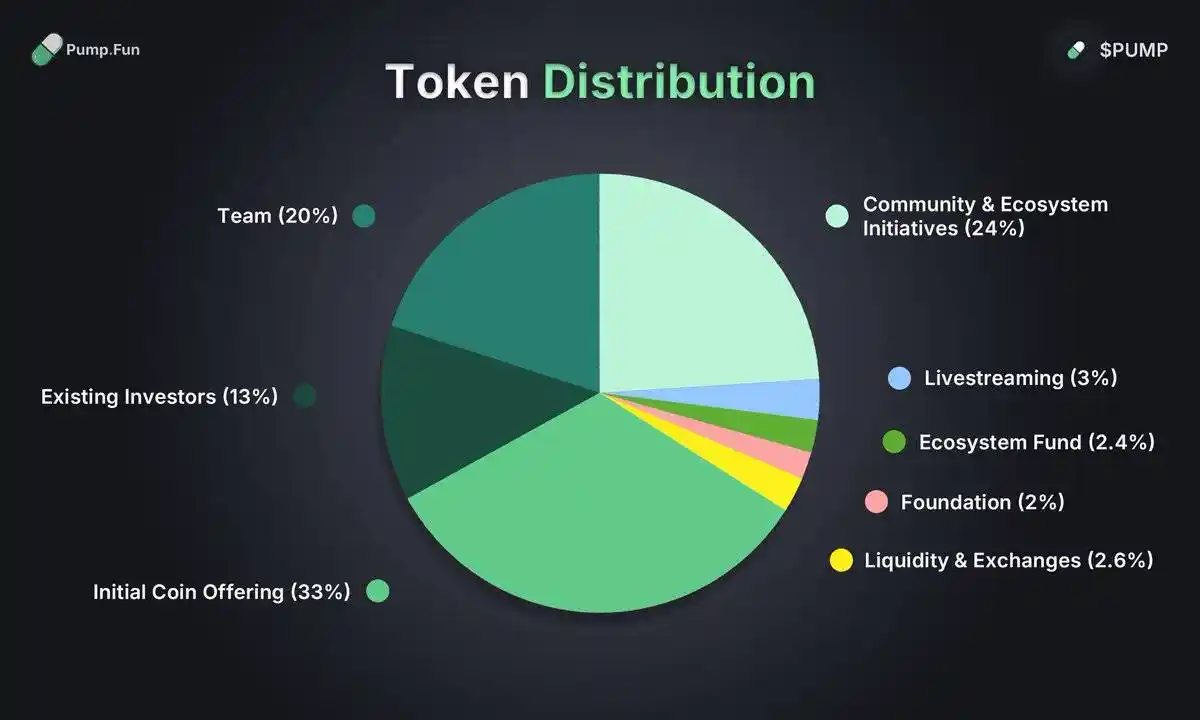

The untapped "Community & Ecosystem Initiatives" fund remains a key lever the team can leverage as the model matures. If Pump can design a sustainable creator token incentive structure, it will open up a whole new economic category for creators looking to leverage cryptographic mechanisms for monetization and audience expansion.

Despite the significant potential upside, streaming will continue to perform as a series of transient hype cycles rather than a persistent and replicable vertical field.

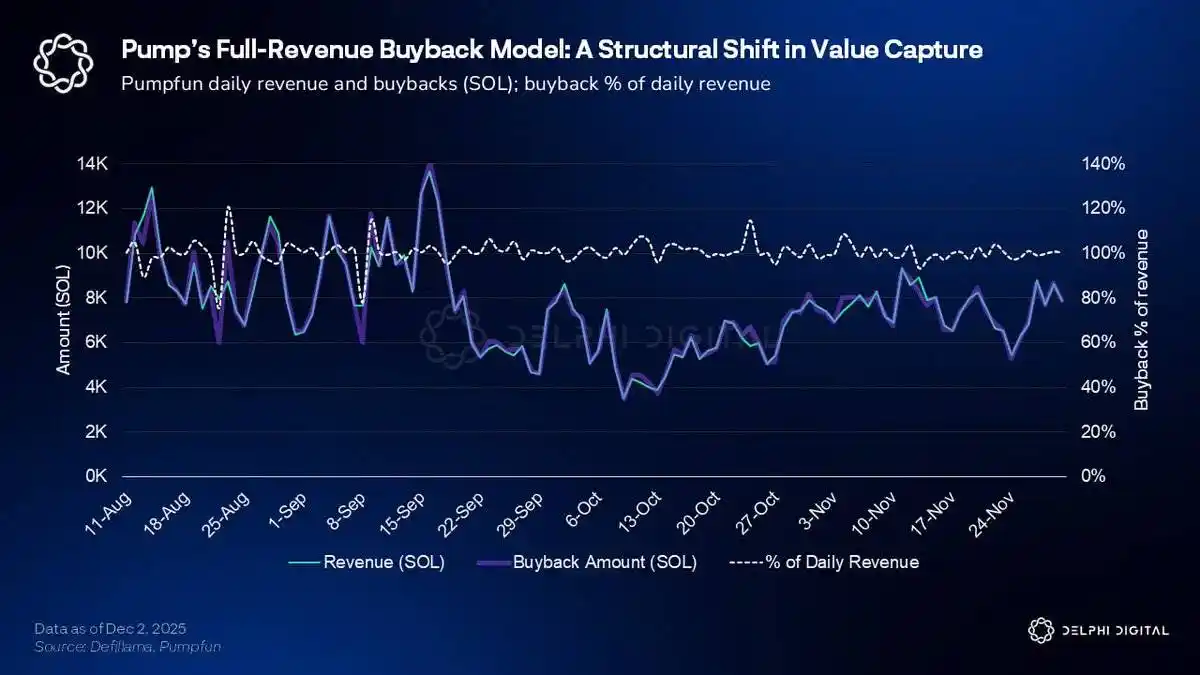

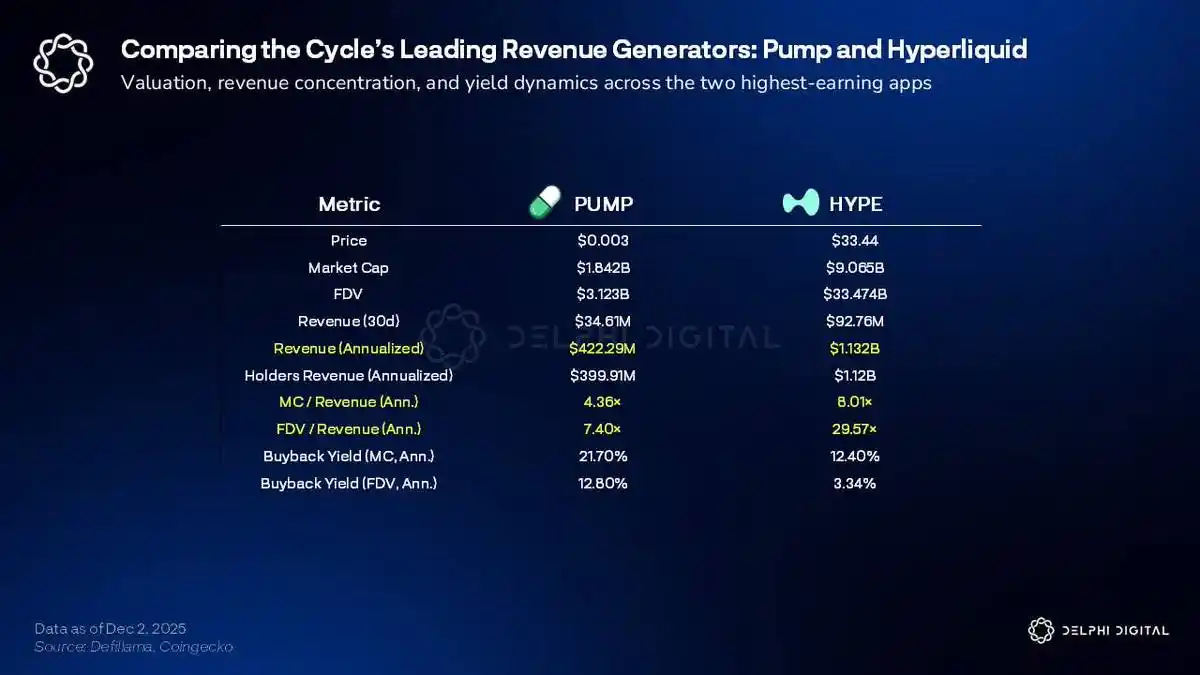

On the token front, a key catalyst driving $PUMP from around 0.025 to 0.085 was the team's decision to allocate 100% of net revenue to buybacks.

Pump initially planned to allocate around a quarter of revenue to buybacks but shifted to a buyback model heavily inspired by Hyperliquid. This shift was made after the market clearly signaled that a partial buyback model would not be well-received. This change ignited one of the strongest large-cap token rebounds this year in a liquidity-scarce and challenging altcoin market.

From a buyback-to-market cap ratio perspective, currently, no major token has a lower trading multiple.

Based on current data, Pump has an annualized revenue of $4.22 billion, a market cap of $18.4 billion, implying a market cap/revenue ratio (MC/Rev) of 4.36x and an annual buyback yield of approximately 12.8%. This level is significantly lower than other large-cap tokens, including Hyperliquid's approximately 8.01x MC/Rev and 3.34% yield.

Nevertheless, the market remains skeptical of Pump's long-term business prospects.

Market concerns may include: the team's ability to continually roll out meaningful products; the future impact of upcoming token supply unlocks, with around 40% of the supply still locked; and the uncertainty surrounding the final distribution of airdrops and creator incentive allocations. Additionally, doubts persist about the overall sustainability of the Meme coin activity in the crypto market, the reduction in end-user activity, and the sustainability of Pump's revenue base.

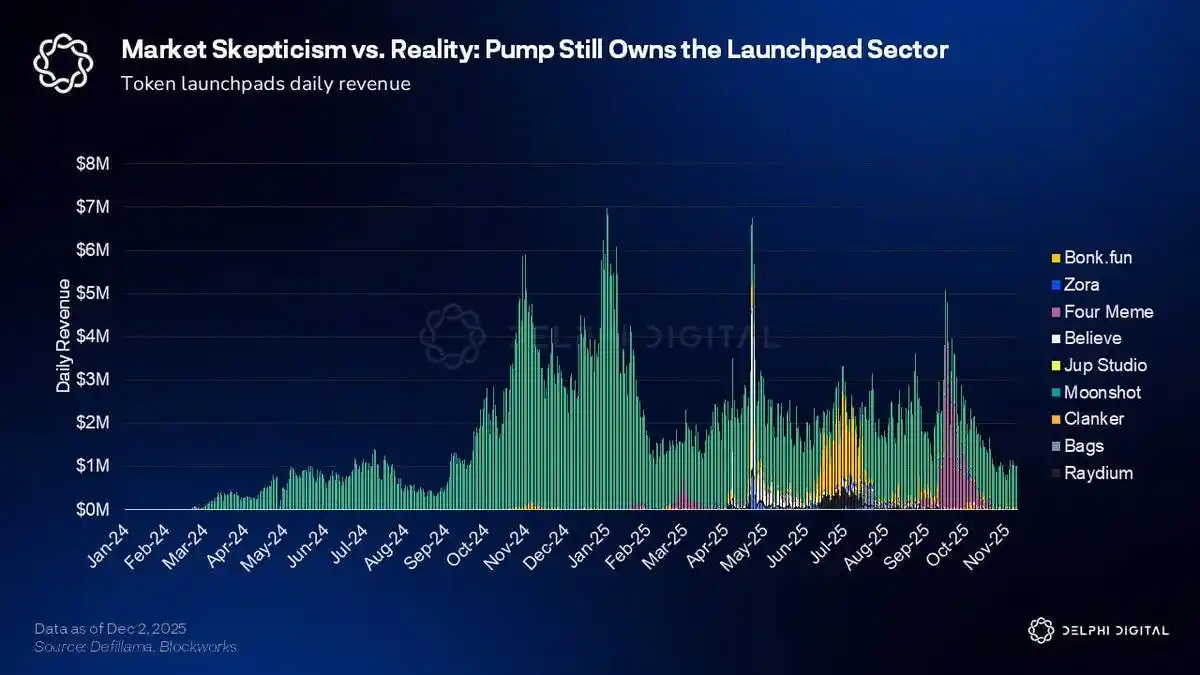

Despite these concerns, Pump continues to dominate in the Meme coin issuance platform space, earning (and buying back) approximately $1 million daily even in the current extremely challenging market environment.

The daily Launchpad revenue of Pump, which neared a peak of around $14 million at the beginning of the year, has significantly dropped by nearly 85% to approximately $2 million. However, competitors only briefly posed a threat to Pump's position and failed to bring a substantial challenge. This aligns with our initial prediction in the early reports regarding the brief challenge stages from Bonk and Raydium: even amidst a contraction in periodic trading volume, Pump has maintained its structural advantage, holding the dominant share of industry activity.

The acquisition of Padre has supported such a view: Pump is intentionally expanding beyond Solana into a multi-chain ecosystem and has added support for BNB ecosystem assets through the Padre frontend. This also aligns with our earlier prediction that Pump would eventually acquire an endpoint or endpoint-related asset to strengthen user acquisition channels and integrate more user journeys.

In addition to these actions, the team has recently maintained a low-key strategy. There are plans for an investor call, but as of the time of writing, it has not yet taken place, so there may be more detailed information to be disclosed later.

The leadership team has also expressed interest in a broader Initial Community Offering (ICO) category, although we believe this is not a core area of Pump's current brand positioning or product advantage. Pump initially experimented with the Believe model but failed to gain practical market attention. MetaDAO has now become a leader in the "high-quality founder + community" funding space.

Furthermore, the culture and structure of ICOs seem somewhat incongruent with Pump's brand positioning. Pump's brand core revolves around speculation, speed, and Meme culture for creators, rather than long-term governance or systems based on Futarchy. If Pump wants to succeed in the ICO space, they would need to lean more towards governance-focused structures and attract non-crypto teams looking to operate on-chain. However, this does not fully align with the current needs and positioning of Pump's users and creators. While theoretically, if the team were to take practical action, ICOs could bring some potential benefits, we believe this is more of a secondary or optional direction rather than a natural extension of Pump's existing flywheel effect in 2026.

Looking ahead to 2026, Pump faces key challenges in whether they can ultimately establish a creator token model that is incentive compatible, if they can achieve substantial expansion into multi-chain markets through Padre, how to manage the risk of token unlocks and declining revenue visibility, and which product vertical to focus on as their main thrust. Currently, Pump's strategy appears to be scattered across multiple directions, including streaming, ICOs, and mobile.

At some point in the future, the team may need to specifically focus on a core breakthrough. For much of 2025, this breakthrough seemed to be streaming, but that is no longer clear.

A bigger question is whether Pump can still attract larger non-crypto-native creators. This may require a redesign of the creator token flywheel mechanism, providing a stronger, longer-term incentive to support viral propagation beyond the crypto-native user base. Pump has the fundamental conditions to achieve this goal. The 2025 Bagwork craze briefly demonstrated the potential success of this pattern, with Pump seemingly on the verge of bridging the gap.

Furthermore, Pump still has ample room to expand its product suite. One strategic direction the team should seriously consider is entering into iGaming or casino-related verticals. Adopting a model similar to Kick or Stake aligns naturally with Pump's speculation-driven user base. This direction will deeply synergize with its meme coin and streaming strategic objectives, and the profit potential in this sector has already been validated.

Shuffle's net gambling revenue and weekly lottery distribution demonstrate the enormous potential of this sector when successfully executed.

Pump's mobile application is another advantage that has not been fully leveraged. Further expanding into the mobile space can broaden user acquisition channels, make the product more accessible to mainstream users, and provide more monetization scenarios for creators. If combined with iGaming, this can not only significantly expand Pump's potential audience but also strengthen the platform's existing successful elements.

Despite the uncertainty, Pump remains one of the most resilient consumer applications in this cycle, maintaining its leadership position even as the market landscape shifts. Substantial progress in any key direction could trigger a significant shift in market sentiment and help Pump achieve a breakthrough, attracting a broader non-crypto-native user base.

You may also like

December 24th Market Key Intelligence, How Much Did You Miss?

The Trillion-Dollar Stablecoin Battle: Binance Decides to Step in Again

Aave Community Governance Drama Escalates, What's the Overseas Crypto Community Talking About Today?

Where Did $362 Million Go? Hyperliquid Counters FUD in Decentralization Showdown

Key Market Information Discrepancy on December 24th - A Must-See! | Alpha Morning Report

2025 Whale Saga: Mansion Kidnapping, Supply Chain Poisoning, and Billions Liquidated

Ether pumps to outsiders, dumps in-house. Can Tom Lee's team still be trusted?

Coinbase Joins Prediction Market, AAVE Governance Dispute - What's the Overseas Crypto Community Talking About Today?

Over the past 24 hours, the crypto market has shown strong momentum across multiple dimensions. The mainstream discussion has focused on Coinbase's official entry into the prediction market through the acquisition of The Clearing Company, as well as the intense controversy within the AAVE community regarding token incentives and governance rights.

In terms of ecosystem development, Solana has introduced the innovative Kora fee layer aimed at reducing user transaction costs; meanwhile, the Perp DEX competition has intensified, with the showdown between Hyperliquid and Lighter sparking widespread community discussion on the future of decentralized derivatives.

This week, Coinbase announced the acquisition of The Clearing Company, marking another significant move to deepen its presence in this field after last week's announcement of launching a prediction market on its platform.

The Clearing Company's founder, Toni Gemayel, and the team will join Coinbase to jointly drive the development of the prediction market business.

Coinbase's Product Lead, Shan Aggarwal, stated that the growth of the prediction market is still in its early stages and predicts that 2026 will be the breakout year for this field.

The community has reacted positively to this, generally believing that Coinbase's entry will bring significant traffic and compliance advantages to the prediction market. However, this has also sparked discussions about the industry's competitive landscape.

Jai Bhavnani, Founder of Rivalry, commented that for startups, if their product model proves to be successful, industry giants like Coinbase have ample reason to replicate it.

This serves as a reminder to all entrepreneurs in the crypto space that they must build significant moats to withstand competition pressure from these giants.

Regulated prediction market platform Kalshi launched its research arm, Kalshi Research, this week, aimed at opening its internal data to the academic community and researchers to facilitate exploration of prediction market-related topics.

Its inaugural research report highlights Kalshi's outperformance in predicting inflation compared to Wall Street's traditional models. Kalshi co-founder Luana Lopes Lara commented that the power of prediction markets lies in the valuable data they generate, and it is now time to better utilize this data.

Meanwhile, Kalshi announced its support for the BNB Chain (BSC), allowing users to deposit and withdraw BNB and USDT via the BSC network.

This move is seen as a significant step for Kalshi to open its platform to a broader crypto user base, aiming to unlock access to the world's largest prediction market. Furthermore, Kalshi also revealed plans to host the first Prediction Market Summit in 2026 to further drive industry engagement and development.

The AAVE community recently engaged in heated debates around an Aave Improvement Proposal (AIP) titled "AAVE Tokenomics Alignment Phase One - Ownership Governance," aiming to transfer ownership and control of the Aave brand from Aave Labs to Aave DAO.

Aave founder Stani Kulechov publicly stated his intention to vote against the proposal, believing it oversimplifies the complex legal and operational structure, potentially slowing down the development process of core products like Aave V4.

The community's reaction was polarized. Some criticized Stani for adopting a "double standard" in governance and questioned whether his team had siphoned off protocol revenue, while others supported his cautious stance, arguing that significant governance changes require more thorough discussion.

This controversy highlights the tension between the ideal of DAO governance in DeFi projects and the actual power held by core development teams.

Despite governance disputes putting pressure on the AAVE token price, on-chain data shows that Stani Kulechov himself has purchased millions of dollars' worth of AAVE in the past few hours.

Simultaneously, a whale address, 0xDDC4, which had been quiet for 6 months, once again spent 500 ETH (approximately $1.53 million) to purchase 9,629 AAVE tokens. Data indicates that this whale has accumulated nearly 40,000 AAVE over the past year but is currently in an unrealized loss position.

The founder and whale's increased holdings during market volatility were interpreted by some investors as a confidence signal in AAVE's long-term value.

In this week's top article, Morpho Labs' "Curator Explained" detailed the role of "curators" in DeFi.

The article likened curators to asset managers in traditional finance, who design, deploy, and manage on-chain vaults, providing users with a one-click diversified investment portfolio.

Unlike traditional fund managers, DeFi curators execute strategies automatically through non-custodial smart contracts, allowing users to maintain full control of their assets. The article offered a new perspective on the specialization and risk management in the DeFi space.

Another widely circulated article, "Ethereum 2025: From Experiment to Global Infrastructure," provided a comprehensive summary of Ethereum's development over the past year. The article noted that 2025 is a crucial year for Ethereum's transition from an experimental project to global financial infrastructure. Through the Pectra and Fusaka hard forks, Ethereum achieved significant reductions in account abstraction and transaction costs.

Furthermore, the SEC's clarification of Ethereum's "non-securities" nature and the launch of tokenized funds on the Ethereum mainnet by traditional financial giants like JPMorgan marked Ethereum's gaining recognition from mainstream institutions. The article suggested that whether it is the continued growth of DeFi, the thriving L2 ecosystem, or the integration with the AI field, Ethereum's vision as the "world computer" is gradually becoming a reality.

The Solana Foundation engineering team released a fee layer solution called Kora this week.

Kora is a fee relayer and signatory node designed to provide the Solana ecosystem with a more flexible transaction fee payment method. Through Kora, users will be able to achieve gas-free transactions or choose to pay network fees using any stablecoin or SPL token. This innovation is seen as an important step in lowering the barrier of entry for new users and improving Solana network's availability.

Additionally, a deep research report on propAMM (proactive market maker) sparked community interest. The report's data analysis of propAMMs on Solana like HumidiFi indicated that Solana has achieved, or even surpassed, the level of transaction execution quality in traditional finance (TradFi) markets.

For example, on the SOL-USDC trading pair, HumidiFi is able to provide a highly competitive spread for large trades (0.4-1.6 bps), which is already better than the trading slippage of some mid-cap stocks in traditional markets.

Research suggests that propAMM is making the vision of the "Internet Capital Market" a reality, with Solana emerging as the prime venue for all of this to happen.

The competition in the perpetual contract DEX (Perp DEX) space is becoming increasingly heated.

In its latest official article, Hyperliquid has positioned its emerging competitor, Lighter, alongside centralized exchanges like Binance, referring to it as a platform utilizing a centralized sequencer. Hyperliquid emphasizes its transparency advantage of being "fully on-chain, operated by a validator network, and with no hidden state."

The community widely interprets this as Hyperliquid declaring "war" on Lighter. The technical differences between the two platforms have also become a focal point of discussion: Hyperliquid focuses on ultimate on-chain transparency, while Lighter emphasizes achieving "verifiable execution" through zero-knowledge proofs to provide users with a Central Limit Order Book (CLOB)-like trading experience.

This battle over the future direction of decentralized derivatives exchanges is expected to peak in 2026.

Meanwhile, discussions about Lighter's trading fees have surfaced. Some users have pointed out that Lighter charged as much as 81 basis points (0.81%) for a $2 million USD/JPY forex trade, far exceeding the near-zero spreads of traditional forex brokers.

Some argue that Lighter does not follow a B-book model that bets against market makers, instead anchoring its prices to the TradFi market, and the high fees may be related to the current liquidity or market maker balance incentives. Providing a more competitive spread for real-world assets (RWA) in the highly volatile crypto market is a key issue Lighter will need to address in the future.

Why Did Market Sentiment Completely Collapse in 2025? Decoding Messari's Ten-Thousand-Word Annual Report

Audiera Sees Massive Price Surge – Key Cryptocurrency Updates

Key Takeaways Audiera (BEAT) has witnessed significant growth, experiencing a 70.10% increase in the past week. Despite the…

Market Outlook: The Future of Cryptocurrency by 2026

Key Takeaways The report focuses on the impact of critical factors like Bitcoin, Ethereum, and Solana, alongside regulatory…

Former SEC Counsel Explains What It Takes to Achieve Compliance in RWA Tokenization

Key Takeaways Shifts in the SEC’s regulatory approach to cryptocurrency are aiding the growth of compliance in Real-World…

Blockchains Quietly Prepare for Quantum Threat Amid Bitcoin’s Debate Over Timeline

Key Takeaways Many blockchains are preparing for potential threats from quantum computing by integrating post-quantum technologies. Ethereum views…

Ronin and ZKsync’s Onchain Metrics Experienced Notable Declines in 2025

Key Takeaways Some of the major blockchain networks, including Ronin and ZKsync, saw a significant reduction in onchain…

Open Source Achilles' Heel: Nofx and Its 9,000-Star Drama, Forking Fiasco, and Open Source Controversy

Stablecoin Weekly Report | Decrypting How Crypto is Reinventing the Internet's Killer Apps through Coinbase's System Upgrade

Upcoming Lighter TGE: What Is a Reasonable Valuation? As a finance and blockchain translation expert, you are familiar with the field's slang and terminology.

Security Tokenization and Prediction Markets: 7 Major Crypto Boons to Watch in 2026

December 24th Market Key Intelligence, How Much Did You Miss?

The Trillion-Dollar Stablecoin Battle: Binance Decides to Step in Again

Aave Community Governance Drama Escalates, What's the Overseas Crypto Community Talking About Today?

Where Did $362 Million Go? Hyperliquid Counters FUD in Decentralization Showdown

Key Market Information Discrepancy on December 24th - A Must-See! | Alpha Morning Report

2025 Whale Saga: Mansion Kidnapping, Supply Chain Poisoning, and Billions Liquidated

Popular coins

Latest Crypto News

Customer Support:@weikecs

Business Cooperation:@weikecs

Quant Trading & MM:[email protected]

VIP Services:[email protected]